B4555 - Chapter 01

Introduction to Assurance and FS Auditing

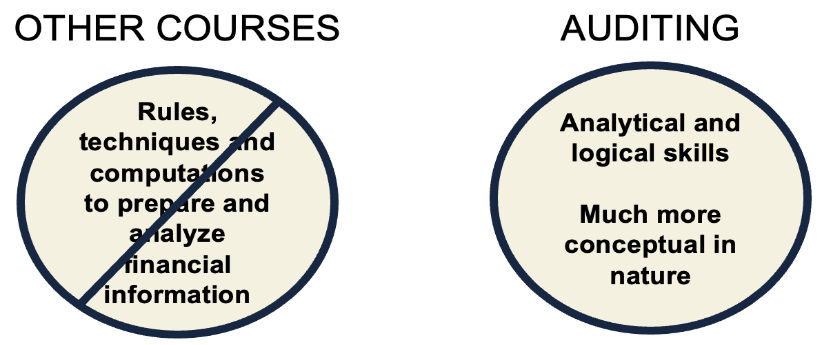

The Study of Auditing

|

|

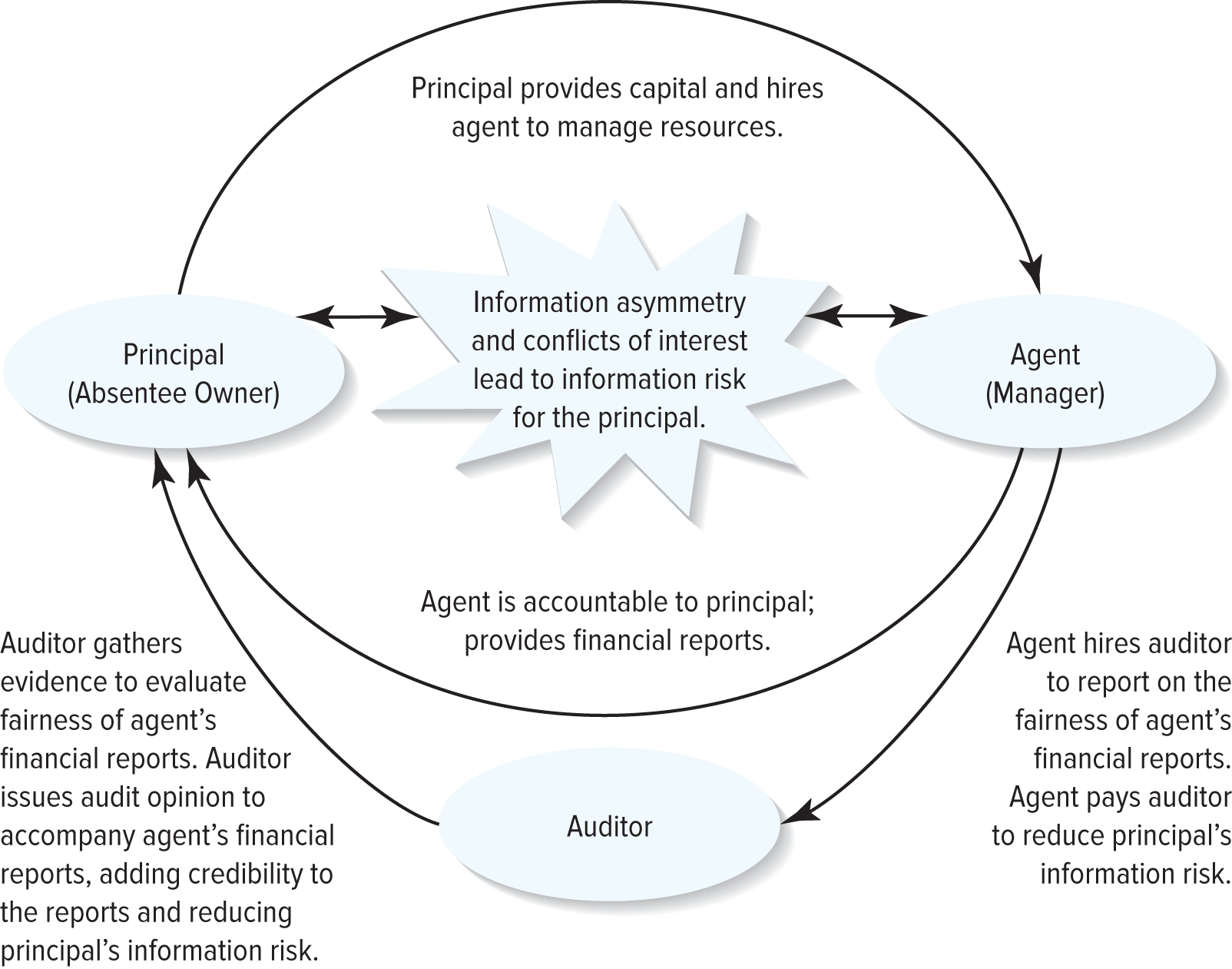

The Demand for Auditing and Assurance

- Auditor helps to ensure that there is no info asymmetry

- What management is reporting to their investors/predators is real and fairly stated

- The development of the corporate form of business and the expanding world economy over the last 200 years have given rise to an explosion in the demand for assurance provided by auditors

- Why? Owners of the companies are no longer the “owners”

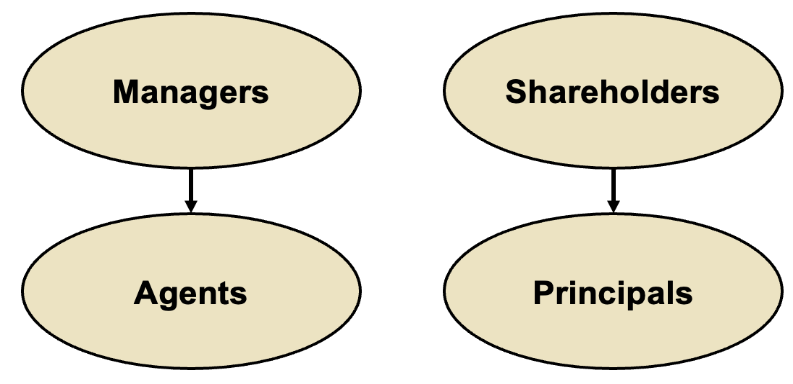

Principals and Agents

|

|

- There is a principal/agent relationship between shareholders and management

- Shareholders have a valid interest in the proper use of a company’s resources

- Management does not necessarily have the same goals as the shareholders

- The relationship between an owner and manager results in info asymmetry between the two parties

- Info asymmetry means that the manager has more info about the “true” financial position and results of operations of the entity than does the absentee owner

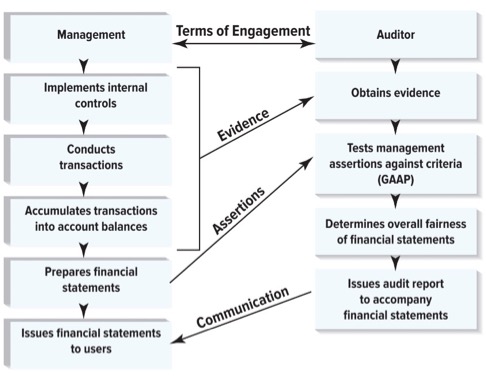

The Role of Auditing

|

|

Summary of Management Assertions by Category

- The role of auditing is to test management assertions about classes of transactions and events for the period under audit, about account balances at the period end, and related disclosures for transactions and balances

An auditor performs a vouching test on A/R by looking through the general ledger, identifying sample accounts, and finding original supporting documentation for those balances. This test deals with which of the following management assertions? |

- Existence

- Occurrence

- Completeness

- Accuracy, valuation, and allocation

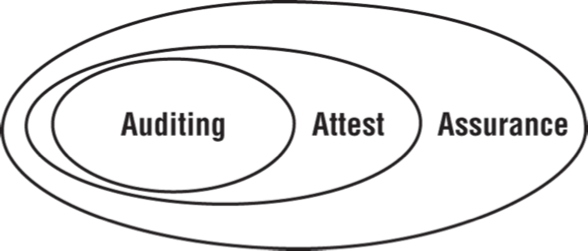

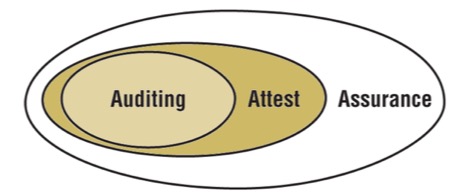

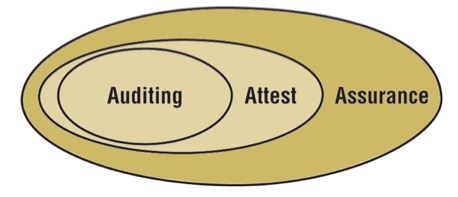

Relationships among Auditing, Attest, and Assurance Services

|

|

Auditing, Attest, and Assurance Services Defined

|

|

|

|

|

|

Fundamental Concepts in Conducting a F/S Audit

Audit Assertions/Objectives

- B/S assertions:

- Valuation

- Existence

- Rights and obligations

- Completeness

- I/S assertions:

- Completeness

- Accuracy

- Cut-off

- Classification

- Occurrence

- The audit assertions are sometimes called objectives and are similar to the management assertions

- Minor differences: authorization is not an audit assertion

|

|

Fundamental Concepts in Conducting a F/S Audit

These concepts drive our study of auditing

These concepts drive our study of auditing

Materiality

- Materiality is the magnitude of an omission or misstatement of accounting info that makes it probable that the judgment of a reasonable person relying on the info would have been changed or influenced by the omission or misstatement

- Ex: Garden Centre purchase a garbage can for $15

- This is an asset and ideally capital assets are depreciated

- In other words, materiality is an amount that will not impact the opinion of the F/S

- Ex: Garden Centre purchase a garbage can for $15

- An auditor’s first task in planning an audit is to make a judgement about how big a misstatement would have to be before it would significantly affect users’ judgements

- Common rule of thumb: total (aggregated) misstatements of more than about 5% of income before tax would cause the F/S to be materially misstated

Audit Risk

- Note: more detail in chapter 3

- Audit risk is the risk that the auditor mistakenly expresses a clean audit opinion when the F/S are materially misstated

- In other words, audit risk is the risk that an auditor will express on a decision

- This can never be 0 because auditors can’t audit every transaction of an organization

- Auditing standards make it clear that the audit provides only reasonable assurance that the F/S do not contain material misstatements

- Reasonable assurance implies some risk that a material misstatement could be present in the F/S and the competent auditor will fail to detect it

Which of the following best describes the concept of audit risk? |

- The risk of the auditor being sued because of association with an auditee

- The risk that the auditor will provide an unqualified opinion on F/S that are, in fact, materially misstated

- The overall risk that a material misstatement exists in the F/S

- The risk that auditors use audit procedures that are inappropriate

Audit Evidence Regarding Management Assertions

- Audit evidence is evidence that assists the auditor in evaluating management’s F/S assertions consists of the underlying accounting data and any additional info available to the auditor, whether originating from the client or externally

- Relevance is the evidence related to the specific assertion being tested

- Reliability is whether the evidence be relied upon to signal the true state of the specific assertion being tested

- We must have enough evidence to prove our opinion

Sampling: Inferences Based on Limited Observations

- Auditors use a sampling approach to examine a subset of the transactions based on previous audits, an understanding of the company’s internal control system, or knowledge of the company’s industry

- It would be too costly for the auditor to examine every transaction

- Data analytics will sometimes allow for testing entire populations

Why do auditors generally use a sampling approach to evidence gathering? |

- Auditors are experts and do not need to look at much to know whether the F/S are correct or not

- Auditors must balance the cost of the audit with the need for precision

- Auditors must limit their exposure to their auditee to maintain independence

- The auditor's relationship with the auditee is generally adversarial, so the auditor will not have access to all of the financial info of the company

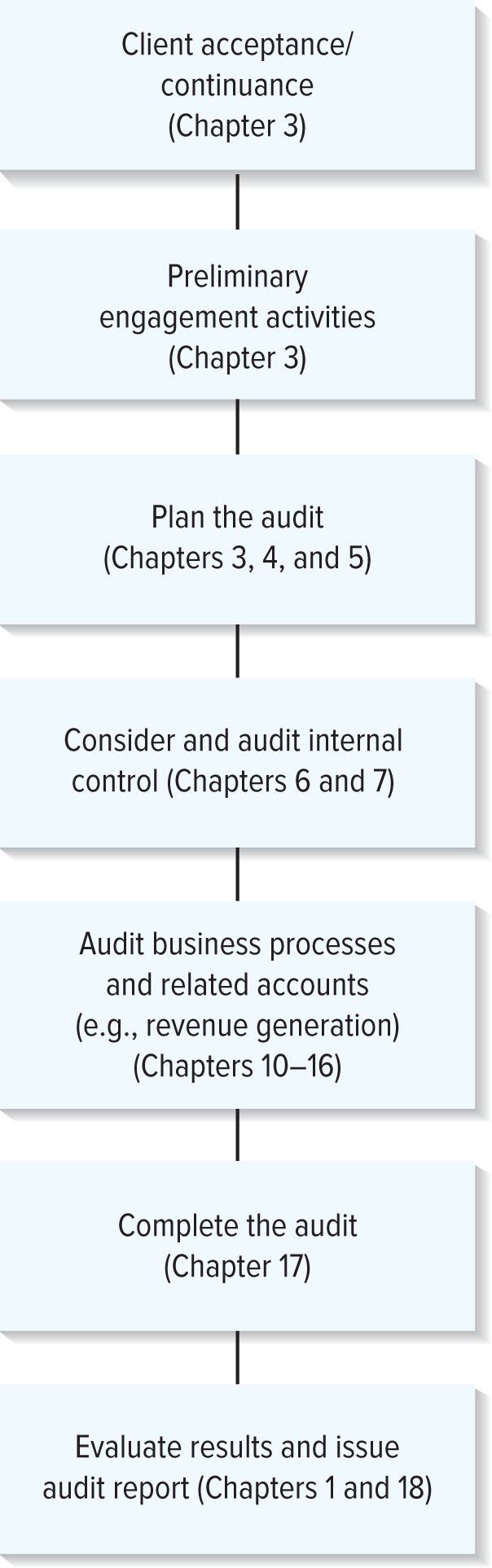

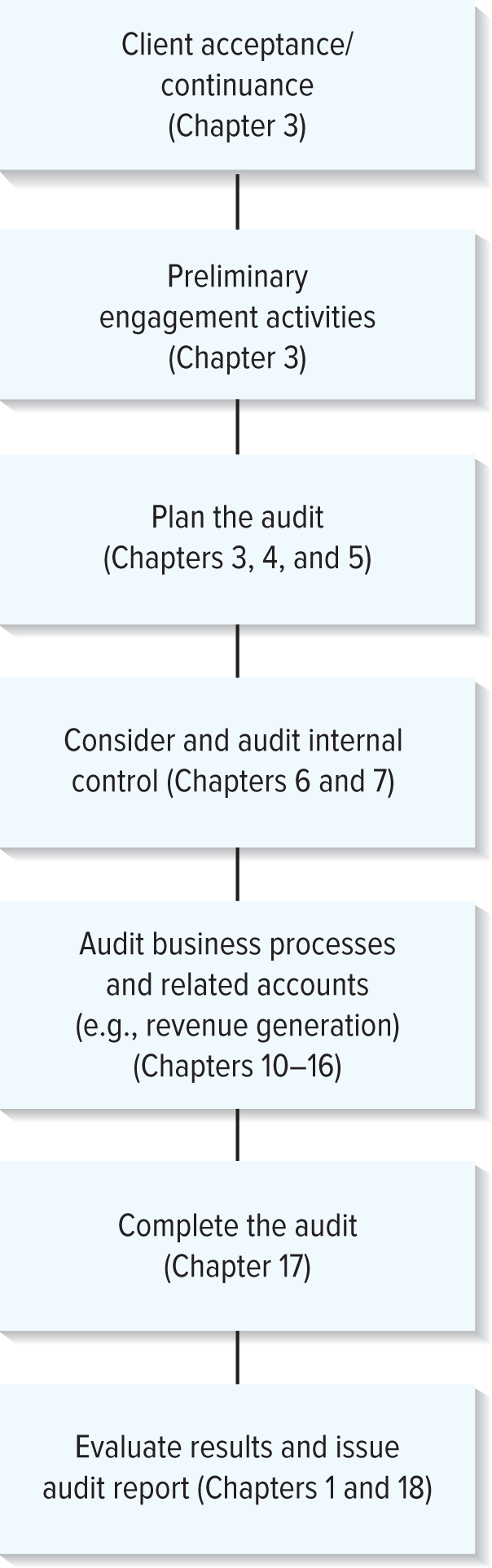

The Audit Process

Major Phases of an Audit

|

|

Structure of the Audit Report

- For public company audits, the title line of the audit report includes “Independent Auditor’s Report”

- Usually, the report is addressed to the shareholders and board of directors of the company

- The audit report includes sections titled:

- “Opinion on the Financial Statements”

- “Basis for Opinion”

- “Critical Audit Matters”

- An explanatory paragraph with the auditor’s opinion of internal controls, if the report on internal controls is included in a separate report

- Concludes with:

- Signature in the name of the audit firm

- The personal name of the auditor, or both, as appropriate

- Auditor addressee

- Date of report

Types of Audit Reports

- The auditor’s report (audit opinion) is the main product or output of the audit

Unqualified

- The standard unqualified (clean) audit report is the most common type of report issued

- In this context, unqualified means that because the F/S are free of material misstatements, the auditor does not find it necessary to qualify his or her opinion about the fairness of the F/S

Qualified

- Suppose an auditee’s F/S contain a misstatement that the auditor considers material and management refuses to correct the misstatement or suppose that the auditor is unable to obtain sufficient appropriate evidence regarding a specific account

- The auditor will likely qualify the report, explaining that the F/S are fairly stated except for the misstatement identified by the auditor

Adverse

- Suppose an auditee’s F/S contain a misstatement that the auditor considers so material that it pervasively affects the interpretation of the F/S

- Given such a situation, the auditor will issue an adverse opinion, indicating that the F/S are not fairly stated and should not be relied upon

Disclaimer

- If a scope limitation is so pervasive that it limits the ability of the auditor to conclude on the F/S as a whole, the auditor will issue a “disclaimer of opinion,” indicating that it is not possible to express an opinion on the fairness of the F/S

An investor is reading the F/S of the Stankey Corporation and observes that the statements are accompanied by an auditor's unqualified report. From this, the investor may conclude that: |

- Any disputes over significant accounting issues have been settled to the auditor's satisfaction

- The auditor is satisfied that Stankey will be highly profitable in the future

- The auditor is certain that Stankey's F/S have been prepared accurately and that all account balances are precisely correct

- The auditor has determined that Stankey's management is not qualified to lead the company

Auditing Demands Logic, Reasoning, and Resourcefulness

- An auditor needs to understand more than just the accounting concepts and techniques

- Auditing is a fundamentally logical process of thinking and reasoning – so use your common sense and reasoning skills

- As you learn new auditing concepts, try to understand the underlying logic and how the concepts interrelate with other concepts

- Being a good auditor requires imagination and innovation

- Understanding audit concepts is useful for all business professionals, consultants, and etc.