Economics Flashcards

Background to Supply

Short-run Theory of Production

Profits and Aims of the Firm:

Traditional and alternative theories.

In the short run, firms aim to maximize profits by analyzing production functions and understanding the relationship between input variables and output.

Long-run vs. Short-run Production:

Fixed and variable factors of production.

Law of Diminishing Returns:

When increasing amounts of a variable factor are used with a given amount of a fixed factor, there will come a point when each extra unit of the variable factor will produce less extra output than the previous unit.

Short-run Production Function

Total Physical Product (TPP)

Average Physical Product (APP)

APP={TPP}/{QV}

Marginal Physical Product (MPP)

MPP={\Delta TPP}/{\Delta QV}

Example: Wheat Production

Number of Workers (Lb) | TPP (tonnes) | APP (=TPP/Lb) | MPP (=ΔTPP/ΔLb) |

|---|---|---|---|

0 | 0 | – | – |

1 | 3 | 3 | 3 |

2 | 10 | 5 | 7 |

3 | 24 | 8 | 14 |

4 | 36 | 9 | 12 |

5 | 40 | 8 | 4 |

6 | 42 | 7 | 2 |

7 | 42 | 6 | 0 |

8 | 40 | 5 | -2 |

Graphical Relationship

Relationship between TPP, APP, and MPP is shown graphically.

TPP increases with the number of farm workers up to a point, then declines.

Diminishing returns set in at a certain point.

MPP illustrates the change in TPP with each additional worker.

Short-run Costs

Measuring Costs of Production:

Fixed Costs: Costs that do not change with the level of output, such as rent and salaries.

Variable Costs: Costs that vary with the level of production, including raw materials and labor.

Total Costs: The sum of fixed and variable costs at a given level of output.

Explicit Costs

These are direct, out-of-pocket expenses that a firm incurs during the production process, such as wages, rent, and material costs.

Implicit Costs

These represent the opportunity costs of utilizing resources owned by the firm, reflecting the income that could have been earned if those resources were employed in their next best alternative use.

Fixed Costs and Variable Costs:

Fixed Costs and Sunk Costs

Total Costs:

Total Fixed Cost (TFC)

Total Variable Cost (TVC)

Total Cost (TC)

TC = TFC + TVC

Example: Total Costs for Firm X

Output (Q) | TFC (£) | TVC (£) | TC (£) |

|---|---|---|---|

0 | 12 | 0 | 12 |

1 | 12 | 10 | 22 |

2 | 12 | 16 | 28 |

3 | 12 | 21 | 33 |

4 | 12 | 28 | 40 |

5 | 12 | 40 | 52 |

6 | 12 | 60 | 72 |

7 | 12 | 91 | 103 |

Cost Curves

TFC is constant regardless of output.

TVC increases with output.

TC is the sum of TFC and TVC.

Diminishing marginal returns affect the shape of TVC and TC.

Marginal Cost (MC)

Marginal Cost and the Law of Diminishing Returns

Relationship between Marginal and Total Cost Curves

Average Costs

Average Fixed Cost (AFC)

Average Variable Cost (AVC)

Average (Total) Cost (AC)

Relationship between AC and MC

Example: Total, Average, and Marginal Cost for Firm X

Output (Q) | TFC (£) | AFC (£) | TVC (£) | AVC (£) | TC (£) | AC (£) | MC (£) |

|---|---|---|---|---|---|---|---|

0 | 12 | – | 0 | – | 12 | – | – |

1 | 12 | 12 | 10 | 10 | 22 | 22 | 10 |

2 | 12 | 6 | 16 | 8 | 28 | 14 | 6 |

3 | 12 | 4 | 21 | 7 | 33 | 11 | 5 |

4 | 12 | 3 | 28 | 7 | 40 | 10 | 7 |

5 | 12 | 2.4 | 40 | 8 | 52 | 10.4 | 12 |

6 | 12 | 2 | 60 | 10 | 72 | 12 | 20 |

7 | 12 | 1.7 | 91 | 13 | 103 | 14.7 | 31 |

AFC decreases as output increases.

AVC, AC, and MC are U-shaped due to diminishing returns.

MC intersects AC at its minimum point.

Long-run Theory of Production

All factors variable in the long run.

Scale of Production:

Increasing Returns to Scale

Constant Returns to Scale

Decreasing Returns to Scale

Economies of Scale

Specialization and Division of Labor

Indivisibilities

Container Principle

Greater Efficiency of Large Machines

By-products

Multi-stage Production

Organizational and Administrative Economies

Financial Economies

Economies of Scope

Diseconomies of Scale

Managerial Complexity

Alienation

Industrial Relations Problems

Disruption if part of complex production chains fail

External Economies and Diseconomies of Scale

Location

Costs vary in different locations

Transport Costs: Location relative to market and suppliers

Optimum Combination of Factors

Two-factor case:

If{MPPa}/{Pa}>{MPPb}/{Pb} costs can be reduced by using more factor a and less factor b.

Costs minimized where: MPPa/Pa = MPPb/Pb

Multi-factor case:

Costs minimized where: MPPa/Pa= MPPb/Pb = … MPPn/Pn

(the equi-marginal principle)

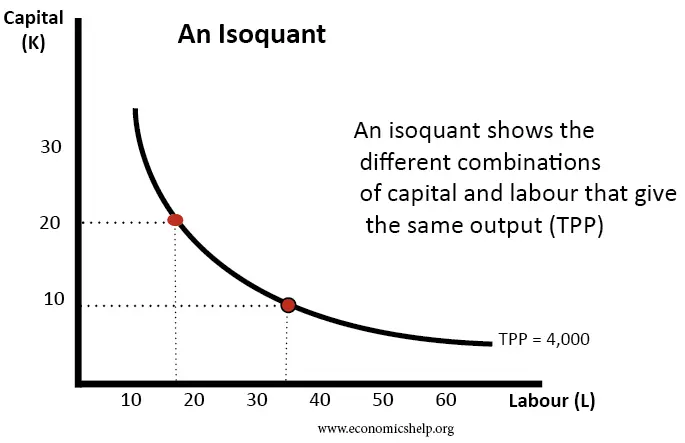

Isoquant-Isocost Analysis

Isoquants

Shape of isoquants.

Diminishing Marginal Rate of Substitution (MRS)

Isoquant Map

Diminishing Marginal Rate of Substitution (MRS)

MRS = frac{\Delta K}{\Delta L}

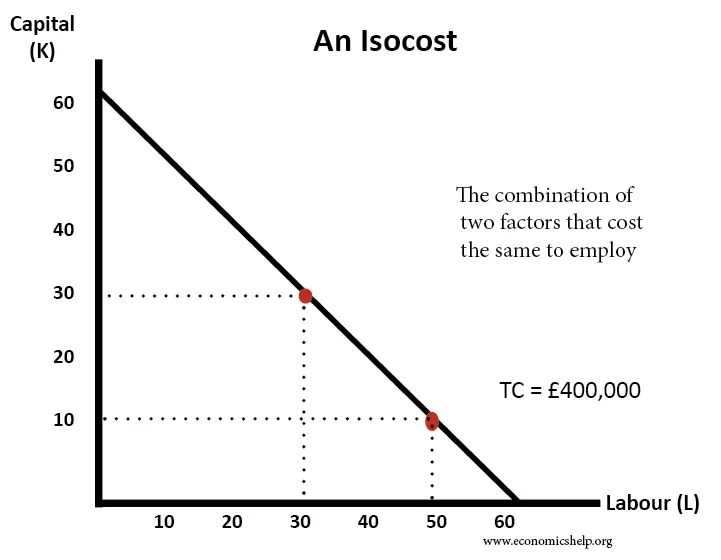

Isocosts

Slope and position of the isocost.

Shifts in the isocost.

Least-cost Combination of Factors for a Given Output

Point of Tangency

Comparison with Marginal Productivity Approach

Highest Output for a Given Cost of Production

Long-run Costs

Long-run Average Costs (LRAC)

Shape of the LRAC curve.

Assumptions behind the curve.

Alternative LRAC Curves

Economies of Scale

Diseconomies of Scale

Constant Costs

Long-run Marginal Costs (LRMC)

Relationship between Long-run and Short-run Average Costs

The Envelope Curve

Revenue

Defining Total, Average, and Marginal Revenue

Revenue Curves When Firms Are Price Takers (Horizontal Demand Curve)

Average Revenue (AR)

Marginal Revenue (MR)

Total Revenue (TR)

Revenue Curves When Price Varies with Output (Downward-Sloping Demand Curve)

Average Revenue (AR)

Marginal Revenue (MR)

Total Revenue (TR)

Revenue Curves and Price Elasticity of Demand

Shifts in Revenue Curves

Profit Maximisation

Using Total Curves

Maximizing difference between TR and TC

The Total Profit Curve

Using Marginal and Average Curves

Stage 1: Profit Maximized where MR = MC

Stage 2: Using AR and AC Curves to Measure Maximum Profit

Some Qualifications

Long-run Profit Maximization

The Meaning of Profit

What if a Loss Is Made?

Loss Minimizing: Still Produce where MR = MC

Short-run Shut-down Point: P = AVC

Long-run Shut-down Point: P = LRAC