B4555 - Chapter 10

Auditing the Revenue Process

November 15, 2023

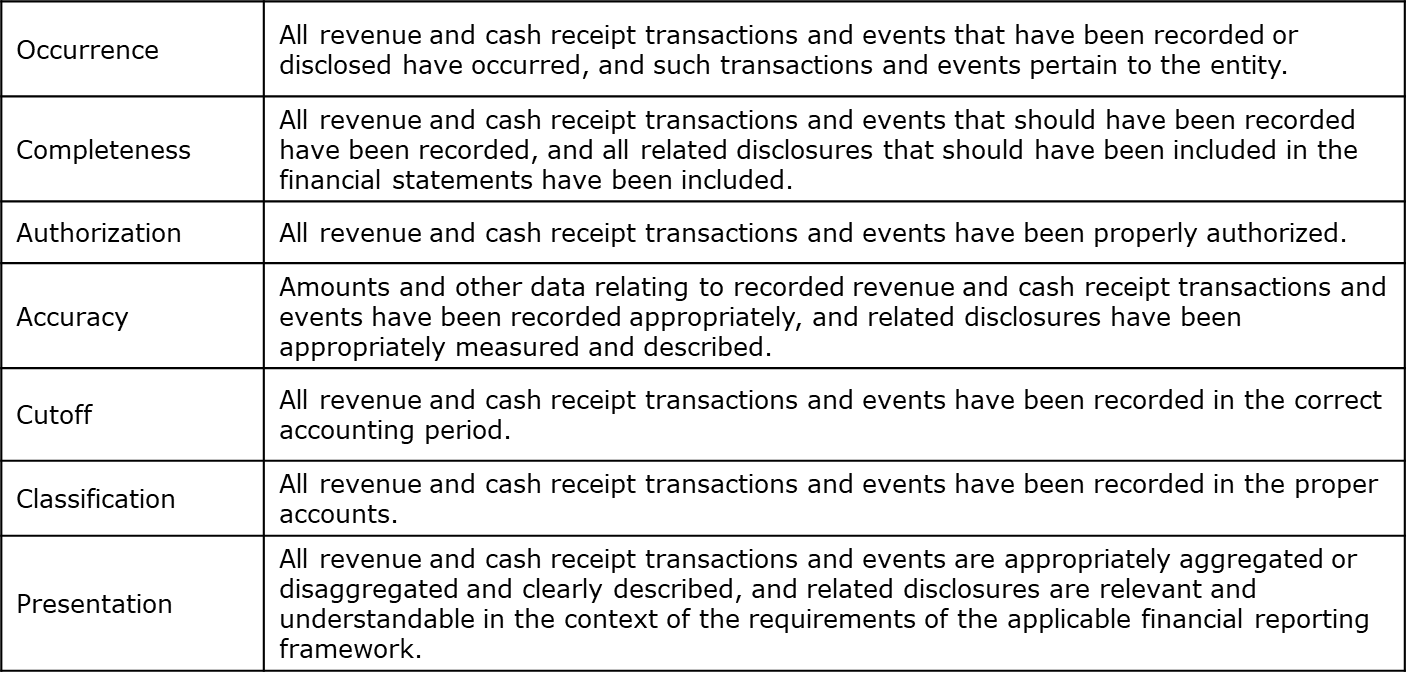

Revenue Recognition

Revenue must be recognized in conformity with GAAP in order for an auditor to issue an unqualified opinion

Revenue is defined as inflows or other enhancements of assets of an entity or settlements of its liabilities (or a combination of both) from delivery or producing goods, rendering services, or other activities that constitute the entity’s major or central operations

The accounting standard for revenue contains principles that an entity should apply to determine the measurement of revenue and timing of when it is recognized

The underlying principle is that “an entity recognizes revenue to depict the transfer of promised goods/services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods/services”

Five-Step Approach to Revenue Recognition

(1) Identify the contract(s) with a customer

(2) Identify the performance obligations in the contract

(3) Determine the transaction price

(4) Allocate the transaction price to the performance obligations in the contract

(5) Recognize revenue when the entity satisfies a performance obligation

Fraud Risks in Revenue Recognition

(1) Side agreements are arrangements that are used to alter the terms and conditions of recorded sales to entice customers to accept delivery of goods/services

(2) Channel stuffing (aka., trade loading) is a marketing practice that suppliers use to boost sales by inducing distributors to buy substantially more inventory than they can promptly resell

Revenue is overstated

(3) Related party transactions are transactions that are not considered arms-length and they require special consideration because related parties can be difficult to identify and may pose significant “substance over form” issues

(4) Bill and hold sales (aka., parked inventory schemes) are sales where the customer agrees to purchase the goods, but the seller retains physical possession ntil the customer requests shipments, unless certain conditions are met

Overview of the Revenue Process

Cash sale: purchases 🡪 inventory 🡪 cash sales

Credit sale: purchases 🡪 inventory 🡪 credit sales 🡪 AR 🡪 cash collection

Types of Transactions and FS Accounts Affected

Three types of transactions are processed through the revenue process:

(1) The sale of goods or rendering of a service for cash or credit

(2) The receipt of cash from the customer in payment for goods or services

(3) The return of goods by the customer for credit or cash

The revenue process affects numerous accounts in the financial statements. The most significant accounts are:

(1) Sales transactions

Trade AR

Sales

Allowance for uncollectible accounts

Bad debt expense

(2) Cash receipts transactions

Cash

Trade AR

Cash discounts

(3) Sales return and allowance transactions

Sales returns

Sales allowances

Trade AR

Types of Documents and Records

Credit approval form – for credit sales, the entity must have a formal procedure for investigating the creditworthiness of the customer

Customer sales order – contains the details of the type and quantity of products or services ordered by the customer

Open order report – a report of all customer orders for which processing has not been completed.

Shipping document – this document generally serves as a bill of lading and contains info on the type of product shipped, the quantity shipped, and other relevant info

Sales invoice – the document is used to bill the customer

This document contains information on the type of product or service, the quantity, the price, and the terms of trade.

Sales journal – once a sales invoice has been issued, the sale needs to be recorded in the accounting records. The sales journal is used to record information about the sales transaction.

Customer statement – this document is mailed to the customer and contains details of all sales, cash receipts, and credit memorandum transactions

AR subsidiary ledger – this ledger contains an account and the details of transactions for each customer

Aged TB of AR – this report summarizes all the customer balances in the accounts receivable subsidiary ledger

Each account is classified as current or placed into one of several past due categories

Remittance advice – this is usually the part of the customer’s bill that should be returned with the payment

Cash receipts journal – this journal is used to record the cash receipts of the entity

Credit memorandum – this document is used to record credits for the return of goods by a customer

Write off authorization – this document authorizes the write-off of an uncollectible account receivable

Final approval is generally authorized by the treasurer

The Major Functions

Functions of the revenue process:

Order entry is the acceptance of customer orders of goods/services into the system in accordance with management criteria

The initial function in the revenue process is the entity of a new sales order into the system

Credit authorization is the appropriate approval of customer orders for creditworthiness

The credit authorization process must determine that the customer is able to pay for the goods or services purchased

Failure to properly authorize credit can lead to extensive bad debts for the entity

Shipping is the shipping of goods that has been authorized

Goods should not be shipped, nor should services be provided without proper authorization

The main control is payment or proper credit authorization

Billing is the issuance of sales invoices to customers or goods shipped or services provided; also, processing of billing adjustments for allowances, discounts, and returns

The objective of proper billing is to ensure that all goods shipped, and all services rendered are billed to the customer

Cash receipts is the processing of the receipt of cash from customers

All cash collected must be properly identified and promptly deposited intact at the bank

AR is the recording of all sales invoices, collections, and credit memoranda in individual customer accounts

All billings, adjustments, and cash collections must be properly recorded in the customers’ accounts receivable records

GL is the proper accumulation, classification, and summarization of revenues, collections, and receivables in the FS accounts

As related to the revenue process, the general ledger function must ensure that all revenues, collections, and receivables are properly recorded and classified

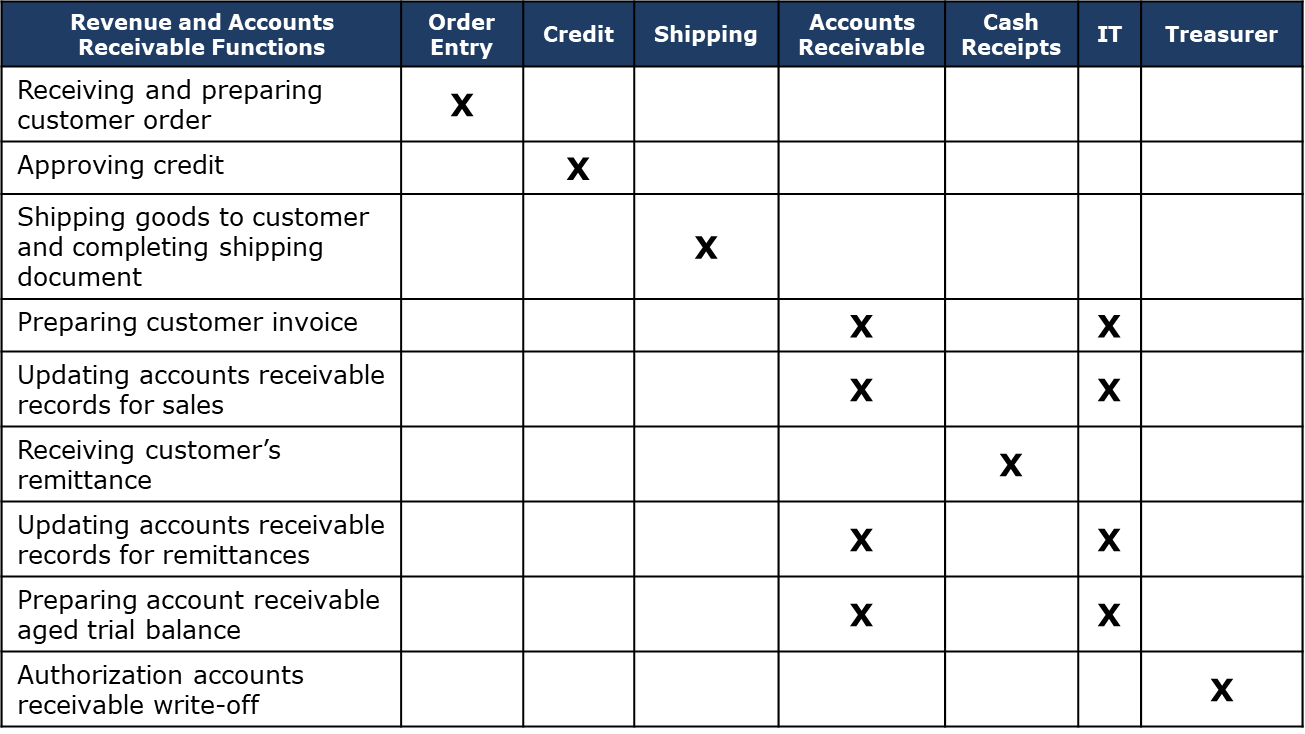

Key Segregation of Duties

Important in the revenue process because of the potential for theft and fraud

Individuals involved in the order entry, credit, shipping, or billing functions should not have access to the AR records, the GL, or any cash receipts activities

Table 10.4 – segregation of duties for the revenue process functions by department:

Inherent Risk Assessment

The four inherent risk factors that may affect the revenue process are:

(1) Industry related factors

(2) The complexity and contentiousness of revenue recognition issues

(3) The difficulty of auditing transactions and account balances

(4) Misstatements detected in prior audits

Control Risk Assessment

(1) Understand and document the revenue process based on a reliance strategy

(2) Plan and perform tests of controls on revenue transactions

(3) Set and document the control risk for the revenue process

Understanding and Documenting Internal Control

(1) Control environment

Understanding the control environment is generally completed on an overall entity basis

(2) The entity’s risk assessment process

The auditor must understand how management considers risks that are relevant to the revenue process

The auditor should estimate the significance of the risk and assess the likelihood of occurrence

(3) Control activities

The auditor identifies what controls ensure that the assertions for transactions and events are being met

Documentation of the auditor’s understanding of the revenue process can be accomplished by using …

(1) Procedures manuals

(2) Narrative descriptions

(3) Internal control questionnaire

(4) Flowcharts

(4) Info systems and communication

The process by which sales, cash receipts, and sales returns and allowances transactions are initiated

The flow of each transaction from initiation to inclusion in the FS

The accounting records, supporting documents, and accounts that are involved in sales, cash receipts, and sales returns

The process used to prepare estimates for accounts such as bad debts and sales returns

(5) Monitoring of controls

The auditor must understand how management assesses the design and operation of controls in the revenue process

This understanding should include how supervisory personnel review the personnel who perform the controls and evaluate the performance of the entity’s IT function

Plan and Perform Tests of Controls

The auditor systematically examines the entity’s revenue process to identify relevant controls that help to prevent, or detect and correct, material misstatement

To properly set control risk, the auditor must test controls over the revenue process – such tests may include …

Inquiry of client personnel

Inspection of documents and records

Observations of the operation of the control

Walkthroughs

Reperformance of the control activities

Set and Document the Control Risk

If the results of the tests of controls support the planned level of control risk, the auditor conducts the planned level of substantive procedures for the account balances

The level of control risk for the revenue process can be set using either quantitative amounts or

qualitative terms such as “low,” “medium,” or “high”

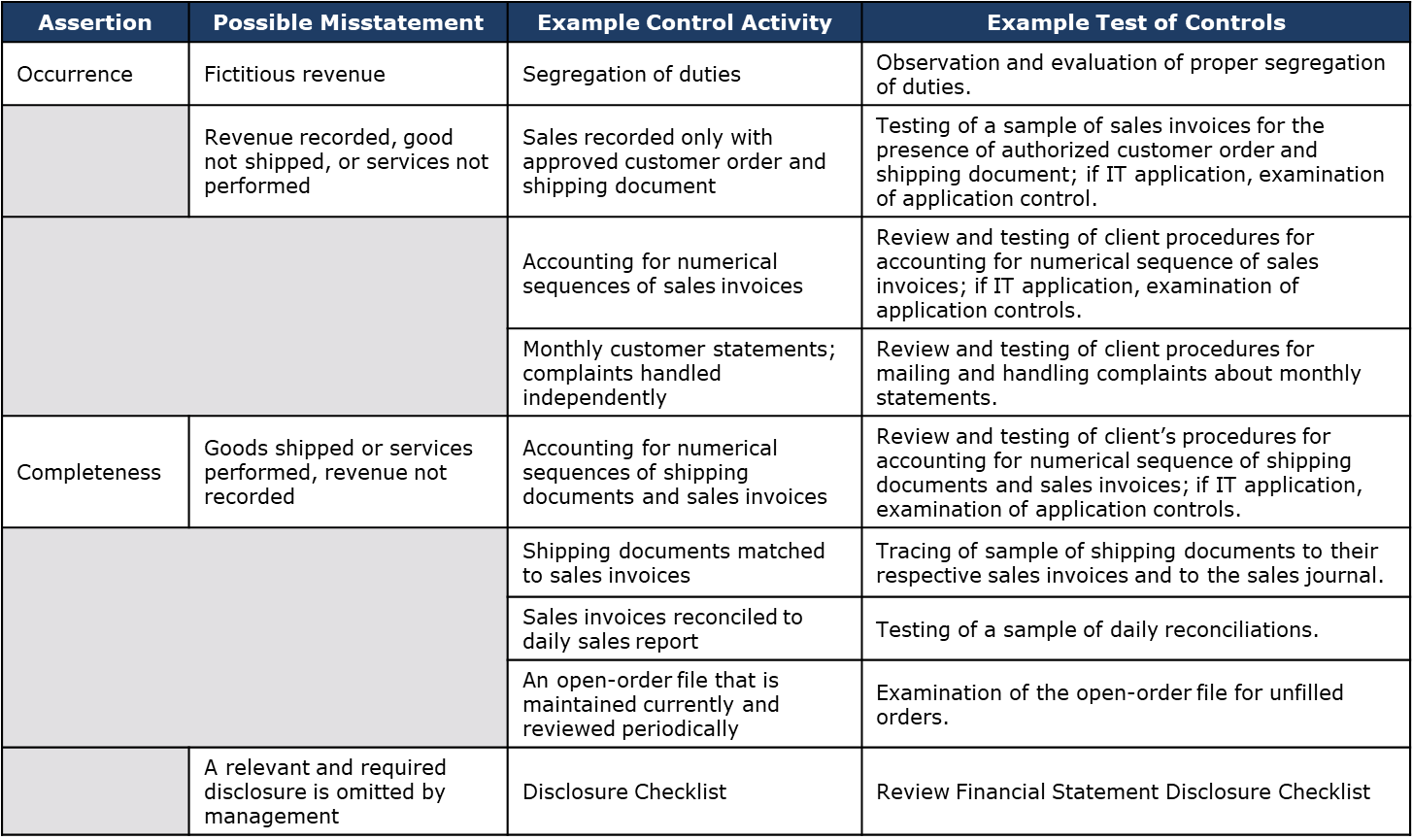

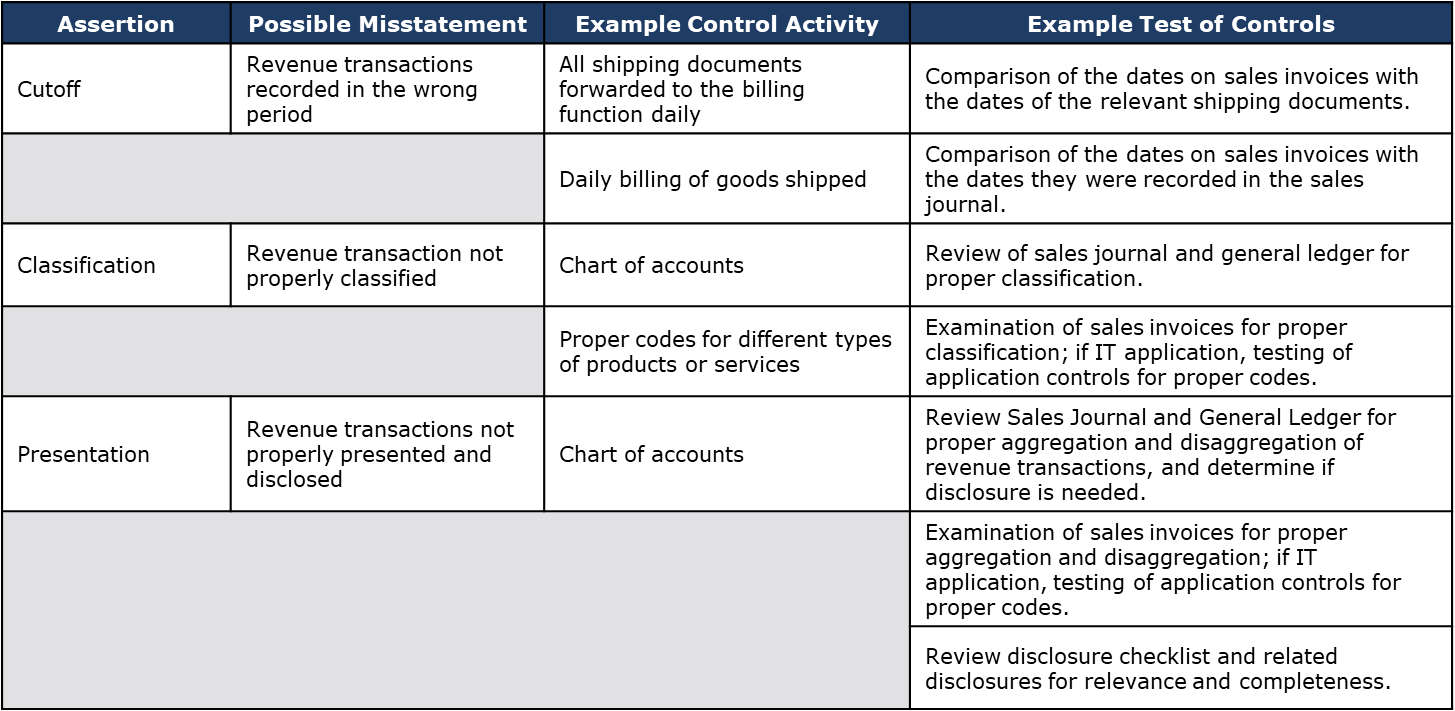

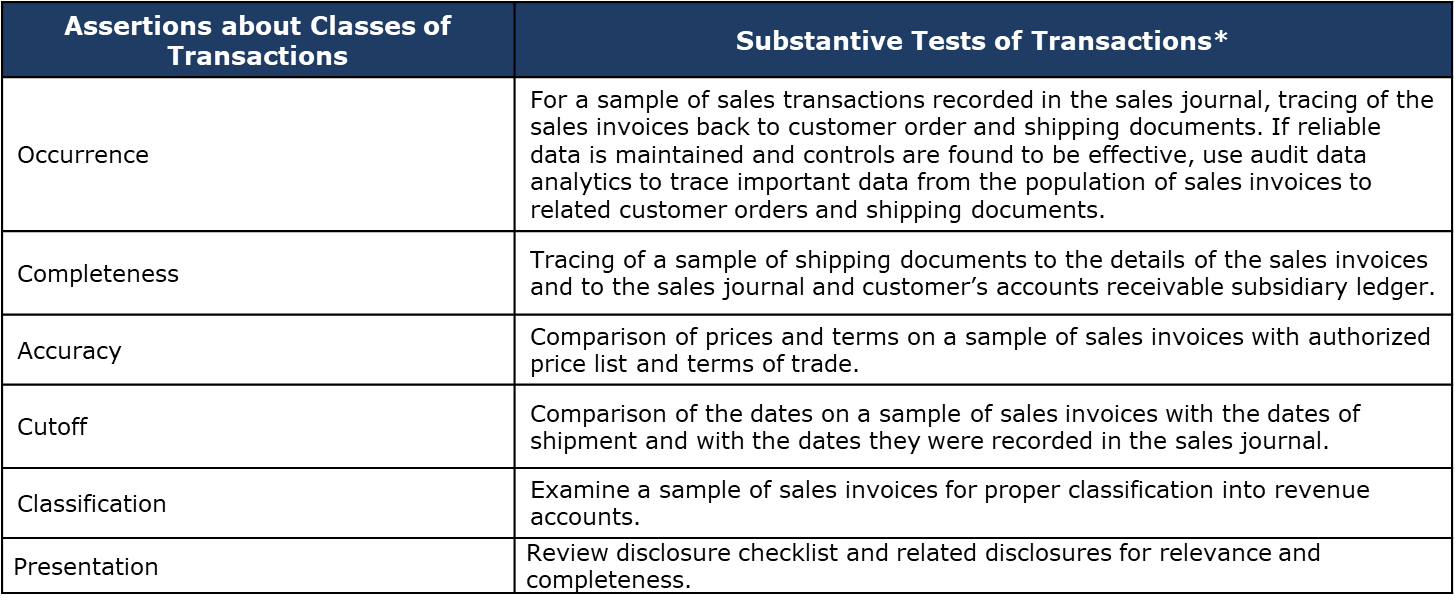

Control Activities and Test of Controls – Revenue Transactions

Table 10.5 – assertions about classes of transactions and events for the period under audit:

Table 10.6 – example tests of controls for revenue transactions

Occurrence of Revenue Transactions

The auditor is concerned about two major types of material misstatements:

(1) Sales to fictitious customers

(2) Recording revenue when goods have not been shipped or services have not been performed

The auditor needs assurance that all recorded revenue transactions are valid

Completeness of Revenue Transactions

The major misstatement that concerns both management and the auditor is that goods are shipped, or services are performed, and no revenue is recognized

Controls concerning completeness include:

(1) Accounting for numerical sequence of shipping documents and sales invoices

(2) Matching shipping documents with sales invoices

(3) Reconciling sales invoices to daily sales reports

(4) Maintaining and reviewing the open-order file

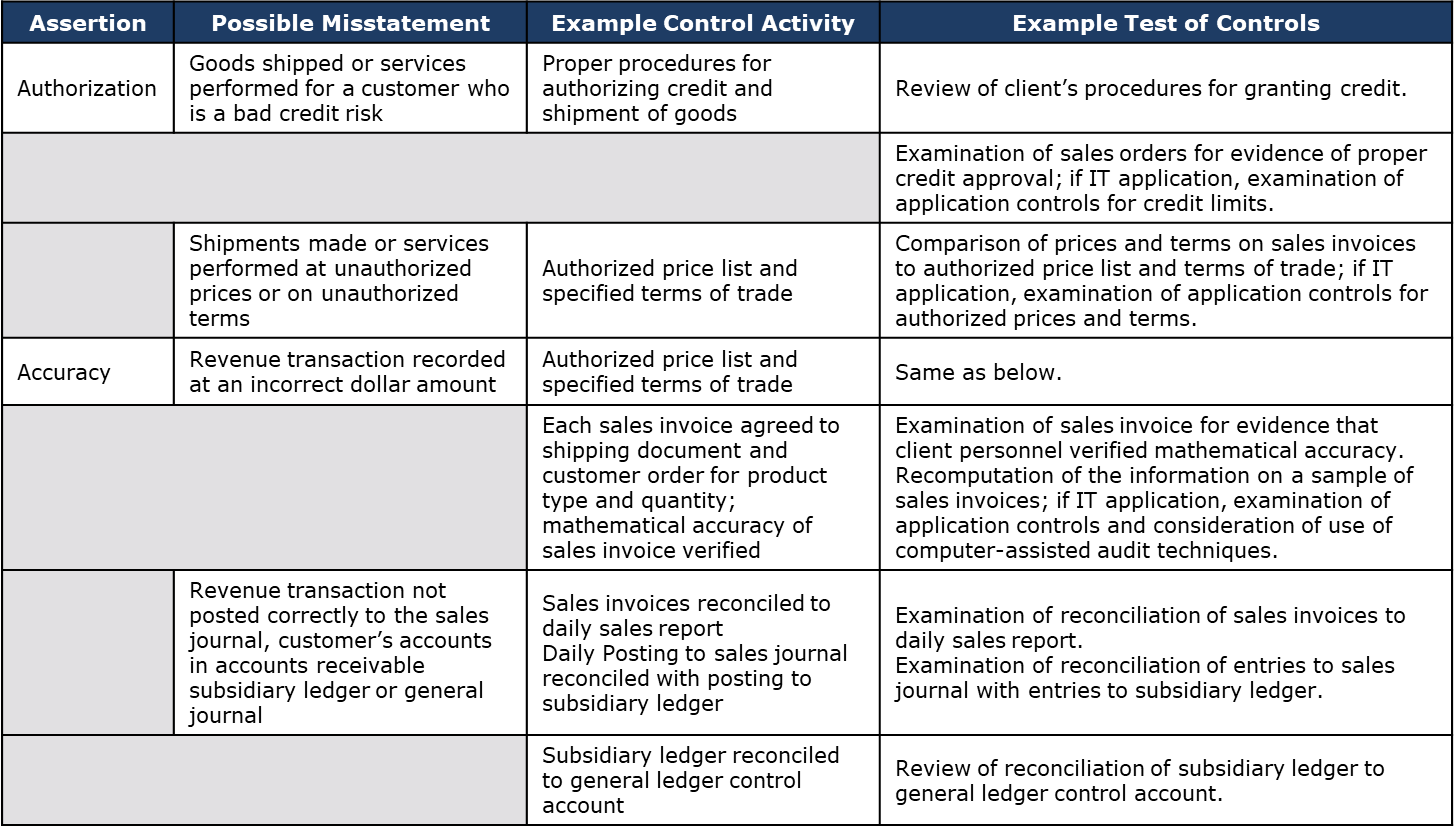

Authorization and Accuracy of Revenue Transactions

Possible misstatements due to improper authorization include shipping goods to, or performing services for, customers who are bad credit risks and making sales at unauthorized prices or terms

The presence of an authorized price list and terms of trade reduces the risk of inaccuracies

The sales invoice should also be verified for mathematical accuracy before being sent to the customer

Cutoff and Classification of Revenue Transactions

Sales may be recorded in the wrong accounting period unless proper controls are in place

All shipping documents should be forwarded to the billing department daily

The use of a chart of accounts and proper codes for recording transactions should provide adequate assurance about the proper classification of revenue transactions

Presentation of Revenue Transactions

Auditor’s tests of controls around management’s use of a chart of accounts, proper codes for recording revenue transactions, and the financial reporting process, including the use of a disclosure checklist, should provide adequate assurance for the presentation assertion

November 17, 2023

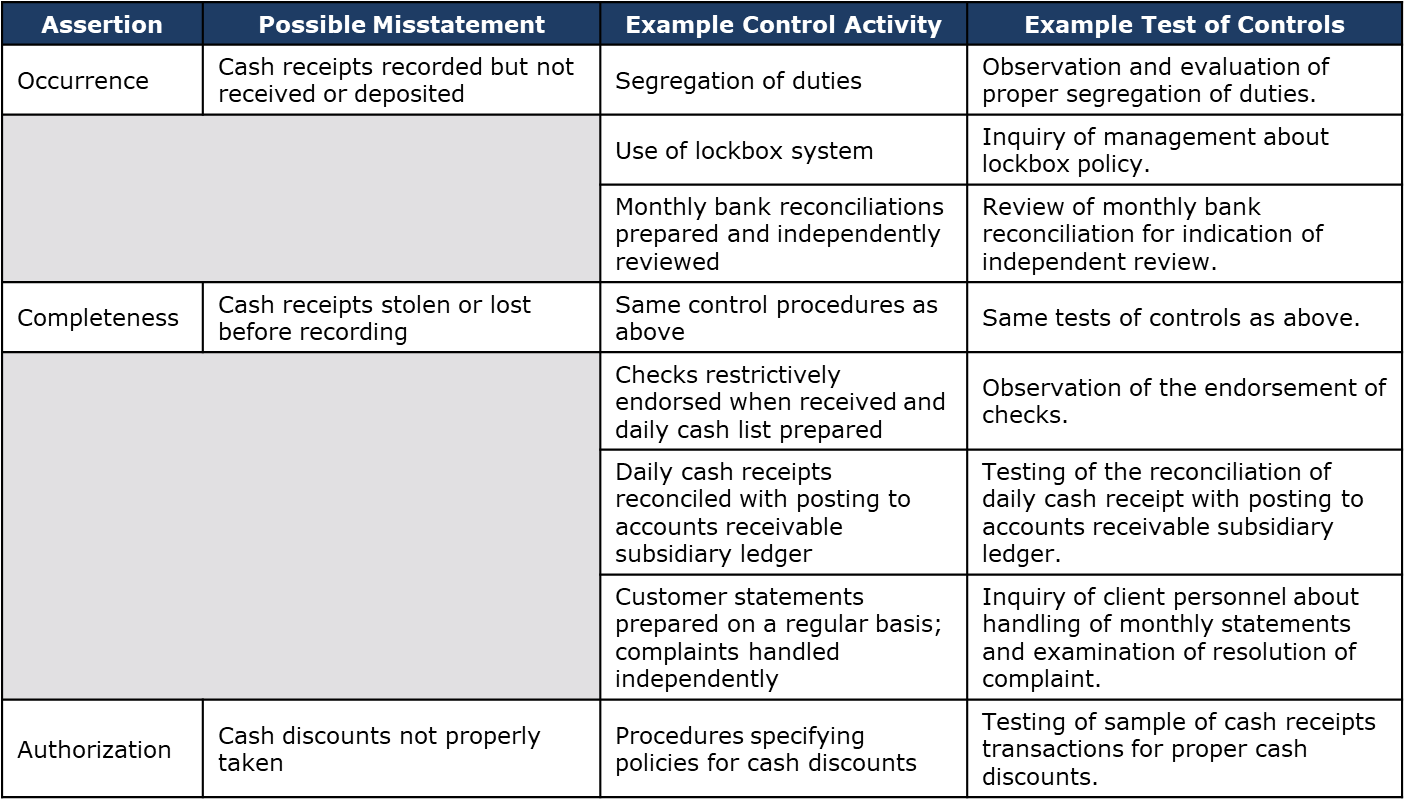

Control Activities and Test of Controls – Cash Receipts Transactions

Table 10.7 – example tests of controls for cash receipts transactions

Occurrence of Cash Receipts Transactions

The possible misstatement that concerns the auditor when considering the occurrence assertion is that cash receipts are recorded but not deposited in the entity’s bank account

Completeness of Cash Receipts and Authorization of Discounts

A major misstatement is that cash or checks are stolen or lost before being recorded in the cash receipts records. Proper segregation of duties and a lockbox system are strong controls relating to completeness

2/10, n/30 – terms of trade generally include discounts for payment within a specified period as a way of encouraging customers to pay on time

Controls in the accounting system and data analytics should ensure that management’s policies concerning cash discounts are followed

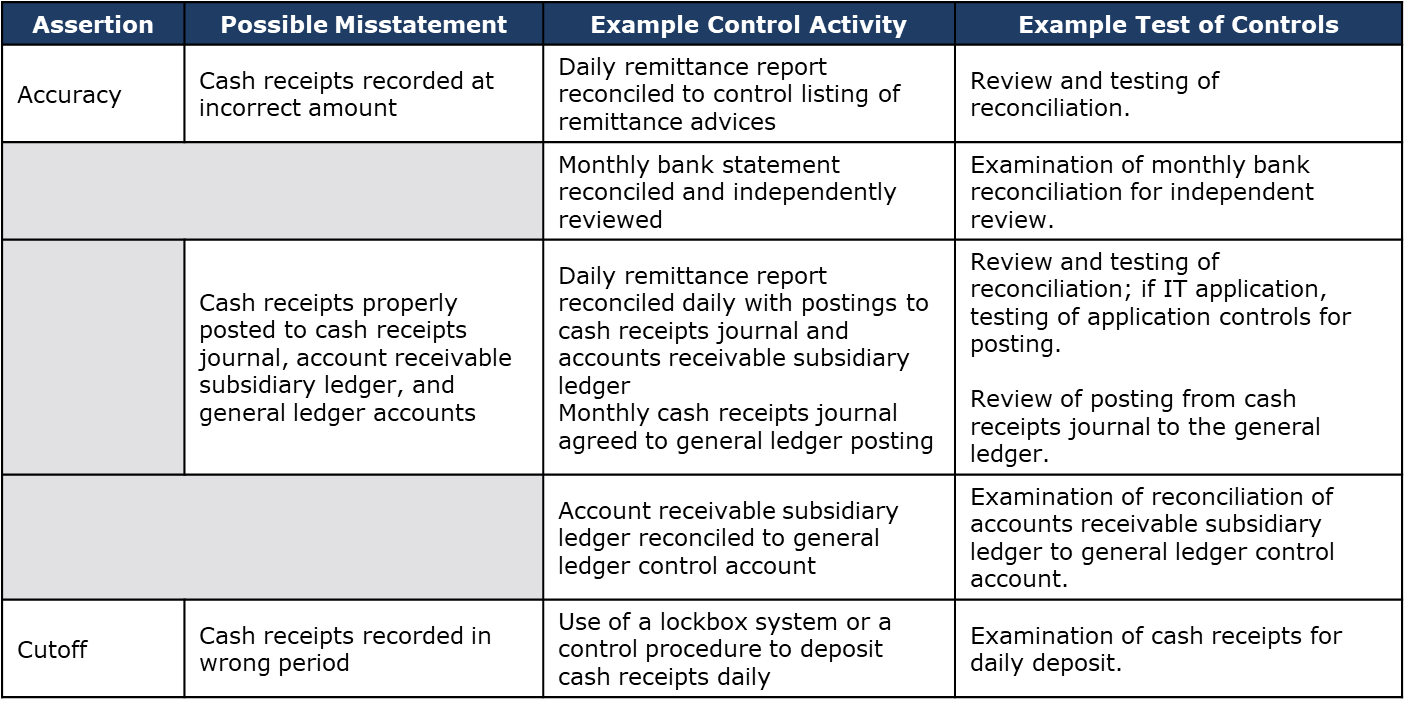

Accuracy of Cash Transactions

The wrong amount of cash could be recorded from the remittance advice, or the receipt could be incorrectly processed during data entry

To minimize these types of errors, daily remittance reports should be reconciled to a control listing of remittance advices

The use of monthly customer statements also provides a check on posting to the correct customer account

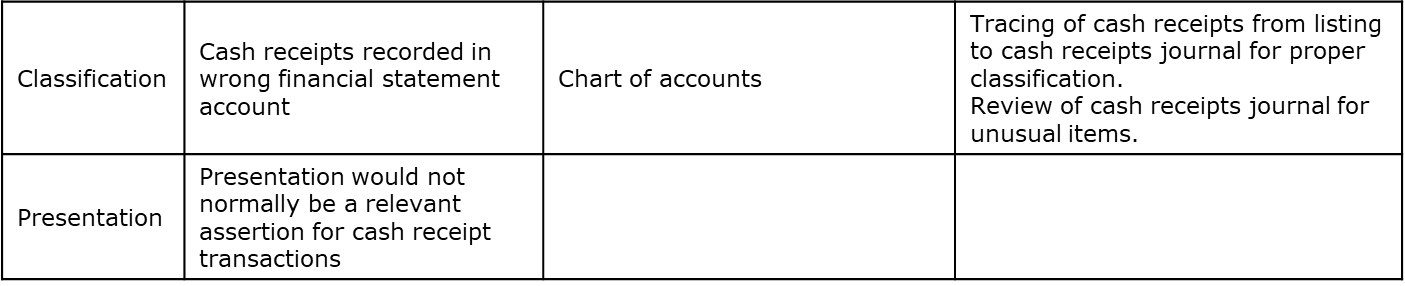

Cutoff and Classification of Cash Receipts Transactions

If the entity uses a lockbox system or if cash is deposited daily in the bank, there is a small possibility of cash being recorded in the wrong accounting period

The auditor seldom has major concerns about cash receipts being recorded in the wrong FS account

Control Activities and Tests of Controls – Sales Returns and Allowances

Sales returns and allowances is usually not a material amount in the financial statements. However, credit memoranda that are used to process sales returns can also be used to cover an unauthorized shipment of goods or conceal a misappropriation of cash

As a result, all credit memoranda should be properly authorized

A credit for returned goods should be supported by a receiving document indicating that the goods have been returned

Relating the Assessed Level of Control Risk to Substantive Procedures

The auditor’s testing of control for revenue processing impacts the detection risk and therefore the level of substantive procedures impacted by the control

AR, sales, cash, allowance for bad debts, sales returns and allowances, and bad debt expense

Auditing Revenue Related Accounts

Substantive analytical procedures are used to examine plausible relationships among revenue related accounts

This gives us an idea as to where we will spend most of our time during our audit testing

Tests of details focus on transactions, account balances, or disclosures

Tests of details concentrate on the ending balance for AR and related accounts as well as related disclosures

What account balances would we want to test to make sure that they’re fairly stated?

AR, sales (tests of controls & tests of transactions)

If we are confident that the sale transactions and receipts, then our account balances that we want to look at are our AR, AFDA, and the BS

Review of Revenue Recognition

T account for AR:

DR. Sales

CR. Cash receipts

CR. Sales discounts

CR. Sales returns and allowances

We want to make sure that the balance is not misstated materially

T account for inventory:

DR. Purchases

Associated with AP

We can do dual-purpose tests when we’re doing purchase and payables

DR. Sales returns (returned inventory)

This is related to AR 🡪 customers are getting credit for goods that are returned 🡪 ensure that the receiving documents matches the credit memo

CR. Cost of goods sold

We can do dual-purpose tests

CR. Inventory write-offs

CR. Purchase discounts

CR. Purchase returns

Common test for the balance of inventory 🡪 inventory count & test counts

Test counts = choosing a sample of inventory and ensure that it exists, it has been counted correctly and been recognized in the GL correctly

Substantive Analytical Procedures

Ratios used for comparative purposes include:

(1) Receivables turnover and days outstanding in AR

(2) Aging categories on aged trial balance of AR

We can age it ourselves using IDEA

We can do our own estimates of what the uncollectible balance should be and more easily support/provide evidence for the AFDA

(3) Bad-debts expense as a percent of revenue

(4) Allowance for uncollectible accounts as a percent of AR or credit sales

(5) Large customer account balances compared to last period

Table 10.10 – for AR, allowance for uncollectible accounts, and bad debt expense:

*Each of these substantive tests of transactions could be conducted as a test of controls or a dual-purpose test. Of these six assertions, the cutoff assertion is the one that is most often conducted as a substantive test of transactions

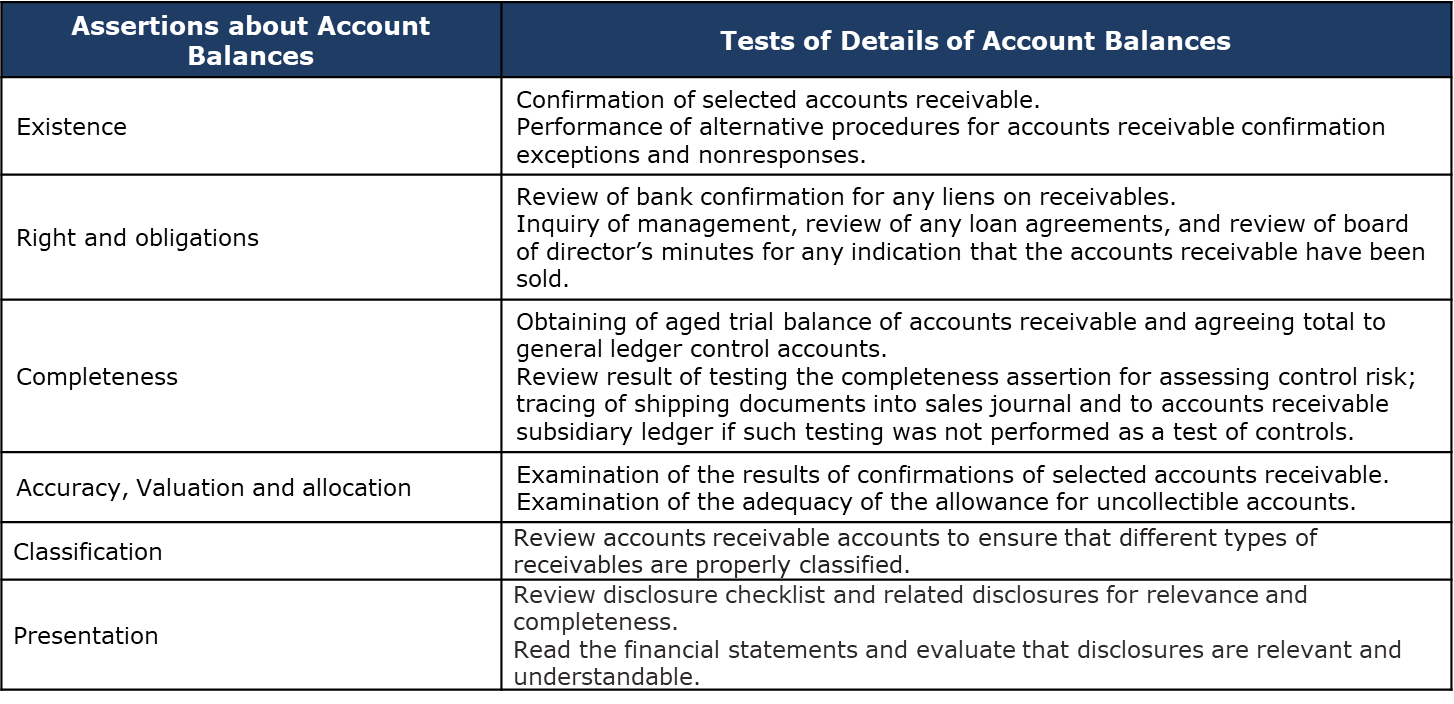

Tests of Details of Account Balances

For AR, allowance for uncollectible accounts, and bad debt expense:

Existence: we want to make sure that the balance exists – confirmations are the best way (high quality evidence)

Rights and obligations: we want to make sure we have the right to record the asset & make sure that from a receivable perspective, that none of that has happened – talk to management and look at bank confirmations/agreements, may be associated with loans & examine documentation

Completeness: we want to ensure that everything that should be recorded is recorded – Are there some transactions missing? Are there cash receipts missing because they’re being misappropriated?

Classification: ensure that no trade receivables are being recorded as a current asset when it should be a long-term asset

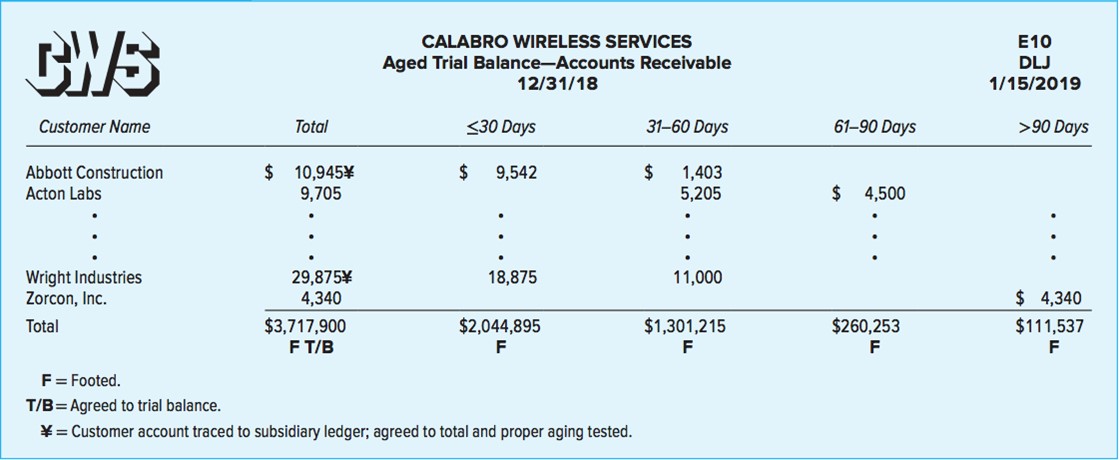

Exhibit 10.4 – example of an aged TB of AR working paper

Completeness

The auditor’s primary concern is whether all AR have been included in the AR subsidiary ledger and the GL AR account

Reconciliation of the aged TB to the GL account should detect an omission of a receivable from either the subsidiary or GL

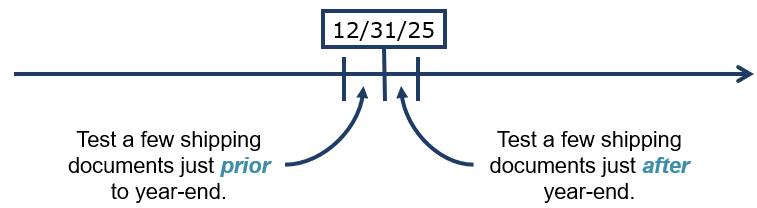

Cutoff

The cutoff test attempts to determine whether all revenue transactions and related accounts receivable are recorded in the proper period

Are all transactions tested recorded in the proper period?

Existence and Rights and Obligations

Existence is one of the more important assertions for accounts receivable because the auditor wants assurance that this account balance is not overstated through the inclusion of fictitious customer accounts or amounts

Confirmation is the major audit procedure used for testing this assertion

The auditor must determine that all accounts receivables are owned by the entity

This is usually not a problem, however, in some cases, accounts receivable may be sold or factored with or without recourse

Accuracy, Valuation, and Allocation

AR should be shown on the BS at net realizable value (gross amount less allowance for uncollectible accounts)

The auditor must verify the adequacy of the allowance for uncollectible accounts

The first step is to prepare an aged trial balance and discuss results with the credit manager

Next, a comparison with last year’s results should be examined

Classification

The major issues related to presentation disclosure, and classification are:

(1) Identifying and reclassifying any material credits contained in AR

(2) Segregating ST and LT receivables

(3) Ensuring that different types of receivables are properly classified

Presentation

The auditor must ensure that all necessary disclosures are made

Most public accounting firms use some type of FS reporting checklist to ensure that all necessary disclosures are made for each account

The Confirmation Process – AR

Confirmation is audit evidence that is a direct written response from third parties about the account receivable balance

Confirmation is a good source of evidence about the existence of the AR

The confirmation process should be controlled by the auditor

Omitting Confirmations

AR balance is immaterial

External confirmations would be ineffective

The auditor’s assessed level of risk of material misstatement at the relevant assertion level is low, and the other planned substantive procedures address the assessed risk

Factors Affecting the Reliability of AR Confirmations

(1) Type of confirmation request (positive versus negative)

(2) Prior experience with the client or similar engagements (ex: response rate, accuracy of returned confirmations, misstatements identified)

(3) The intended respondent (competence, knowledge, ability, and objectivity)

Types of Confirmations

Positive Confirmation – requests that customers indicate whether they agree with the amount due to the client

A response is expected whether the customer agrees or disagrees with the balance indicated

Negative Confirmation – requests that the customer respond only when they disagree with the amount due to the client

Negative confirmations are used when the client has many small account balances and control risk is assessed as low

Timing

AR may be confirmed at an interim date or at year-end

The confirmation request should be sent soon after the end of the accounting period in order to maximize the response rate

Confirmation Procedures

The auditor should mail the confirmation requests outside the entity’s facilities

A record should be maintained of the confirmations mailed and those returned

A second request may be necessary in some cases.

For each exception received, the auditor should examine the reasons for the difference between the balance on the client’s books and the balance indicated by the customer

In many cases, exceptions result from what are referred to as timing differences

Such differences occur because of delays in recording transactions in either the client’s or the customer’s records

Alternative Procedures

When the auditor does not receive responses to positive confirmations, alternative audit procedures are used

These alternative procedures include:

(1) Examination of specific subsequent cash receipts

(2) Examination of shipping documentation

(3) Examination of other client documentation

Auditing Other Receivables

Other types of receivables that are reported on the balance sheet may include:

Receivables from officers and employees

Receivables from related parties

Notes receivable

The auditor’s concern with satisfying the assertions for these receivables is like that for trade accounts receivable

Each of these types of receivables is confirmed and evaluated for collectability

The transactions that result in receivables from related parties are examined to determine if they were at “arm’s length”

Notes receivable would also be confirmed and examined for repayment terms and whether interest income has been properly recognized

Evaluating the Audit Findings – Revenue Related Accounts

When the auditor has completed the planned substantive procedures, the likely misstatement (projected misstatement plus an allowance for sampling risk) for accounts receivable is determined

Aggregate misstatement < tolerable misstatement = accept the account as fairly represented

Aggregate misstatement > tolerable misstatement = account is not fairly presented