B4555 - Chapter 6-10

Internal Control in a Financial Statement Audit

October 20, 2023

Internal Control

- Note: we only need to test internal controls if we need to rely on them

- Ultimately, we want to test control risk 🡪 audit risk = IR*CR*DR where RMM = IR*CR

- Management has the responsibility to maintain controls that provides reasonable assurance that adequate control exists over the entity’s assets and records

- The internal control system should …

- (1) Ensure that assets and records are safeguarded

- (2) Generate reliable info for decision making

- The auditor needs assurance about the reliability of the data generated by the info system

- The auditor uses risk assessment procedures to …

- (1) Obtain an understanding of the entity’s internal control

- (2) Identify key controls

- (3) Recognize the types of potential misstatements

- (4) Design tests of controls and substantive procedures

- There is an inverse relationship between the reliability of internal control and the amount of substantive evidence required by the auditor

- The auditor’s understanding of the internal control is a major factor in determining the overall audit strategy

- The auditor has the responsibility to …

- (1) Obtain an understanding of internal controls

- (2) Assess control risk

Definition of Internal Control

- The purpose of its framework is to help management better achieve the organization’s objectives and provide board of directors an added ability to oversee internal control

- An effective system of internal control allows management to focus on operations and financial performance goals while maintaining compliance with relevant laws and minimizing surprises

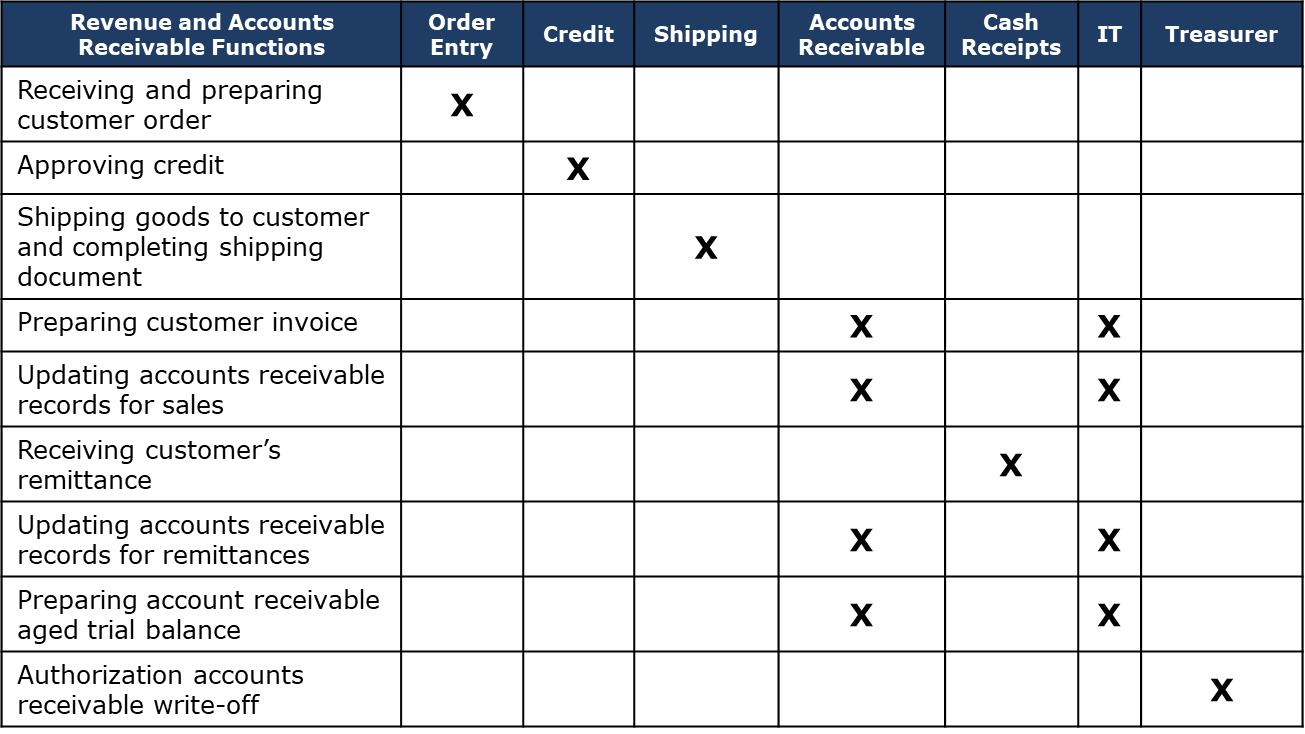

Controls Relevant to the Audit

- The controls that are of most direct relevance to a F/S audit are those that contribute to the reliability, timeliness, and transparency of external financial reporting

- These controls are relevant to an audit because they help to prevent, or detect and correct, material misstatements in the entity’s F/S

- Controls relating to operations and compliance objectives may be relevant when they relate to data the auditor uses to apply auditing procedures

The Effect of Info Technology on Internal Control

- The extent of an entity’s use of IT can affect internal control because IT affects the way transactions are initiated, authorized, recorded, processed, and reported

- Controls in most info systems consist of a combination of …

- (1) Interdependent automated

- (2) Manual controls

Table 6.1 – the effect of info technology on internal control

Benefits:

Risks:

|

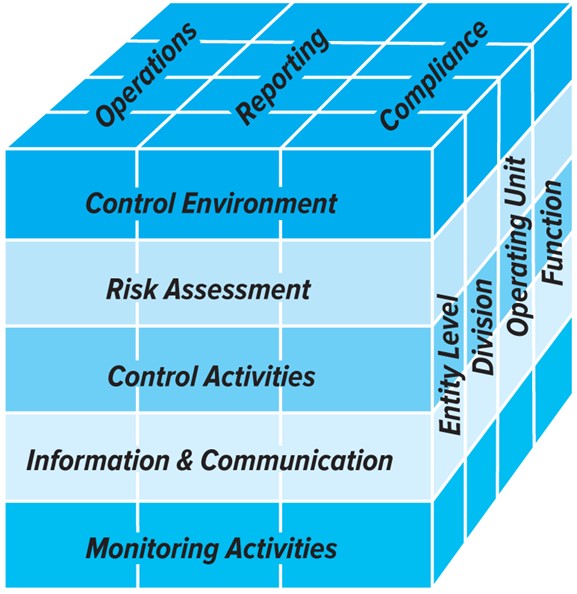

The COSO Framework

Components of Internal Control

- Note: this is the first step to assessing your controls

- (1) Control environment is the set of standards, processes, and structures that provides the basis for carrying out internal control across the organization

- The board of directors and senior management establish the tone at the top regarding the importance of internal control and expected standards of conduct

- (2) Entity’s risk assessment process involves a dynamic and iterative process for identifying the entity’s objectives, thereby forming a basis for determining how risks should be managed

- Management considers possible changes in the external environment and within its own business model that may impede its ability to achieve its objectives

- (3) Control activities are the actions established by policies and procedures to help ensure that management commands to mitigate risks to the achievement of objectives are carried out

- Control activities are performed at all levels of the entity and at various stages within the business processes, and over the technology environment

- (4) Info and communication

- Information is necessary for the entity to carry out internal control responsibilities in support of achievement of its objectives

- Communication occurs both internally and externally and provides the organization with the info needed to carry out day-to-day internal control activities

- Enables personnel to understand internal control responsibilities and their importance to the achievement of objectives and allows for upward flow of operating info to management

- (5) Monitoring activities

- Ongoing evaluations, separate evaluations, or some combination of the two are used to ascertain whether each of the 5 components of internal control, including controls to affect the principles within each component, are present and functioning

- Findings are evaluated and deficiencies are communicated in a timely manner, with serious matters reported to senior management and to the board

| Figure 6.1 – components of internal control

|

The 17 Principles Underlying the Components of Internal Control

Control Environment

- Principle 1: The organization demonstrates a commitment to integrity and ethical values

- Principle 2: The board of directors demonstrates independence from management and exercises oversight of the development and performance of internal control

- Principle 3: Management establishes, with board oversight, structures, reporting lines, and appropriate authorities and responsibilities in the pursuit of objectives

- Principle 4: The organization demonstrates a commitment to attract, develop, and retain competent individuals in alignment with objectives

- Principle 5: The organization holds individuals accountable for their internal control responsibilities in the pursuit of objectives

The Entity’s Risk Assessment Process

- The risk assessment process identifies and responds to business risks in relation to achieving business objectives

- Principle 6: The organization specifies objectives with sufficient clarity to enable the identification and assessment of risks relating to objectives

- Principle 7: The organization identifies risks to the achievement of its objectives across the entity and analyzes risks as a basis for determining how the risks should be managed

- Principle 8: The organization considers the potential for fraud in assessing risks to the achievement of objectives

- Principle 9: The organization identifies and assesses changes that could significantly impact the system of internal control

Control Activities

- Control activities involve policies and procedures that help mitigate risks that endanger the achievement of objectives

- Principle 10: The organization selects and develops control activities that contribute to the mitigation of risks to the achievement of objectives to acceptable levels

- Performance reviews

- Physical controls

- Segregation of duties

- Info processing controls

- Principle 11: The organization selects and develops general control activities over technology to support the achievement of objectives

- General controls relate to the overall info processing environment and include controls over data center and network operations

- Application controls apply to the processing of individual applications and help ensure the occurrence (validity), completeness, and accuracy of transaction processing

- Principle 12: The organization deploys control activities through policies that establish what is expected and procedures that put policies into action

- A policy is a rule or guideline that calls for certain activities to take place in certain circumstances

Info and Communication

- Principle 13: The organization obtains or generates and uses relevant, quality info to support the functioning of internal control

- Identify and record all valid transactions

- Classify transactions properly

- Measure the value of transactions properly

- Record transactions in the proper period

- Properly present transactions and disclosures

- Principle 14: The organization internally communicates info, including objectives and responsibilities for internal control, necessary to support the functioning of internal control

- Principle 15: The organization communicates with external parties regarding matters affecting the functioning of internal control

Monitoring of Controls

- Monitoring of controls is a process that assesses the quality of internal control performance over time

- Principle 16: The organization selects, develops, and performs ongoing and/or separate evaluations to ascertain whether the components of internal control are present and functioning

- Principle 17: The organization evaluates and communicates internal control deficiencies in a timely manner to those parties responsible for taking corrective action, including senior management and the board of directors, as appropriate

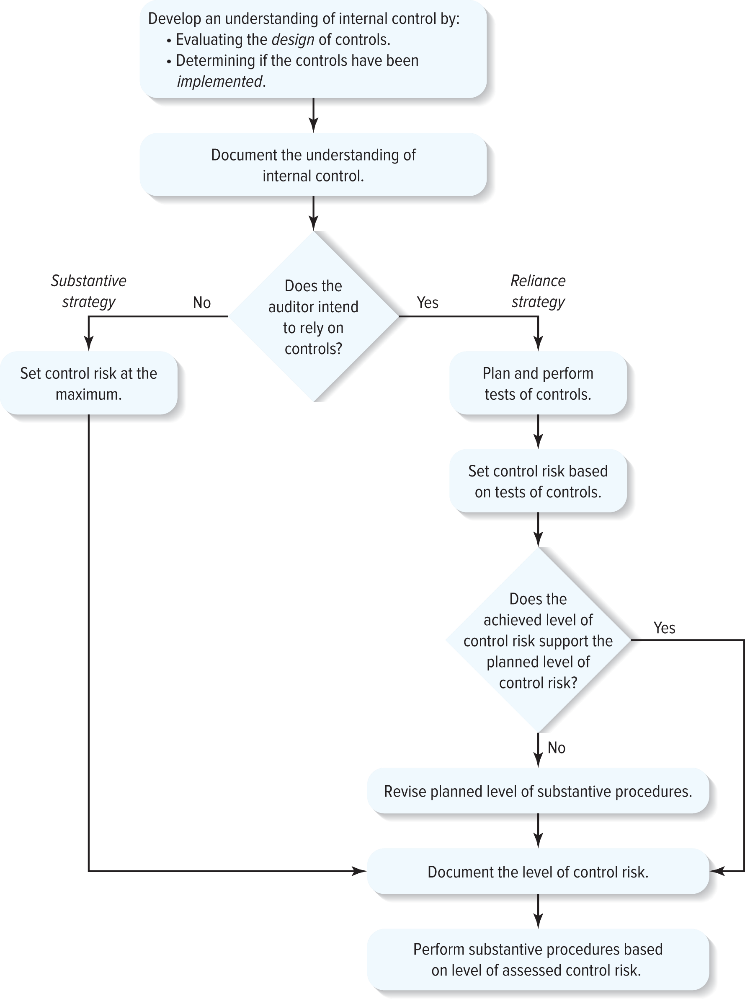

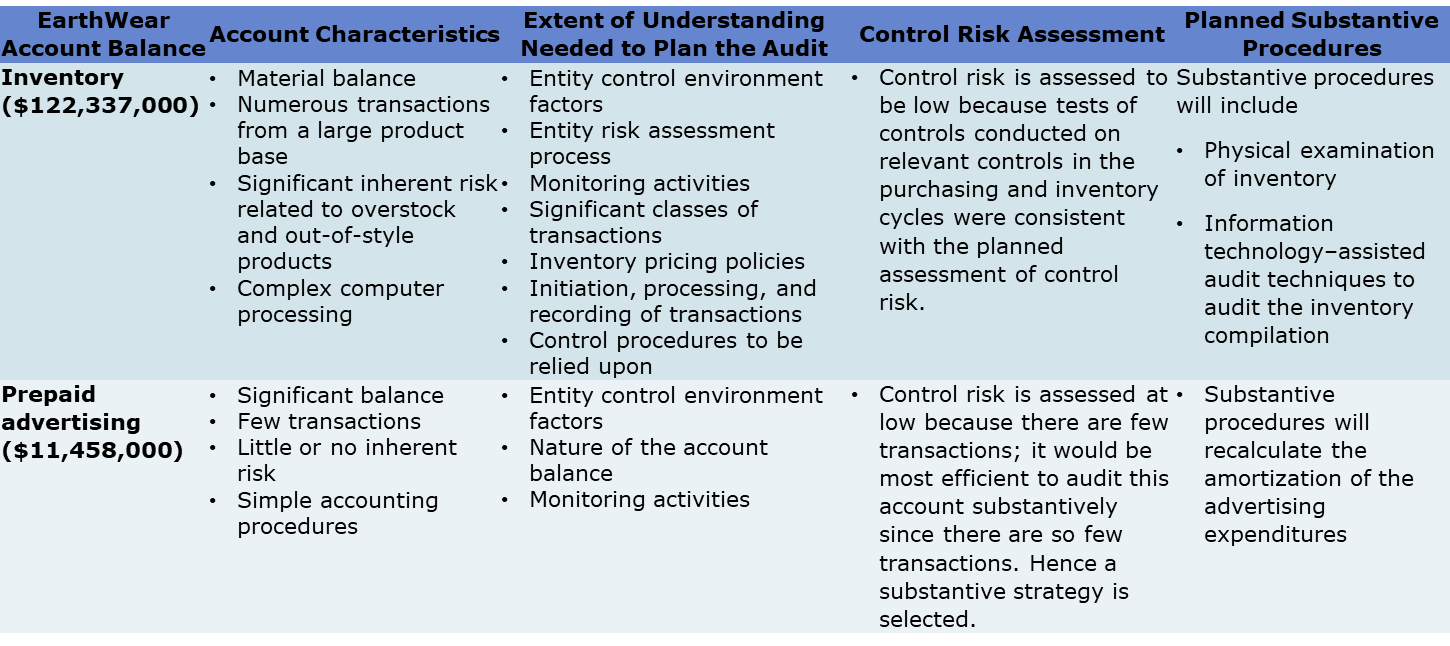

Planning an Audit Strategy

- Audit risk model: AR = RMM*DR where RMM = IR*CR

- The auditor’s assessment of RMM must consider the level of CR in applying the audit risk model

- If IR and CR are high, then DR is low = more substantive evidence

- In applying the audit risk model, the auditor must assess control risk

- Step 1: gather info by performing risk assessment procedures to evaluate the design of controls and to determine whether the controls have been implemented

- Step 2: decide whether to rely on the entity’s controls for assurance about management’s F/S assertions

- If the risk assessment procedures indicate that the controls are not properly designed or not implemented, the auditor will not rely on the controls – CR is set high, and the use of substantive procedures will be used to reduce the RMM to a low level

- If the risk assessment procedures suggest that the controls are properly designed and implemented – auditor will rely on the controls and tests of controls are required to be performed to obtain audit evidence that the controls are operating effectively

Figure 6.2 presents a flowchart of the auditor’s decision process when considering internal control in planning an audit

|

|

Substantive Strategy

- Strategy 1: substantive audit

- Understand what is there

- Document what is there

- It would be inefficient to take too much time to test these controls when we can say up front that these controls are not working

- Conclusion: no tests of controls evidence

- Auditor has decided not to rely on the entity’s controls and instead use substantive procedures as the main source of evidence about the assertions in the F/S

- After obtaining an understanding of internal control, an auditor may choose to follow a substantive strategy and set control risk at high for some or all assertions because of one or all the following factors:

- (1) Controls do not pertain to an assertion

- (2) Controls are assessed as ineffective

- (3) Testing the effectiveness of controls is inefficient

- Auditor documents the level of CR as being set at high and substantive procedures are designed and performed based on the assessment of a high level of CR

- When the auditor follows a substantive strategy, the assurance bucket is filled with some evidence from the risk assessment procedures and an extensive amount of evidence from substantive procedures

Reliance Strategy

- Strategy 2: combined approach

- Designed effectively

- Obtaining understanding of internal control

- Reliance strategy means the auditor plans to rely on internal control and assess control risk at a lower level

- The auditor uses the test results to assess the “achieved” level of control risk

- If the test results indicate that achieved CR > planned = auditor will increase the planned substantive procedures and document the revised CR assessment

- If tests of controls support the planned level of control risk, no revisions of the planned substantive procedures are required

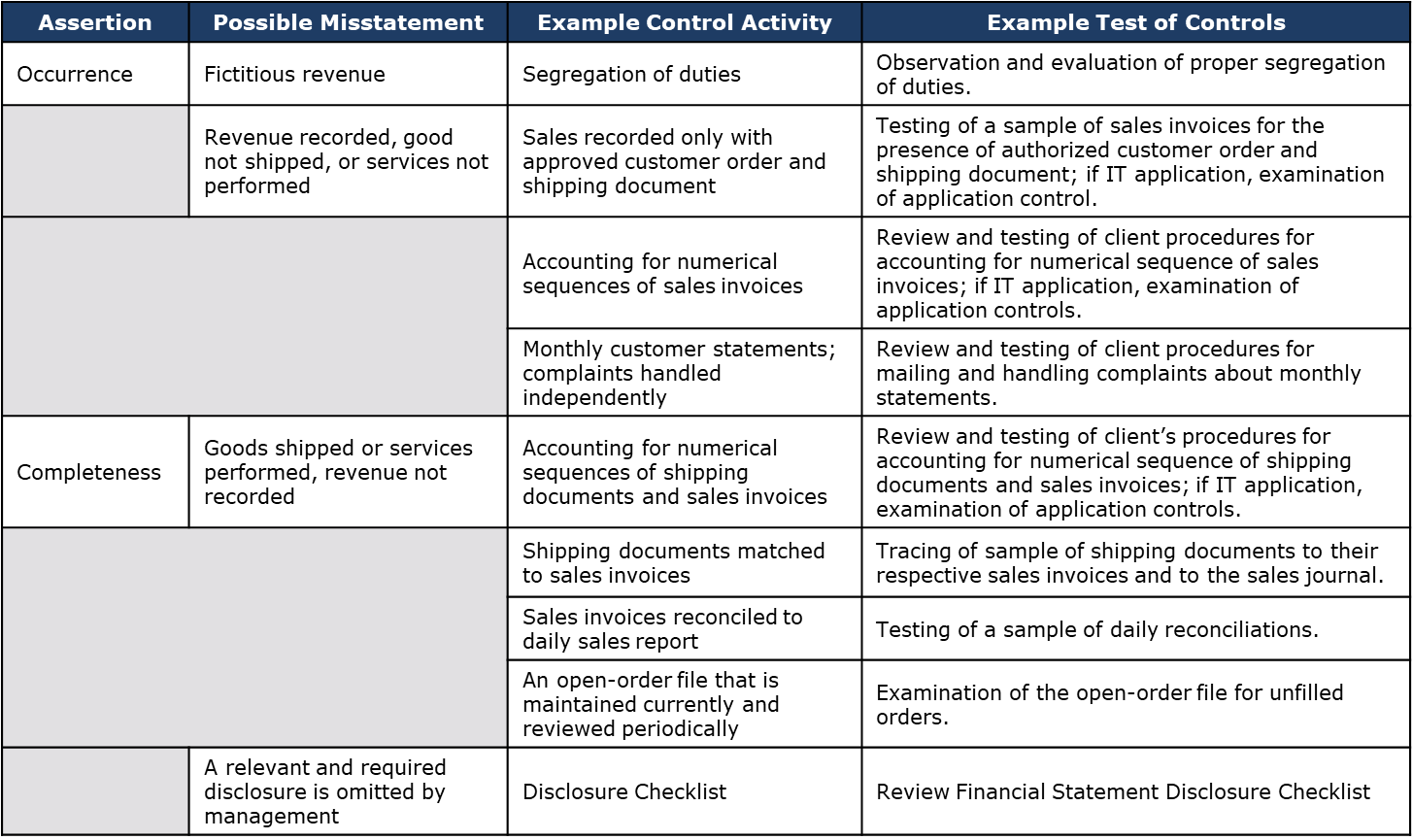

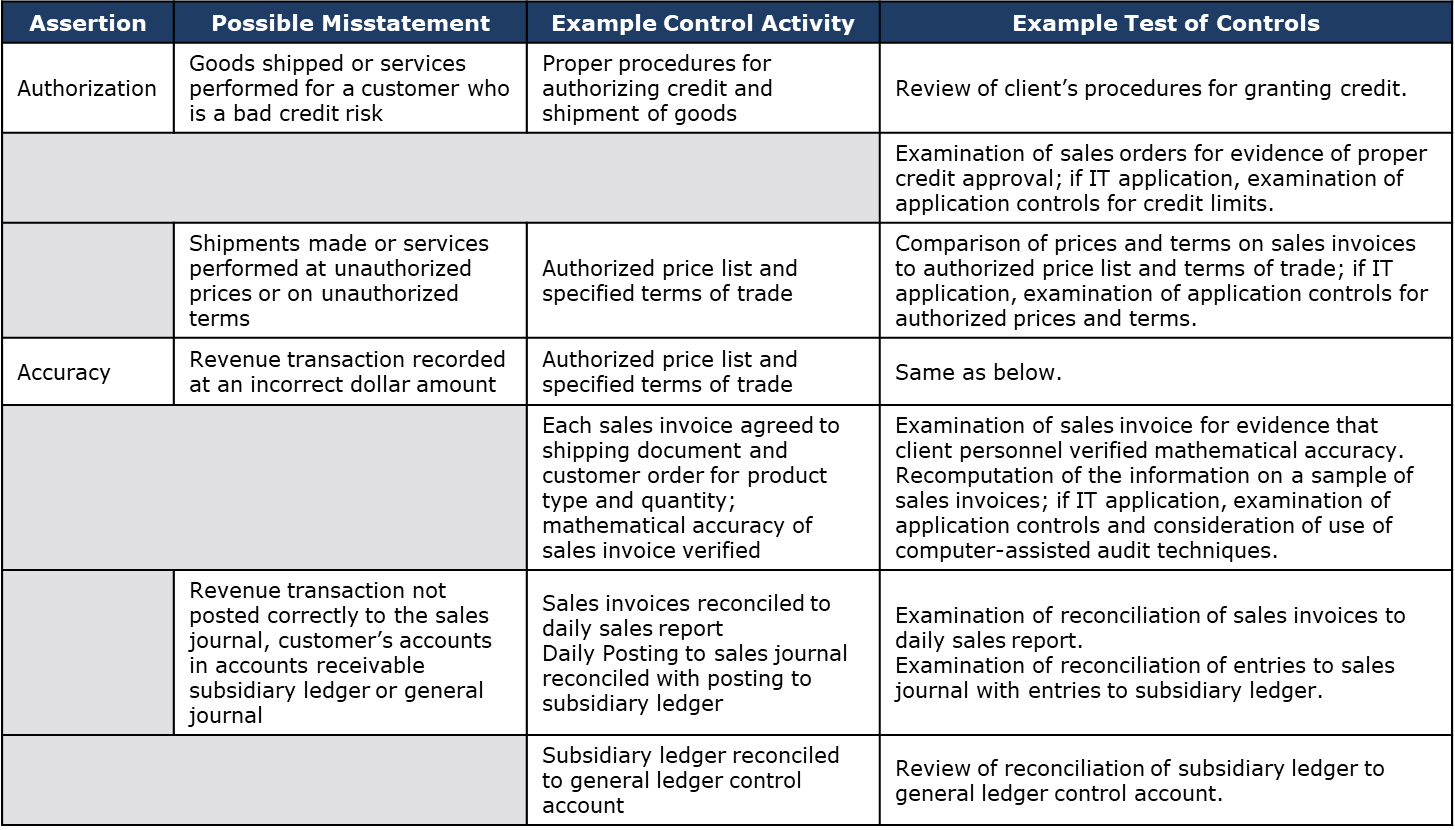

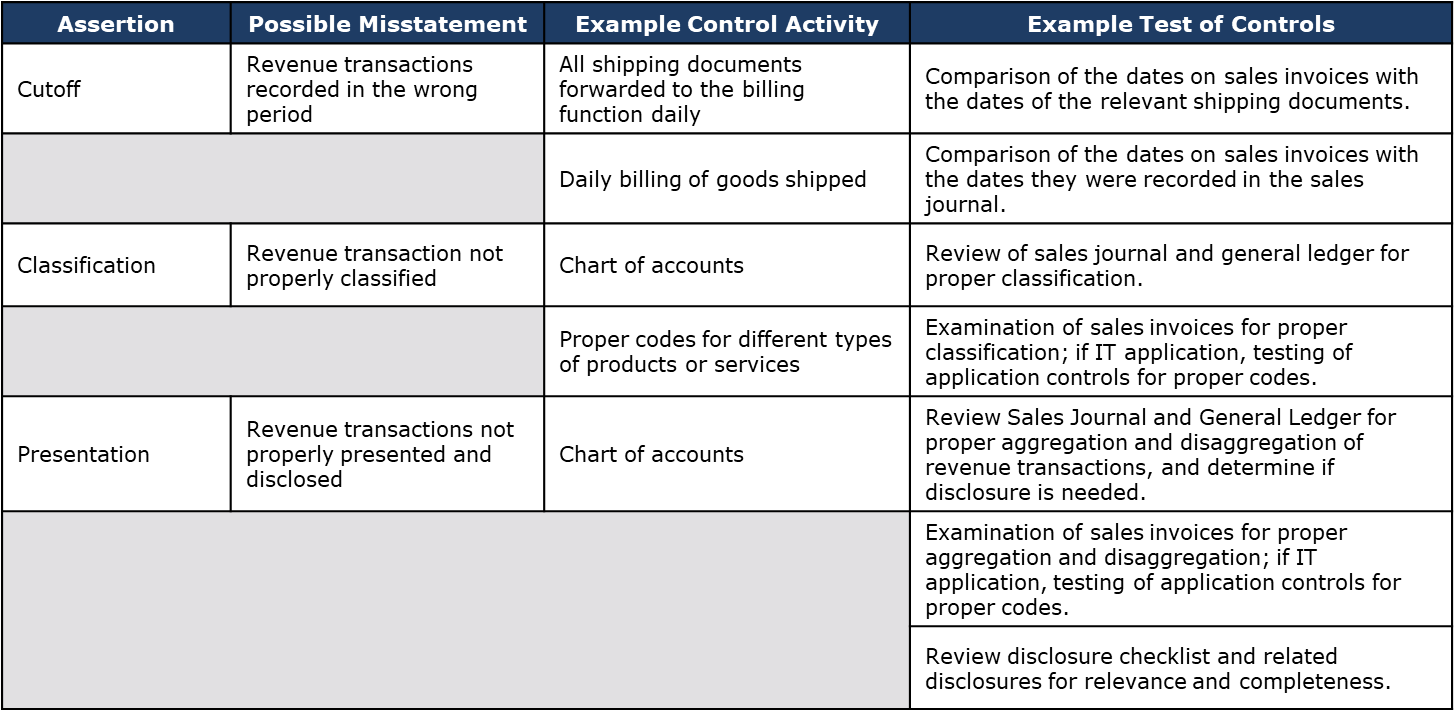

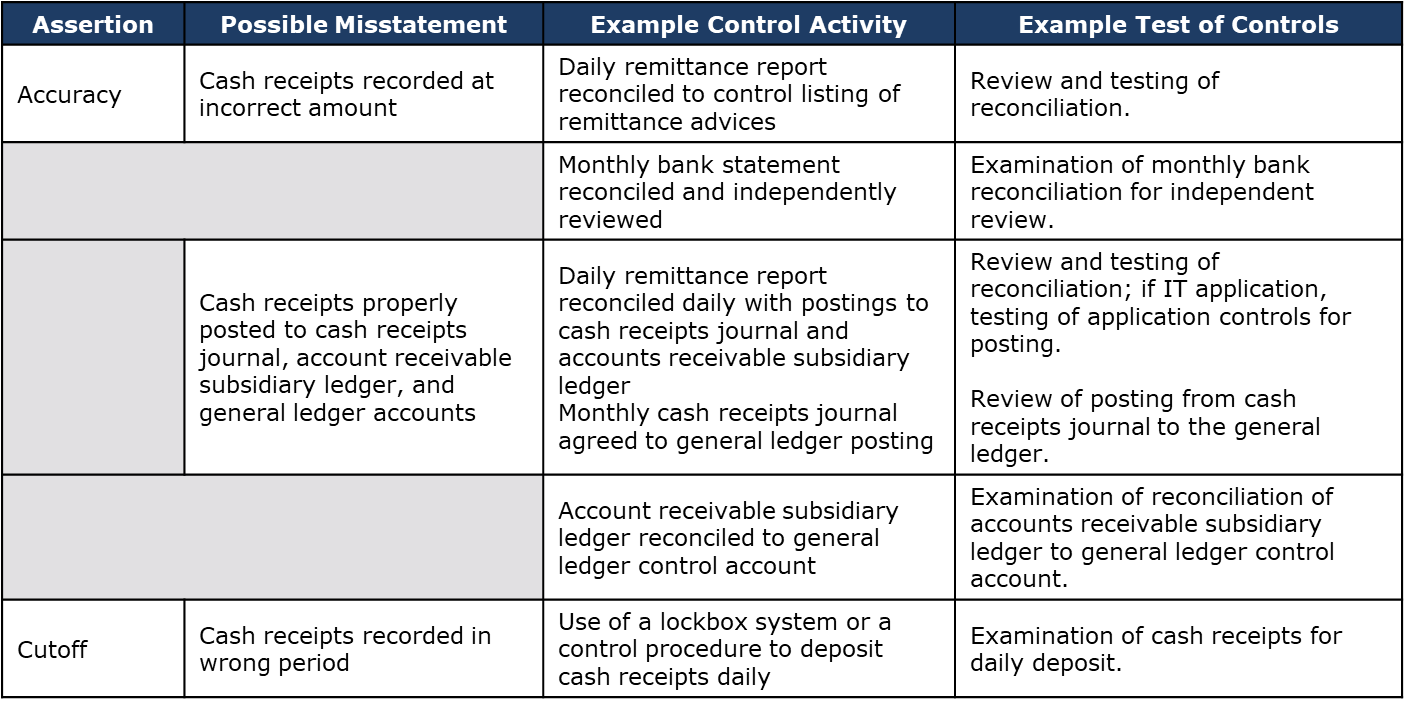

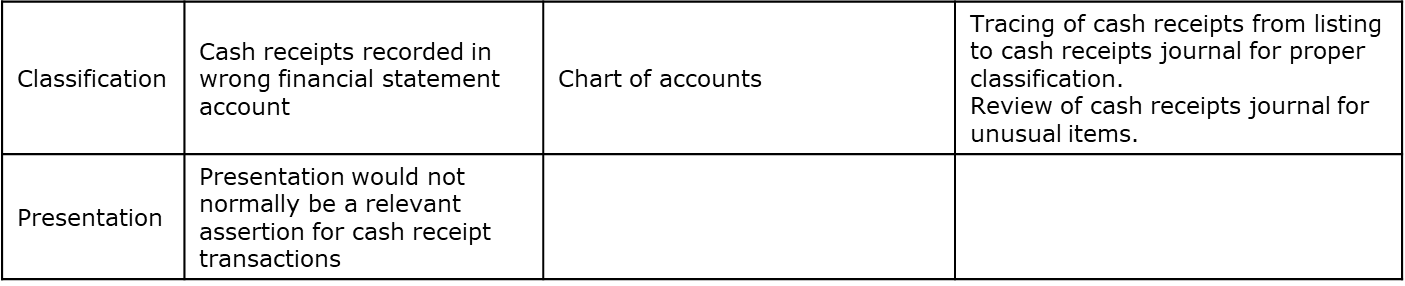

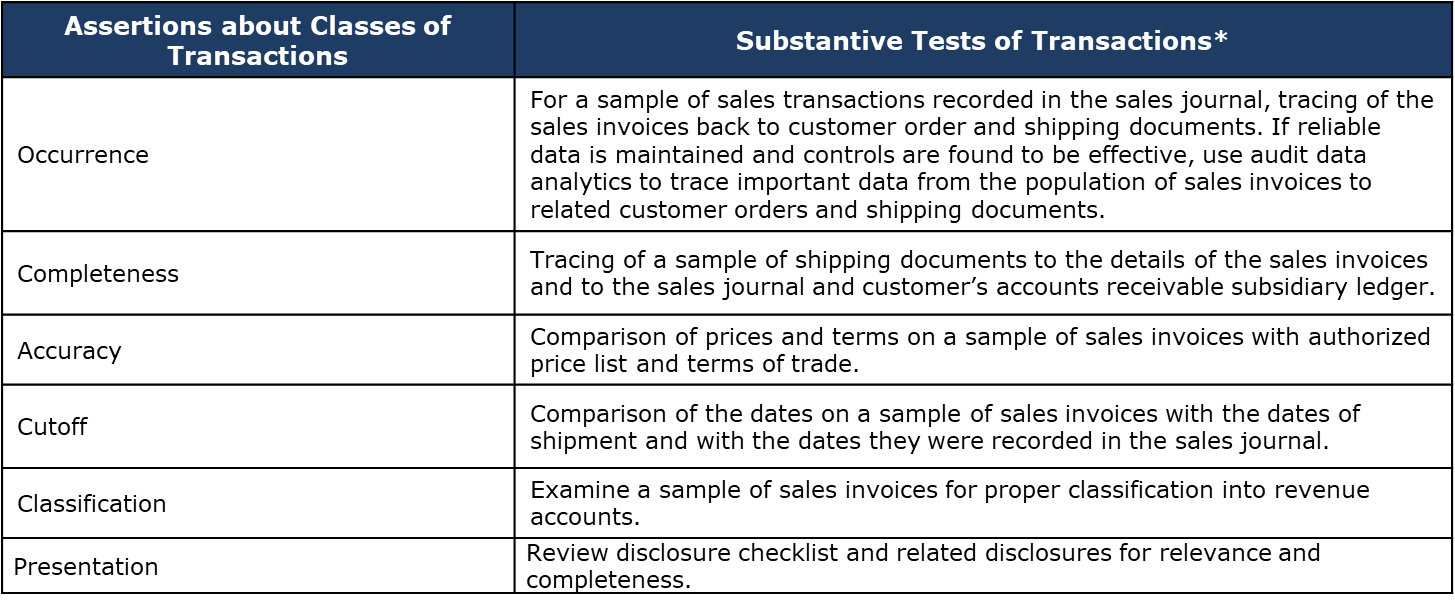

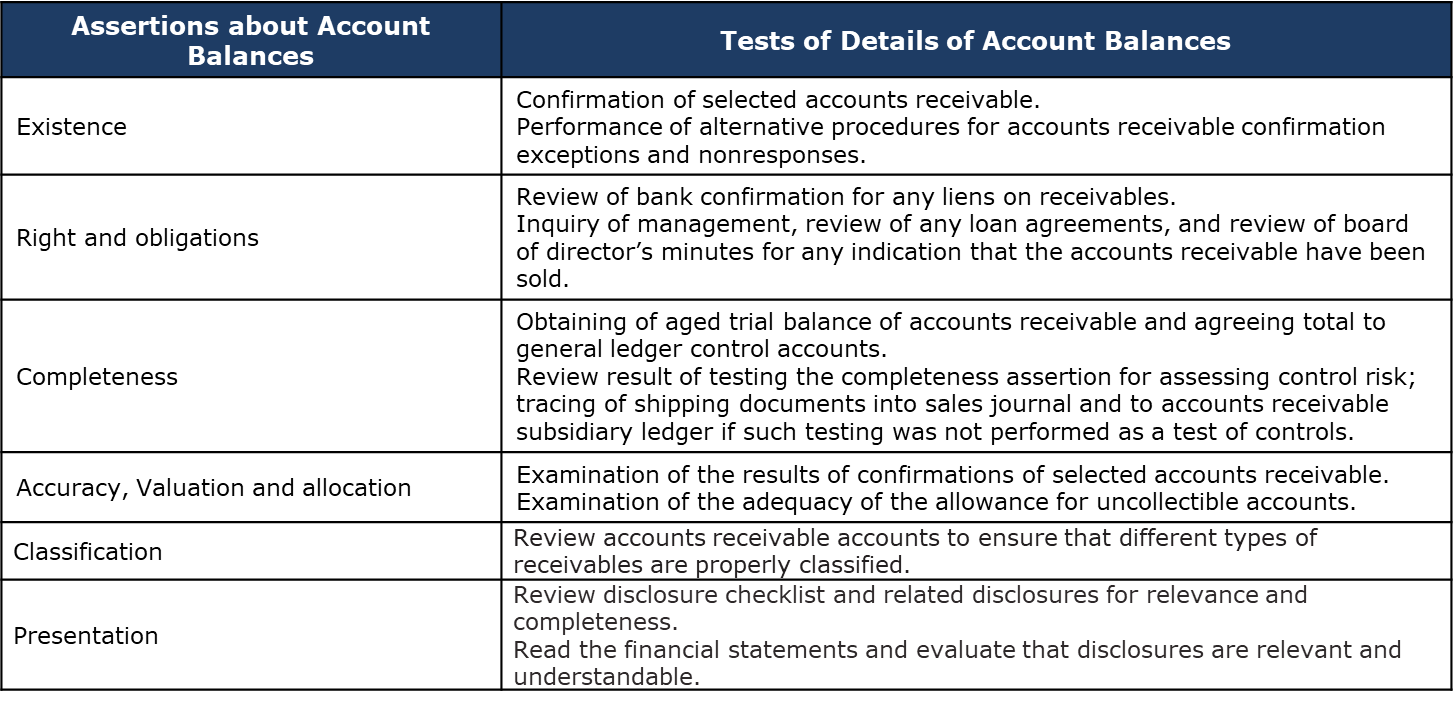

Table 6.4 – assertions about classes of transactions and events and related control procedures

Assertion | Control Activities |

Occurrence |

|

Completeness |

|

Authorization |

|

Accuracy |

|

Cutoff |

|

Classification |

|

Presentation |

|

October 23, 2023

Obtain and Understanding of Internal Control

- The auditor should obtain an understanding of each of the components of internal control to plan the audit:

- (1) Understand the control environment

- (2) Understand the entity’s risk assessment process

- (3) Understand the info system and communications

- (4) Understand control activities

- (5) Understand monitoring of controls

- This knowledge is used to …

- (1) Identify types of potential misstatement

- (2) Pinpoint the factors that affect the RMM

- (3) Design tests of controls and substantive procedures

- In deciding on the nature and extent of the understanding of internal control needed for the audit, the auditor should consider the complexity and sophistication of the entity’s operations and systems, including the extent to which the entity relies on annual controls or on automated controls

- The auditor may determine that the engagement team needs an IT specialist:

- (1) Evaluate the nature and complexity of the entity’s IT systems

- (2) Determine whether the engagement team needs an IT specialist

- In determining whether an IT specialist is needed, the following factors should be considered:

- (1) The complexity of the entity’s IT systems and controls and the manner in which they are used in conducting the entity’s business

- (2) The significance of changes made to existing systems, or the implementation of new systems

- (3) The extent to which data are shared among systems

- (4) The extent of the entity’s participation in e-commerce

- (5) The entity’s use of emerging technologies

- (6) The significance of audit evidence that is available only in electronic form

Understanding the Control Environment

Exhibit 6.1 – example info & documentation excerpt

Control Environment Questionnaire | ||

Entity: EarthWear Clothiers Completed by: SAA Date: 9/30/25 | Balance Sheet Date: 12/31/2025 Reviewed by: DRM Date: 10/15/25 | |

COMMUNICATION AND ENFORCEMENT OF INTEGRITY AND ETHICAL VALUES The effectiveness of controls cannot rise above the integrity and ethical values of the people who create, administer, and monitor them. Integrity and ethical values are essential elements of the control environment, affecting the design, administration, and monitoring of other components. Integrity and ethical behaviour are the product of the entity’s ethical and behavioral standards, how they are communicated, and how they are reinforced in practice. | ||

Yes, No, or N/A | Comments | |

Have appropriate entity policies regarding matters such as acceptable business practices, conflicts of interest, and codes of conduct been established, and are they adequately communicated? | Yes | The permanent work papers contain a copy of EarthWear’s conflict-of-interest policy. |

Does management demonstrate the appropriate “tone at the top,” including explicit moral guidance about what is right or wrong? | Yes | EarthWear’s management maintains high moral and ethical standards and expects employees to act accordingly. |

Are everyday dealings with customers, suppliers, employees, and other parties based on honesty and fairness? | Yes | EarthWear’s management maintains a high degree of integrity in dealing with customers, suppliers, employees, and other parties; it requires employees and agents to act accordingly. |

Does management determine to an adequate extent the knowledge and skills needed to perform particular jobs? | Yes | The job descriptions specify the knowledge and skills needed. The Human Resources Department uses this information in hiring, training, and promotion decisions. |

Does evidence exist that employees have the requisite knowledge and skills to perform their job? | Yes | Our prior experiences with EarthWear personnel indicate that they have the necessary knowledge and skills. |

Documenting and Understanding of Internal Control

- Procedure manuals and organizational charts

- Documents the entity’s policies and procedures

- Includes documentation of the accounting system and related control activities

- Organizational chart presents the designated lines of authority and responsibility

- These can assist the auditor document their understanding of the internal control system

- Internal control questionnaires

- Provide a systematic means for the auditor to investigate various areas

- Generally used for entities with a complex internal control structure

- Contains questions about the important factors or characteristics of the 5 internal control components

- Flowcharts

- Provide a diagrammatic representation of the entity’s accounting system

- Outlines the configuration of the system in terms of functions, documents, processes, and reports

- Documentation facilities an auditor’s analysis of the system’s strengths and weaknesses

- Used to document the auditor’s understanding of an entity’s internal control over financial reporting

- Narrative description

- Understanding of internal controls may be documented in a memo

- This approach is the most appropriate when the entity has a simple internal control system

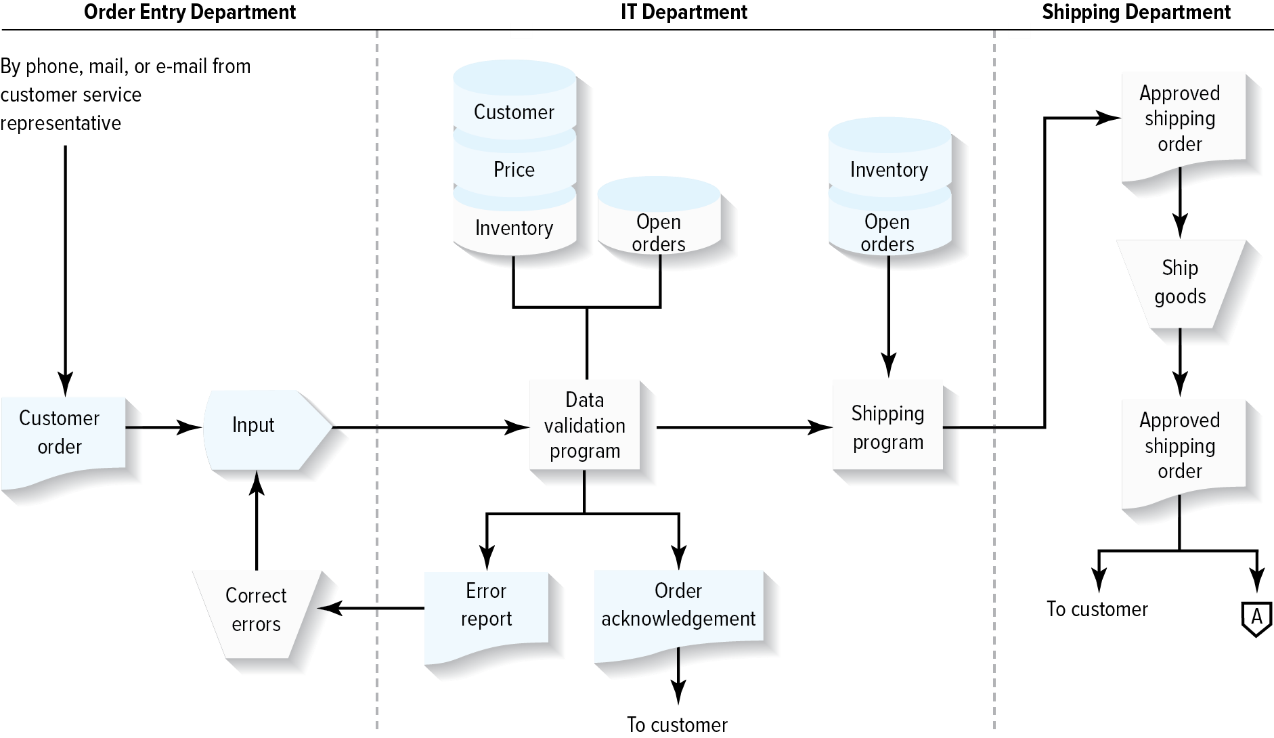

Figure 6.3 – an example of a flowchart for the order entry portion of the revenue process

The Effect of Entity Size on Internal Control

- The size of an entity may affect how the various components of internal control are implemented

- While the basic concepts of the five components should be present in all entities, they are likely to be less formal in a small or midsize entity than in a large entity

The Limitation of an Entity’s Internal Control

- An internal control system should be designed and operated to provide reasonable assurance that an entity’s objectives are being achieved

- The concept of reasonable assurance recognizes that the cost of an entity’s internal control system should not exceed the benefits that are expected to be derived

- Limitations:

- (1) Management override of internal control

- (2) Human errors or mistakes

- (3) Collusion

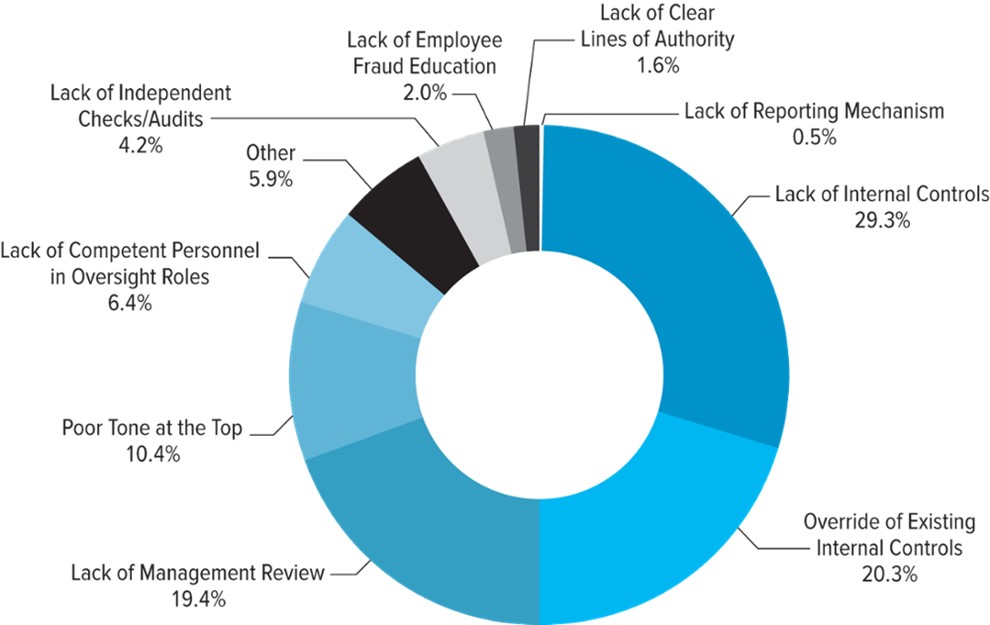

Figure 6.4 – primary internal control weakness observed by CFE

Assessing Control Risk

- Assessing control risk is the process of evaluating the effectiveness of an entity’s internal control in preventing, or detecting and correcting, material misstatements in the F/S

- Auditor can set CR at high (substantive strategy) or at a low level (reliance strategy)

- To set CR below high (moderate or low), the auditor must …

- (1) Identify specific controls that will be relied upon

- (2) Perform tests of controls

- (3) Conclude on the achieved level of control risk

Identify Specific Controls That Will Be Relied Upon

- The auditor’s understanding of internal control is used to identify the controls that are likely to prevent, or detect and correct, material misstatement in specific assertions

- We don’t necessarily need to rely on every single control

- We need to understand them all

- Prepare a narrative or a flowchart that documents these control procedures

Perform Tests of Controls

- Tests of controls are performed in order to provide evidence to support the lower level of CR when using a reliance strategy

- Directed toward the effectiveness of the design of a control concerned with evaluating whether that control is suitably designed to prevent, or detect and correct, material misstatements

- Directed toward operating effectiveness are concerned with assessing how the control was applied, the consistency with which it was applied during the audit period, and by whom it was applied

- Types of tests of controls:

- Inquiry of appropriate entity personnel

- Inspection of documents indicating the performance of the control

- Observation of the application of the control

- Reperformance of the application of the control by the auditor

- What controls will we rely on to help us assess whether the account balances or class of transactions are not materiality misstated?

Conclude on the Achieved Level of Control Risk

- The auditor uses the combination of the achieved level of CR and the assessed level of IR to determine the level of DR that is needed in order to bring audit risk to an acceptable low level

- When we are doing our planning, we need to do a planned level of control risk based on the organization

- We will only do this when we decided to use a reliance strategy (aka., combined approach)

Documenting the Achieved Level of Control Risk

- The auditor’s assessment of CR and the basis for the achieved level can be documented using a structured working paper, an internal control questionnaire, or a memorandum

Table 6.5 – an example of assessing control risks and its effects

- There is not one pattern/test description that fits all

Which of the following audit techniques would most likely provide an auditor with the least assurance about the effectiveness of the operation of a control? |

- Inquiry of entity personnel

- Reperformance of the control by the auditor

- Observation of entity personnel

- Walkthrough

Substantive Procedures

- Last step in the decision process under either strategy

- Auditing standards require some substantive testing for all significant account balances or classes of transactions

Table 6.6 – performing substantive procedures

Low-Detection-Risk Strategy 🡪 Entity 1 | |

Nature | Aduit tests for all significant audit assertions using the following types of audit procedures:

|

Timing | All significant work completed at YE |

Extent | Extensive testing of significant accounts or transactions |

High-Detection-Risk Strategy 🡪 Entity 2 | |

Nature | Corroborative audit tests using the following types of audit tests:

|

Timing | Interim and YE |

Extent | Limited testing of accounts or transactions |

- Note: if an inventory count is taking place, the auditor must attend

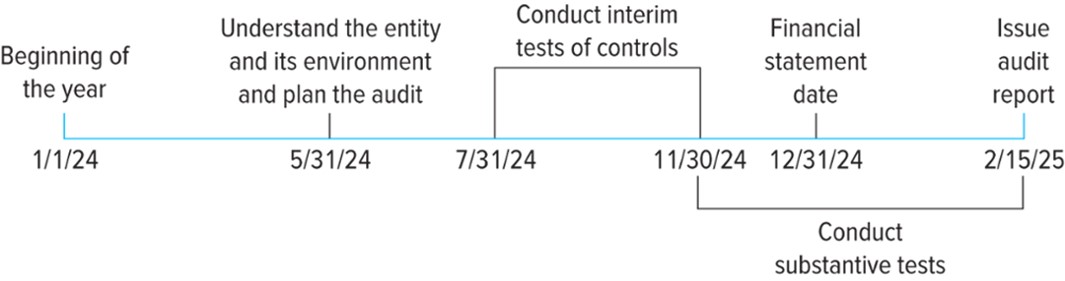

Timing of Audit Procedures

- Interim

- Year end

Figure 6.5 – timeline for planning and performing the audit of EarthWear Clothiers

Interim Audit Procedures

- Interim tests of controls:

- Assertion being tested not significant

- Control has been effective in prior audits

- Efficient use of staff time

- Interim substantive procedures:

- Control environment

- Availability of info later

- The purpose of the substantive procedure

- The assessed risk of material misstatement

- The nature of the transactions or balances and relevant assertions

- The ability of the auditor to perform appropriate procedures to cover the remaining period

Auditing Accounting Applications Processed by Service Organizations

- In some instances, an entity may have some or all its accounting transactions processed by an outside service organization

- Because the entity’s transactions are subjected to the controls of the service organization, one of the auditor’s concerns is the internal control system in place at the service organization

- It is not uncommon for service organizations to have an auditor issue one of two types of reports on their operations

- The type 1 report describes the service organization’s controls and assesses whether they are suitably designed to achieve specified internal control objectives

- The type 2 report goes further by providing assurance on the operating effectiveness of the service organization’s controls based on the auditor’s tests of controls

- An auditor may reduce control risk below high only based on a service auditor’s Type 2 report

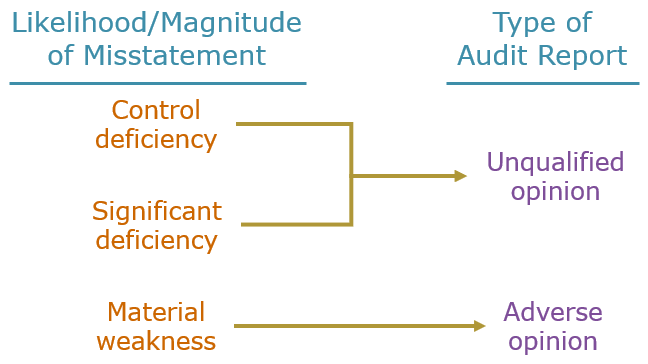

Communication of Internal Control-Related Maters

- Control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned function, to prevent, or detect and correct, misstatements on a timely basis

- Significant deficiency is a deficiency, or a combination of deficiencies, in internal control that is less severe than a material weakness but is important enough to merit attention by those charged with governance

- Material weakness is a deficiency, or combination of deficiencies, in internal control, such that there is a reasonable possibility that a material misstatement of the entity’s financial statements will not be prevented, or detected and corrected, on a timely basis

Table 6.7 – examples of reportable conditions

Deficiencies in the Design of Controls

Failures in the Operation of Internal Control

|

Types of Controls in an IT Environment

- General controls:

- Data center and network operations

- System software acquisition, change, and maintenance

- Access security

- Application system acquisition, development, and maintenance

- Application controls:

- Data capture controls

- Data validation controls

- Processing controls

- Output controls

- Error controls

Table 6.8 – common data validation controls

Data Validation Control | Description |

Limit test | A test to ensure that a numerical value does not exceed some predetermined value |

Range test | A check to ensure that the value in a field falls within an allowable range of values |

Sequence check | A check to determine if input data are in proper numerical or alphabetical sequence |

Existence (validity) test | A test of an ID number or code by comparison to a file or table containing valid ID numbers or codes |

Field test | A check on a field to ensure that it contains either all numeric or all alphabetic characters |

Sign test | A check to ensure that the data in a field have the proper arithmetic sign |

Check-digit verification | A numerical value computed to provide assurance that the original value was not altered |

Closed-loop verification | A process that takes data entered into the system to find and present other, related info, enabling the user to verify the correctness of the original data entry |

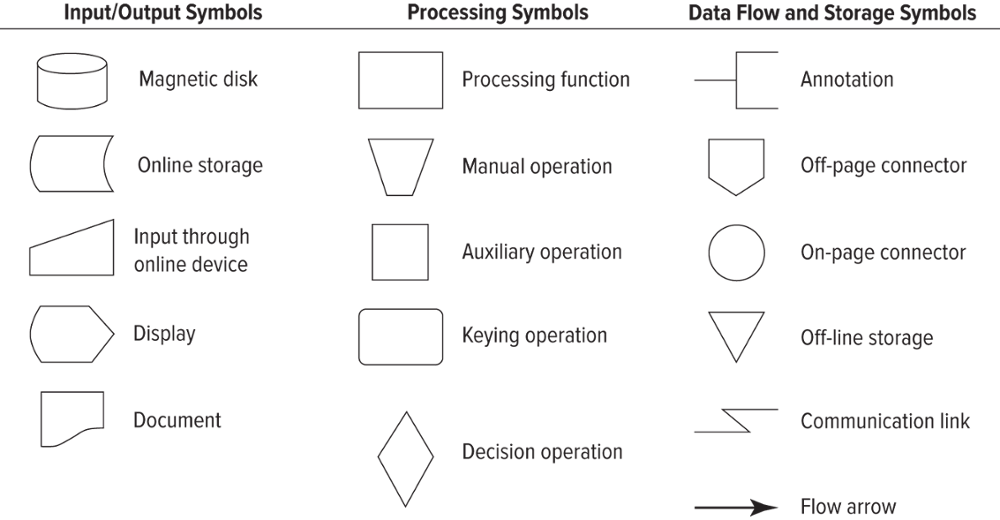

Figure 6.6 – flowcharting symbols

Auditing Internal Control Over Financial Reporting

October 27, 2023

Check Nexus for 7 generally accepted internal control document

Management Responsibilities

Canada

- The national instruments 52-109 requires management’s of publicly traded companies to issue a report that certifies the effectiveness of their internal controls

- This certification is not yet required to be audited

- Management can choose to have it audited under Other Canadian Standard Section 5952

United States

- Management are required to comply with the following requirements for the external auditor to complete an audit of ICFR:

- (1) Accept responsibility for the effectiveness of the entity’s ICFR

- (2) Evaluate the effectiveness of the entity’s ICFR using suitable control criteria

- (3) Support the evaluation with sufficient evidence, including documentation

- (4) Present a written assessment regarding the effectiveness of the entity’s ICFR as of the end of the entity’s most recent fiscal year

Internal Control over Financial Reporting (ICFR) Defined

- ICFR is defined as a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of FS in accordance with GAAP

- Controls include procedures that:

- (1) Pertain to the maintenance of records that accurately and fairly reflect the transactions and dispositions of the assets of the company

- (2) Provide reasonable assurance that transactions are properly authorized and recorded in accordance with GAAP

- (3) Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s asset that could have a material effect on the FS

- Points (1) and (2) relate directly to controls for initiating, authorizing, recording, processing, and reporting significant accounts and disclosures and related assertions embodied in the FS

- These significant accounts are the ones that are likely to give us a material misstatement

- Point (3) is concerned with controls over safeguarding of assets that are moveable or can potentially be stolen (ex: inventory or cash on hand)

Internal Control Deficiencies Defined

Control Deficiency

- A control deficiency exists when the design or operation of a control does not allow management or employees, in the normal course of performing their assigned functions, to prevent or detect misstatements on a timely basis

- A design deficiency exists when:

- (1) A control necessary to meet the relevant control objective is missing

- Has it been designed correctly?

- Is it intended to do what it has to do?

- There is no control in place to ensure that the 2nd signature is properly authorized

- (2) An existing control is not properly designed so that, even if the controls operates as designed, the control objective would not be met

- (1) A control necessary to meet the relevant control objective is missing

- A deficiency in operation exists when:

- (1) A properly designed control does not operate as designed

- (2) When the person performing the control does not possess the necessary authority or qualifications to perform the control effectively

Significant Deficiency

- A significant deficiency is a control deficiency, or a combination of control deficiencies, in ICFR that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of the company's financial reporting

- If we find these in controls, we want to be able to report that to the audit committee

- A control deficiency may be serious enough that it is to be considered not only a significant deficiency but also a material weakness in the system of internal control

Material Weakness

- A material weakness is a deficiency, or a combination of deficiencies, in ICFR, such that there is a reasonable possibility that a material misstatement of the annual or interim FS will not be prevented or detected on a timely basis

- This is a bigger issue

- If we find this, we have to report that info ASAP to the audit committee and we can no longer rely on that control to work 🡪 increase substantive testing

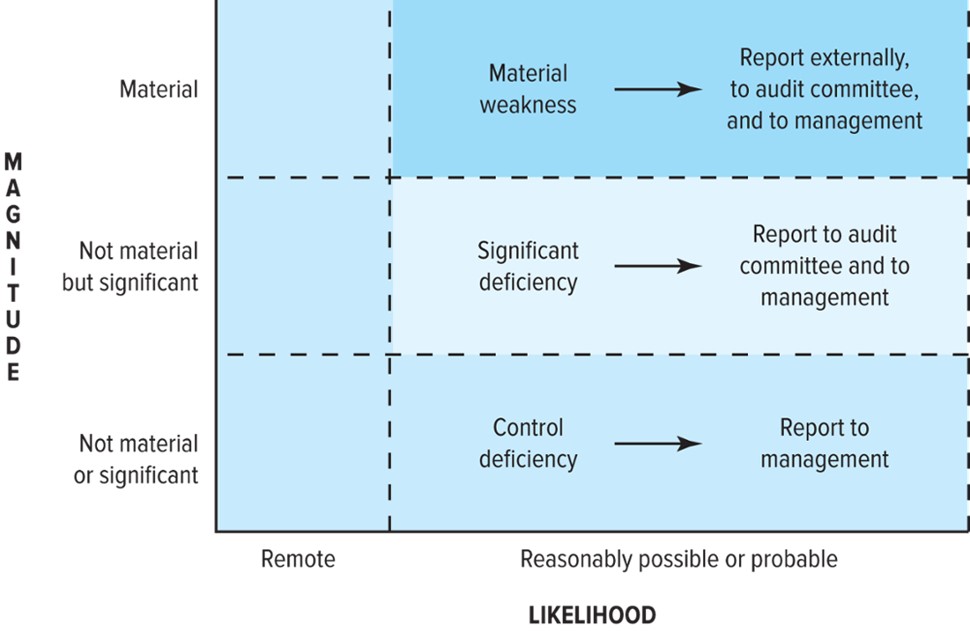

Likelihood and Magnitude

- The auditor must consider two dimensions of the control deficiency:

- (1) Likelihood means reasonably possible (50% or more)

- (2) Magnitude means material, significant, or insignificant

- If likelihood is assessed as “remote”, an identified control issue does not rise to the level of control deficiency

- If likelihood is assessed as more than remote, the control issue will be considered a deficiency, a significant deficiency, or a material weakness depending on the magnitude of the deficiency

| Figure 7.1 – the relationship of likelihood and magnitude in determining the materiality of a control deficiency |

A control deviation caused by an employee performing a control procedure that he or she is not authorized to perform is always considered a … |

- Deficiency in design

- We can argue that this is right

- According to the definition, the control is missing to prevent or detect the misstatement and/or it doesn’t matter if the control is there, it will not work

- Deficiency in operation

- Significant deficiency

- It is not this because we can’t determine the magnitude of material weakness

- Material weakness

Management’s Assessment Process

- Steps in the evaluation process:

- (1) Identify financial reporting risks and related controls

- (2) Consider which locations to include in the evaluation

- (3) Evaluate evidence about the operating effectiveness of ICFR

- Most entities use the framework developed by COSO

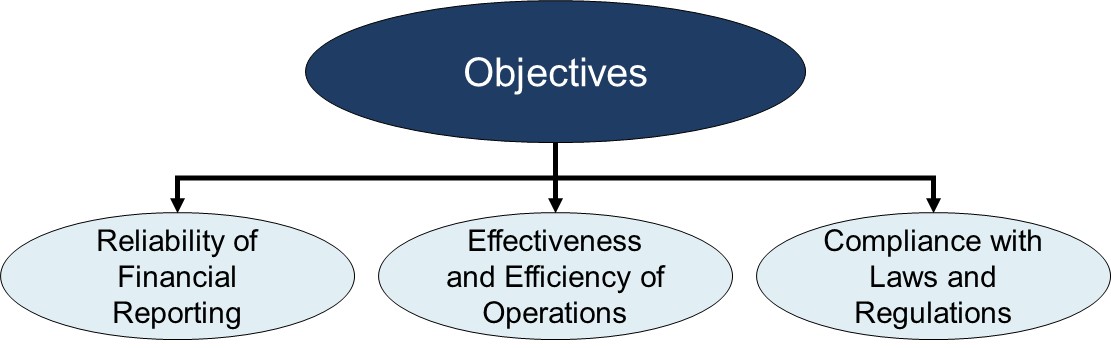

- This framework identifies primary objectives of internal control:

- (1) Reliable financial reporting

- (2) Efficiency and effectiveness of operations

- (3) Compliance with laws and regulations

Identify Financial Reporting Risks and Related Controls

Table 7.1 – examples of entity-level controls

|

Management’s Documentation

- Documentation should include the design of the controls management has placed in operation to adequately address identified financial reporting risks, including the entity-level controls and other pervasive elements necessary for effective ICFR

- Management is not required to identify and document every control in the process or to document the business process impacting ICFR

- Management must develop sufficient documentation to support its assessment of the effectiveness of internal control

- This documentation may take many forms (ex: paper, electronic files, or other media)

- It also includes policy manuals, process models, flowcharts, job descriptions, documents, and forms

Performing an Audit of ICFR

Integrating the Audits of Internal Control and Financial Statements

- An integrated audit is composed of the audits of internal control and the FS

- The control testing impacts the planned substantive procedures

- Also, the results of the substantive procedures are considered in the evaluation of internal control

- The tests and the discussions related to control testing in this chapter are relevant even if we are not doing an entire audit on the internal controls

- We still evaluate the effectiveness of internal controls & decide whether we are relying on them

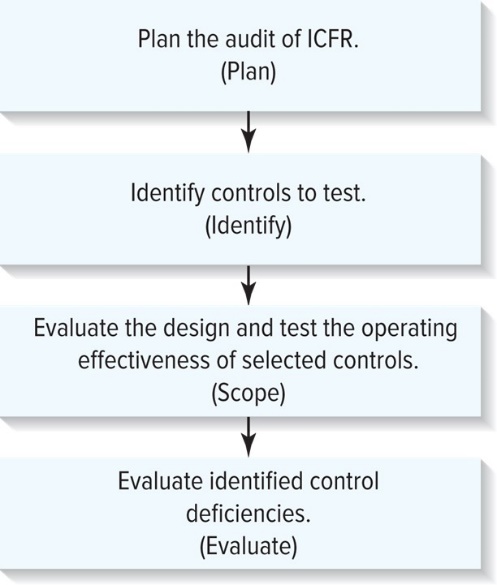

| Figure 7.2 – steps in performing an audit of ICFR

|

Planning the Audit of ICFR

- The planning process is like the process used for the audit of FS

- Consider the following:

- Role of risk assessment and the risk of fraud

- Scaling the audit

- Using the work of others

Table 7.3 – factors that may affect planning an audit of ICFR

|

Using the Work of Others

- A major consideration for the external auditor is how much work is to be performed by others

- In determining the extent to which the auditor may use the work of others, the auditor should:

- (1) Evaluate the nature of the controls subjected to the work of others

- (2) Evaluate the competence and objectivity of the individuals who performed the work

- (3) Test some of the work performed by others to evaluate the quality and effectiveness of their work

- As the risk associated with control being tested increases, the external auditor should do more of the work

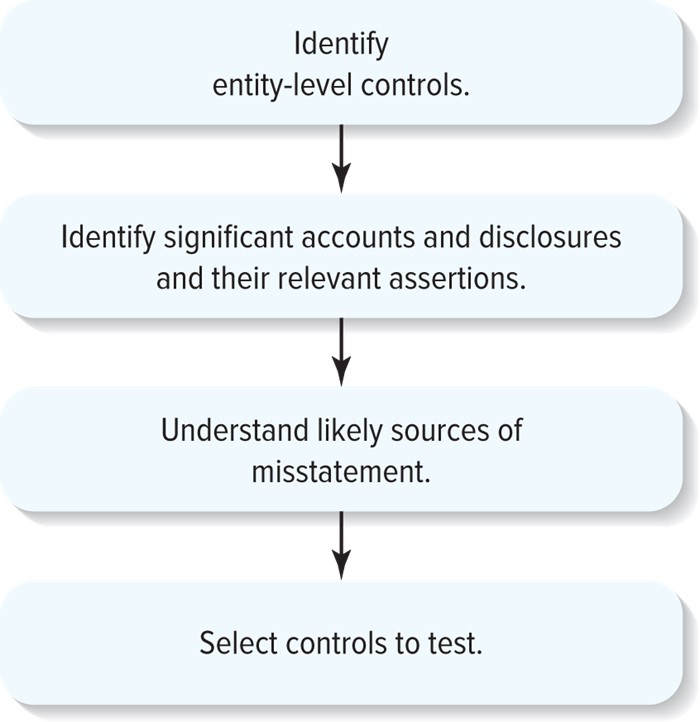

Identify Controls to Test

| Figure 7.3 – identifying the controls to test

|

Identifying Significant Accounts

- To identify significant accounts and disclosures and their relevant assertions, the auditor assesses the following risk factors:

- Size and composition of the account

- Susceptibility to misstatement due to errors or fraud

- Volume of activity, complexity, and homogeneity of the individual transactions processed through the account or reflected in the disclosure

- Nature of the account or disclosure

- Accounting and reporting complexities associated with the account or disclosure

- Exposure to losses in the account

- Possibility of significant contingent liabilities arising from the activities reflected in the account or disclosure

- Existence of related party transactions in the account

- Changes from the prior period in account or disclosure characteristics

Sources of Misstatements

- To understand the likely sources of potential misstatements, the auditor needs to do the following:

- Understand the flow of transactions related to the relevant assertions

- Identify the points within the entity’s processes at which a misstatement could arise that would be material

- Identify the controls that management has implemented to address these potential misstatements

- Identify the controls that management has implemented over the prevention or timely detection of unauthorized acquisition, use, or disposition of the company’s assets that could result in a material misstatement of the FS

- Performing walkthroughs is the best way to identify potential sources of misstatements

- Preforming a walkthrough involves auditors tracing a transaction from origination through the entity’s process and info system until it is reflected in the entity’s financial reports

Select Controls to Test

- Auditor does not need to test all controls – only the ones that are important to the auditor’s conclusion about whether the entity’s controls sufficiently address the assessed risk of misstatement to each relevant assertion 🡪 key controls

- This is a subjective task and therefore requires professional judgement

- The auditor should evaluate whether to test preventive controls, detective controls, or a combination of both

Table 7.4 – select controls to test

Factors to consider when identifying controls to test:

|

Evaluate, Design, and Test Operating Effectiveness of Controls

- Evaluate design effectiveness of controls

- Controls are effectively designed when they prevent or detect errors or fraud that could result in material misstatements in the FS

- Evaluate key controls through inquiry, observation, walkthrough, inspection of relevant documentation and subjective evaluation

- Test and evaluate operating effectiveness

- An auditor evaluates the operating effectiveness of a control by determining whether the control is operating as designed and whether the person performing the control possesses the necessary authority and competence to perform the control effectively

- (1) Nature: inquiry, inspection of documents, observation, and reperformance

- (2) Timing: interim vs. “as of” date

- This is when we decide when to do these tests

- Testing at interim gives management time to correct any deficiencies they do find

- (3) Extent:

- (a) Nature of the control

- Manual or automated

- We want to be able to test manual controls more – easier to manipulate & find human error

- (b) Frequency of operation

- The more frequent a manual control operates, the greater the number of operations of control that the auditor should test

- (c) Importance of the control

- The more important the control = the more extensively it should be tested

- (a) Nature of the control

Suppose an entity implements a control whereby its sales manager reviews and investigates a report listing sales invoices with unusually high or low gross margins. Would inquiry of the sales manager as to whether he or she investigates discrepancies be sufficient evidence to ensure that the control is working effectively? |

- No

- The auditor should corroborate the sales manager’s responses by performing other procedures, such as inspecting reports generated by the performance of the control and evaluating whether appropriate actions were taken

Evaluate Identified Control Deficiencies

- As discussed previously, the auditor must consider the likelihood and magnitude of the control deficiency à see table 7.6

- Factors that affect whether the magnitude of the misstatement may result in a material weakness include …

- (1) The FS amounts or total of transactions exposed to the deficiency

- (2) The volume of activity in the account balance or class of transactions exposed to t he deficiency that has occurred in the current period or that is expected in future periods

- If a deficiency, or combination of deficiencies, prevents the auditor from having reasonable assurance that transactions are recorded properly, then the auditor should treat the deficiency as an indicator of a material weakness à see table 7.7

Note: these tables are useful when identifying the likelihood

Table 7.6 – risk factors that affect the likelihood that a control deficiency will result in a misstatement of an account balance or disclosure

|

Table 7.7 – indicators of material weaknesses

|

October 30, 2023

Remediation of a Material Weakness

- Remediation is the process of correcting a material weakness in the ICFR

- If a material weakness is corrected before the “as of” date, there must be sufficient time for both management and the auditor to test the operating effectiveness of the control – if not, an adverse opinion is still issued

Auditor Documentation Requirements

- The auditor should document the processes, procedures, judgments, and results relating to the audit of internal control consistent with audit quality documentation standards

- Documentation must include …

- (1) Auditor’s understanding and evaluation of the design of each of the components of the entity’s ICFR

- (2) Documentation of the process used to determine the points at which misstatements could occur within significant accounts and disclosures

- (3) Extent to which they relied on work performed by others

- (4) Scope of the testing

Special Considerations When Auditing Internal Control

Use of Service Organizations

- Many companies use a service organization to process transactions

- If the service organization’s services make up part of a company’s information system, then it is considered part of the information and communication component of the company’s internal control over financial reporting

- Thus, both management and the auditor must consider the activities of the service organization

- Management and the auditor should perform the following procedures with respect to the activities performed by the service organization:

- (1) Obtain an understanding of the nature and significance of the services provided by the service organization and their effect of the user entity’s internal control relevant to the audit, sufficient to identify and assess the risks of material misstatement

- (2) Design and perform audit procedures responsive to those risks

Safeguarding of Assets

- Safeguarding of assets are policies and procedures that “provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the entity’s assets that could have a material effect on the financial statements”

Computer-Assisted Audit Techniques

- Computer-assisted audit techniques (CAATs) include:

- Generalized audit software

- Custom audit software

- Test data

Table 7.9 – generalized audit software

Functions | Description |

File or database access | Reads and extracts data from an entity's computer files or databases for further audit testing |

Selection operators | Select from files or databases transactions that meet certain criteria |

Arithmetic functions | Perform a variety of arithmetic calculations (addition, subtraction, and so on) on transactions, files, and databases |

Statistical analyses | Provide functions supporting various types of audit sampling |

Report generation | Prepares various types of documents and reports |

Custom Audit Software

- Custom audit software is generally written by auditors for specific audit tasks and it may be required when the entity’s computer system is not compatible with the auditor’s generalized audit software

- Custom software:

- Is expensive to develop

- May require long development time

- May required extensive modification if the entity changes its accounting application programs

Test Data

- Test data are developed by the auditor to test the application controls in the entity’s computer programs

- The technique can be used to check:

- Data validation controls and error detection routines

- Processing logic controls

- Arithmetic calculations

- The inclusion of transactions in the records, files, and reports

Management Responsibilities Under Section 404

- Section 404 of the Sarbanes-Oxley Act requires managements of publicly traded companies to issue a report that accepts responsibility for establishing and maintaining “adequate” internal control over financial reporting (ICFR) and assert whether ICFR is effective as of the end of the fiscal year

- Management must comply with the following requirements for the external auditor to complete an audit of ICFR:

- (1) Accept responsibility for the effectiveness of the entity’s ICFR

- (2) Evaluate the effectiveness of the entity’s ICFR using suitable control criteria

- (3) Support the evaluation with sufficient evidence, including documentation

- (4) Present a written assessment regarding the effectiveness of the entity’s ICFR as of the end of the entity’s most recent fiscal year

Auditor Responsibilities Under Section 404 and AS5

- The entity’s independent auditor must audit and report on the effectiveness of ICFR

- The auditor is required to conduct an integrated audit of the entity’s ICFR and its F/S

Written Representations

- In addition to the management representations obtained as part of a F/S audit, the auditor also obtains written representations from management related to the audit of ICFR

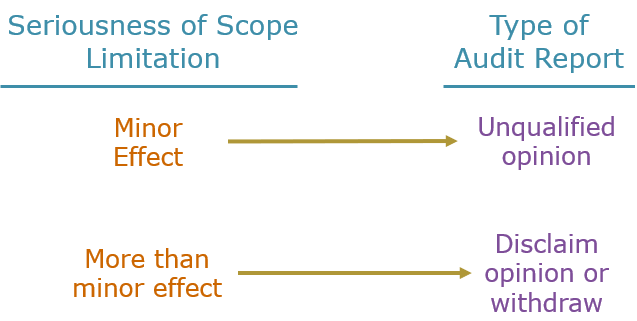

- Failure to obtain written representations from management, including management’s refusal to furnish them, constitutes a limitation on the scope of the audit sufficient to preclude an unqualified opinion

Auditor Reporting on ICFR

Types of Reports

| Figure 7.5a – report modification based on control deficiencies

|

| Figure 7.5b – report modification based on scope limitation |

Other Reporting Issues

- Management’s report is incomplete or improperly presented

- The auditor decides to refer to the report of other auditors

- A significant subsequent event has occurred

- There is additional information contained in management’s report on internal control

- There is a remediated material weakness at an interim date

Additional Required Communications in an Audit of ICFR

- Significant deficiencies and material weaknesses:

- The auditor must communicate in writing to management and the audit committee all significant deficiencies and material weaknesses identified during the audit (AS5)

- This communication should be made prior to the issuance of the auditor’s report on ICFR

- Control deficiencies:

- In addition, the auditor should communicate to management, in writing, all control deficiencies identified during the audit

- As well as inform the audit committee when such a communication has been made

Audit Sampling: An Overview and Application to Tests of Controls

November 01, 2023

Introduction

- Given the size and complexity of most entities needing a FS audit, it is usually not economical to examine all of the accounting records and supporting documents

- Auditors often find it necessary to draw conclusions about the fairness of FS assertions based on examinations of samples of the records and transactions

- As a result, the auditor provides reasonable, not absolute, assurance that the FS are fairly presented

- Accepting uncertainty is the trade-off between the cost of examining all the data and the cost of making an incorrect decision based on a sample of the data

- Auditing standards recognize and permit both statistical and nonstatistical methods of audit sampling

- With nonstatistical sampling, the auditor does not strictly apply statistical techniques and can apply some judgement to evaluate the results

- The steps and techniques used for these two sampling approaches are similar than they are different

- Technological advances have reduced the number of times auditors need to apply sampling techniques to gather audit evidence:

- (1) Development of well-controlled, automated accounting systems

- (2) Powerful audit software to download and examine entire population of data

- Technology will never eliminate the need for auditors to rely on sampling to some degree because:

- (1) Many control processes require human involvement

- (2) Many testing procedures require the auditor to physically inspect an asset or inspect characteristics of a transaction or balance

- (3) In many cases, auditors are required to obtain and evaluate evidence from third parties

- (4) Audit data analytics are only as good as the quality of the underlying data and often the completeness, accuracy, and validity of the underlying data need to be tested and sampling can be an effective and efficient technique

- (5) Audit data analytics often identify many potential exceptions that the auditor may test using sampling

Definitions and Key Concepts

Audit Sampling

- Audit sampling is the selection and evaluation of less than 100 percent of the items in a population of audit relevance selected in such a way that the auditor expects the sample to be representative of the population and thus likely to provide a reasonable basis for conclusions about the population

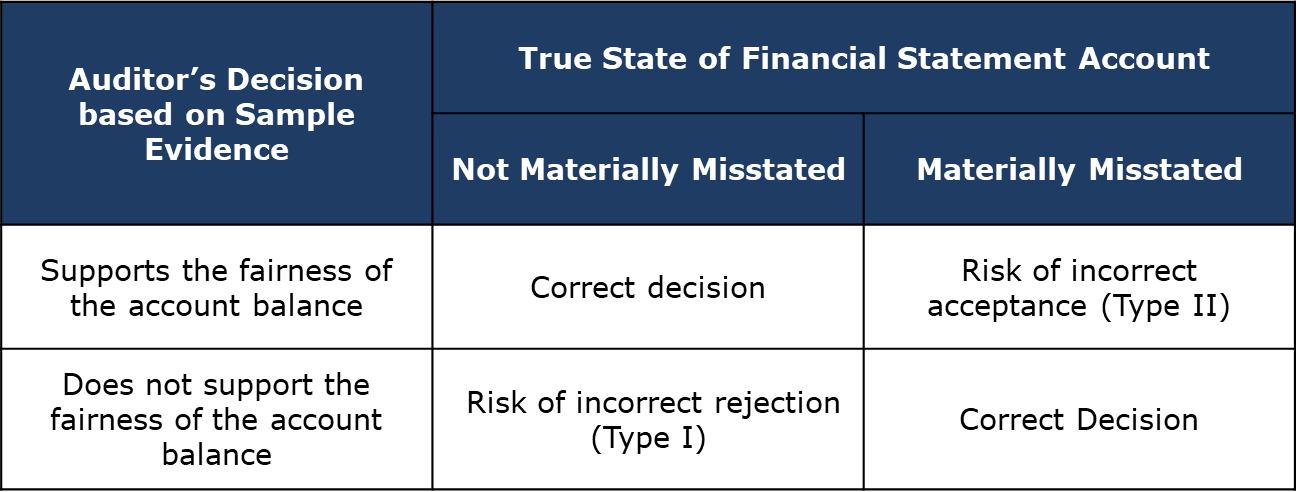

Sampling Risk

- Sampling risk is the possibility that the sample drawn is not representative of the population and that, as a result, the auditor will reach an incorrect conclusion about the account balance or class of transactions based on the sample

- A representative sample is one where the evaluation of the sample results lead to the same conclusions that would be drawn if the same audit procedures were applied to the entire population

- When using audit sampling to obtain evidence, the auditor must always accept some sampling risk because they are not examining all items in a population

- Types of sampling risk:

- (1) Type I - risk of incorrect rejection

- In a test of internal controls, if the risk that the sample supports a conclusion that the control is not operating effectively when, in fact, it is operating effectively

- In substantive testing, it is the risk that the sample indicates that the recorded balance is materially misstated when, in fact, it is not

- This relates to the efficiency of the audit

- This type of decision error can result in the auditor conducting more audit work than necessary to reach the correct conclusion

- (2) Type II - risk of incorrect acceptance

- In a test of internal controls, it is the risk that the sample supports a conclusion that the control is operating effectively when, in fact, it is not operating effectively

- In substantive testing, it is the risk that a sample supports the recorded balance when it is, in fact materially misstated

- This relates to effectiveness of the audit

- This type of decision error can result in the auditor failing to detect a material misstatement in the FS, which can lead to litigation against the auditor by parties that rely on the FS

- (1) Type I - risk of incorrect rejection

- Auditors focus only on Type II decision errors in determining their sample sizes, because Type I decision errors affect efficiency and not effectiveness

- Important factors in determining sample size:

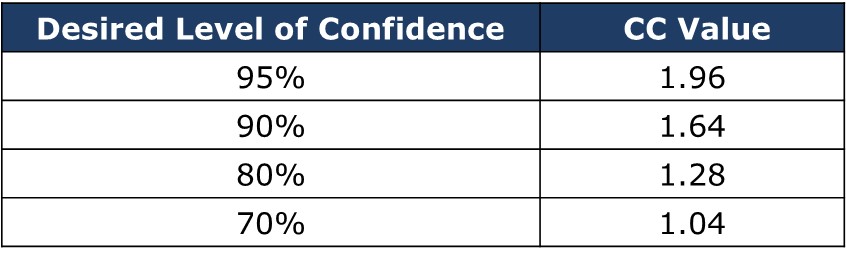

- (1) The desired level of assurance in the results (confidence level)

- (2) Acceptable defect rate (tolerable error)

- (3) The historical defect rate (expected error)

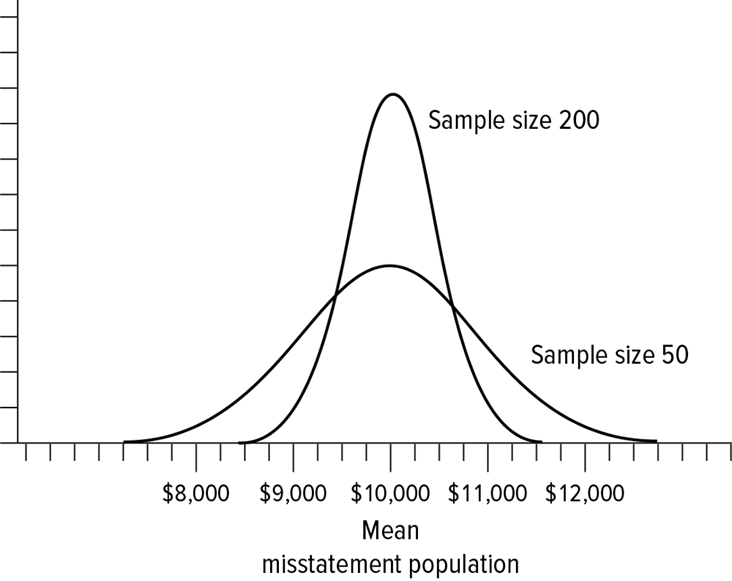

Confidence Level

- Confidence level is the complement of sampling risk

- The auditor may set sampling risk for a particular sampling application at 5%, which results in a confidence level of 95%

Tolerable and Expected Error

- Once the desired confidence level is established, the sample size is determined largely by how much the tolerable error exceeds expected error

- Precision at the planning state of audit sampling is the difference between the expected and tolerable deviation rates

- Auditing standards refer to precision as the “allowance for sampling risk”

Auditing Evidence

To Sample or Not to Sample

- Inspection of tangible assets is when auditors attend the entity’s year-end inventory count

- When there are many items in inventory, the auditor will select a sample to physically inspect and count

- Inspection of records or documents is when certain controls may require the matching of documents

- The procedure may take place many times a day

- The auditor may gather evidence on the effectiveness of the control by testing a sample of the documentation packages

- Reperformance is to comply with PCAOB standards, publicly traded entities must document and test controls over important assertions for significant accounts

- The auditor may reperform a sample of the tests performed by the entity.

- Confirmation is the practice of rather than confirming all customer account receivable balances, the auditor may select a sample of customers

Testing All Items with a Particular Characteristic

- When an account or class of transactions is made up of a few large items, the auditor may examine all the items in the account or class of transaction

- When a small number of large transactions make up a relatively large percent of an account or class of transactions, auditors will typically test all the transactions greater than a particular dollar amount

Testing Only One or a Few Items

- Automated info systems process transactions consistently unless the system or programs are changed

- The auditor may test the general controls over the system and any program changes, but test only a few transactions processed by the IT system

Types of Audit Sampling

- This depends on the firm

- The idea is that it allows us to use probability theory in order to determine a precise error in the account, in the test, in the sample, or in the population – but it doesn’t always work

- Auditing standards recognize and permit both statistical and nonstatistical methods of audit sampling

- (1) In nonstatistical (or judgmental) sampling, the auditor does not use statistical techniques to determine sample size, select the sample items, or measure sampling risk

- (2) Statistical sampling uses the laws of probability to compute sample size and evaluate results

- The auditor can use the most efficient sample size and quantify sampling risk

- Advantages of statistical sampling:

- Design an efficient sample

- Measure the sufficiency of evidence obtained

- Quantify sampling risk

- Disadvantages of statistical sampling:

- Cost of training auditors in proper use

- Cost to design and conduct sampling application

- Lack of consistent application across audit teams

Statistical Sampling Techniques

Attribute Sampling

- Attribute sampling is used to estimate the proportion of a population that possess a specified characteristic

- The most common use of attribute sampling is for tests of controls

- For example:

- The entity’s controls require that all checks have two independent signatures

- The auditors plan a test of that control using attribute sampling

Monetary-Unit Sampling

- Monetary-unit sampling uses attribute sampling theory to estimate the dollar amount of misstatement for a class of transactions or an account balance

- This technique is used extensively because it has several advantages over classical variables sampling

Classical Variables Sampling

- Auditors sometimes use classical variables sampling to estimate the dollar value of a class of transactions or account balance

- It is more frequently used to determine whether an account is materially misstated

Attribute Sampling Applied to Tests of Controls

- In conducting a statistical sample for a test of controls, auditing standards require the auditor to properly plan, perform, and evaluate the sampling application and to adequately document each phase of the sampling application

Planning

- (1) Determine the test objectives

- The objective of attributable sampling when used for tests of controls is to evaluate the operating effectiveness of the internal control

- (2) Define the population characteristics:

- Define the sampling population

- All or a subset of the items that constitute the class of transactions make up the sampling population

- Define the sampling unit

- Each sampling unit makes up one item in the population

- The sampling unit should be defined in relation to the control being tested

- Define the control deviation conditions

- A deviation is a departure from adequate performance of the internal control

- Define the sampling population

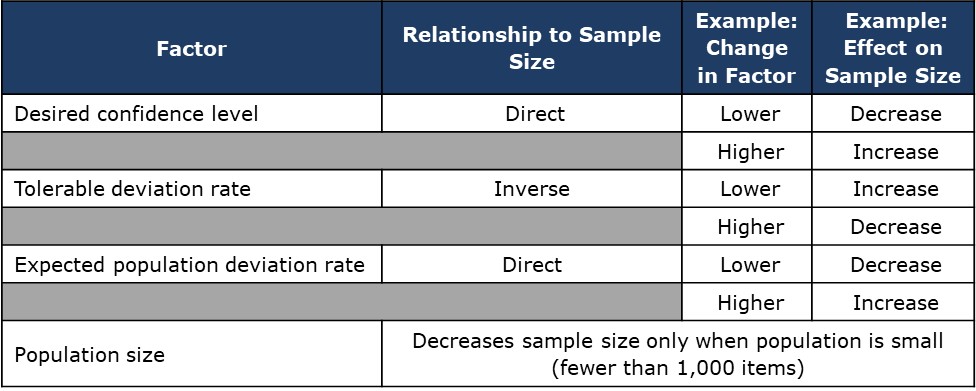

- (3) Determine the sample size using the following inputs:

- The desired confidence level or risk of incorrect acceptance

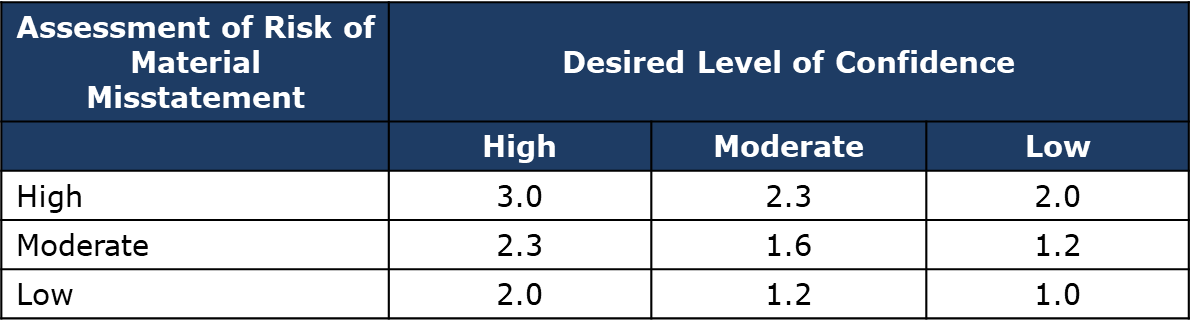

- The confidence level is the desired level of assurance that the sample results will support a conclusion that the control is functioning effectively

- Generally, when the auditor has decided to rely on controls, the confidence level is set at 90% or 95%

- This means the auditor is willing to accept a 10% or 5% risk of accepting the control as effective when it is not

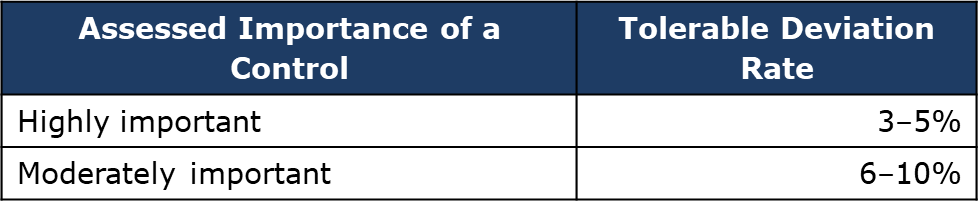

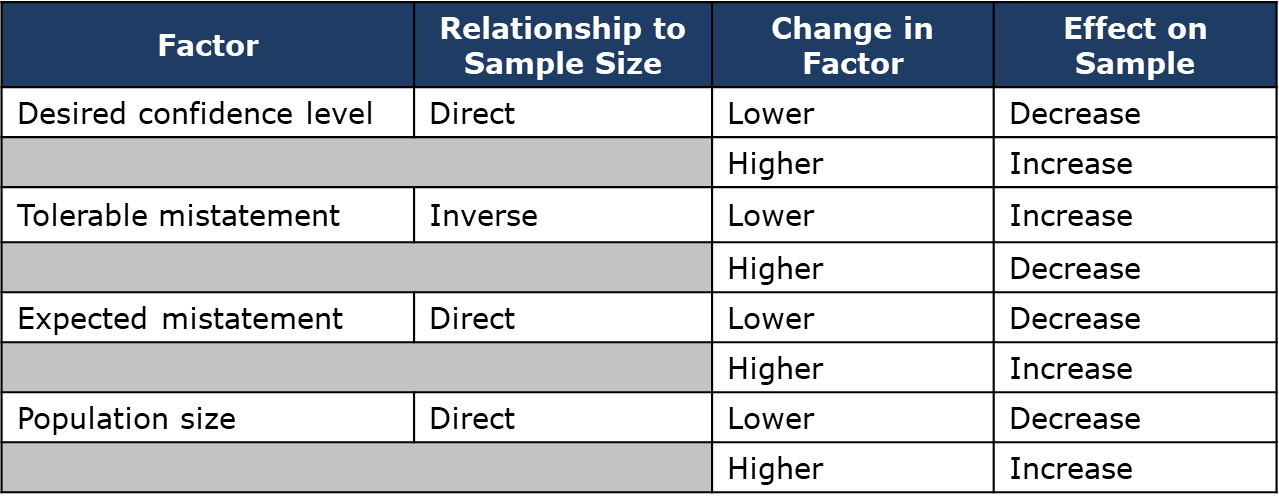

- The tolerable deviation rate is the maximum deviation rate from a prescribed control that the auditor is willing to accept and still consider the control effective

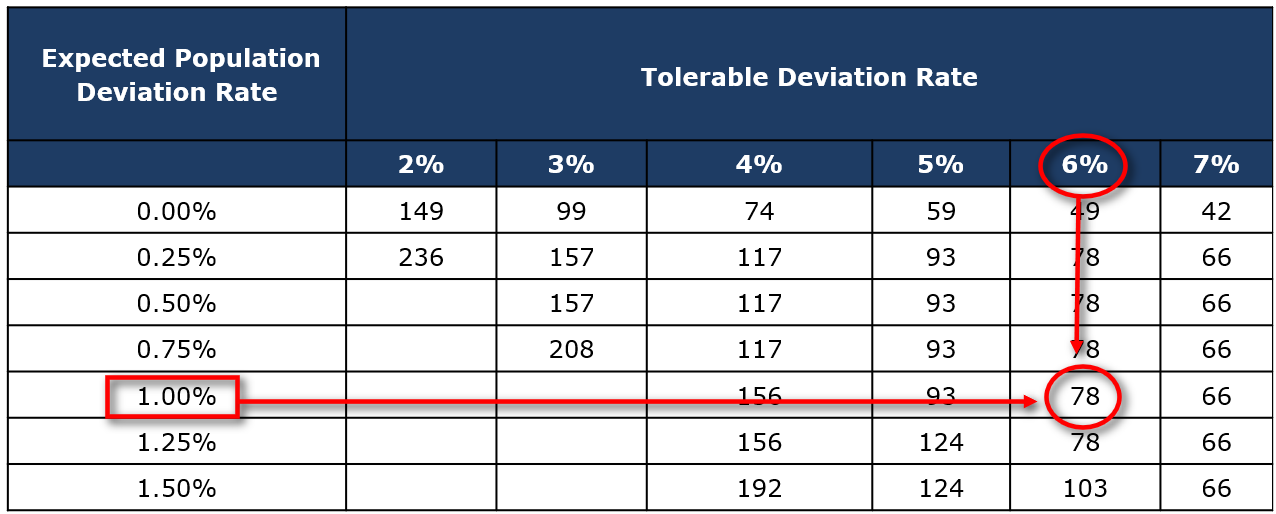

- Example: suggested tolerable deviation rates

- The desired confidence level or risk of incorrect acceptance

- The expected population deviation rate is the rate the auditor expects to exist in the population

- The larger the expected population deviation rate, the larger the sample size must be, all else equal

- Example: assume a desired confidence level of 95%, and a large population, the effect of the expected population deviation rate on sample size is shown below

- The expected population deviation rate is the rate the auditor expects to exist in the population

Population Size: Attributes Sampling

- Population size is not an important factor in determining sample size for attributes sampling

- The population size has little or no effect on the sample size, unless the population is relatively small, say less than 1,000 items

Performance

- (4) Select sample items:

- Random-number selection is when every item in the population has the same probability of being selected as every other sampling unit in the population

- Systematic Selection is when the auditor determines the sampling interval by dividing the population by the sample size

- A starting number is randomly selected in the first interval and then every nth item is selected

- (5) Perform the auditing procedures:

- Voided documents

- Example: assume a sales invoice should not be prepared unless there is a related shipping document

- If the shipping document is present, there is evidence the control is working properly

- If the shipping document is not present, a control deviation exists

- Example: assume a sales invoice should not be prepared unless there is a related shipping document

- Unused or inapplicable documents

- Unless the auditor finds something unusual about either of these items, they should be replaced with a new sample item

- Inability to examine a sample item

- If the auditor is unable to examine a document or to use an alternative procedure to test the control, the sample item is a deviation for purposes of evaluating the sample results

- Stopping the test before completion

- If many deviations are detected early in the tests of controls, the auditor should consider stopping the test, as soon as the results of the test will not support the planned assessed level of control risk

- Voided documents

November 03, 2023

Evaluation

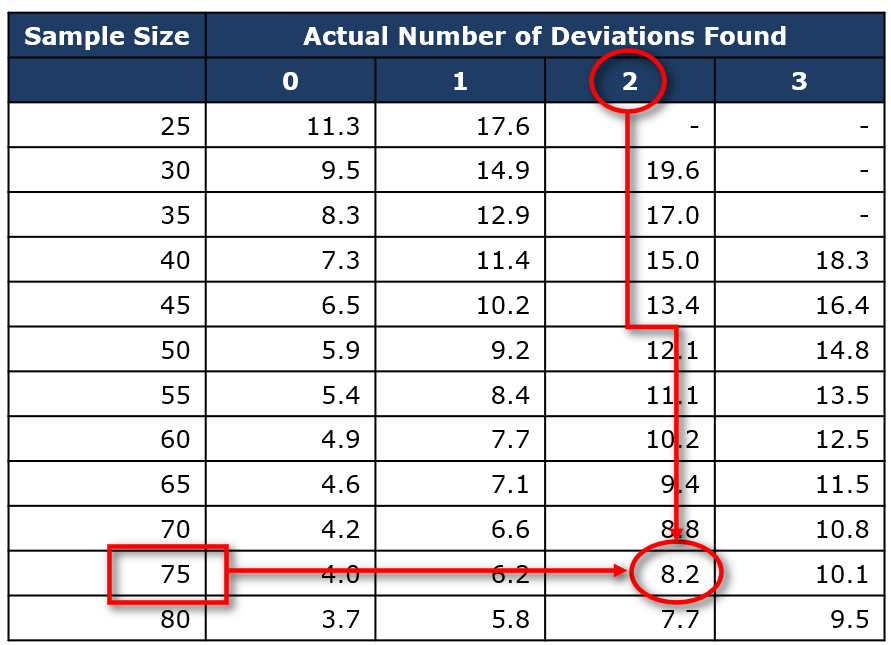

- (6) Calculate the sample deviation and upper deviation rates

- After completing the audit procedures, the auditor summarizes the deviations for each control tested and evaluates the results

- Example: if the auditor discovered two deviations in a sample of 50, the deviation rate in the sample would be 4% (# of deviation/sample size = 2/50)

- The upper deviation rate is the sum of the sample deviation rate and an appropriate allowance for sampling risk

- (7) Draw final conclusions

- The auditor compares the tolerable deviation rate to the computed upper deviation rate

Auditor’s Decision Based on Sample Evidence | True State of Internal Control-Reliable | True State of Internal Control – Not Reliable |

Supports the planned level of control risk | Correct decision | Risk of incorrect acceptance (Type II) |

Does not support the planned level of control risk | Risk of incorrect rejection (Type I) | Correct decision |

Attribute Sampling Example

- The auditor has decided to test a control at Calabro Wireless Services

- The test is to determine that the sales and service contracts are properly authorized for credit approval

- This is a common type of control test

- A deviation in this test is defined as the failure of the credit department personnel to follow proper credit approval procedures for new and existing customers

- The test is to determine that the sales and service contracts are properly authorized for credit approval

- Here is info relating to the test:

- Desired confidence level = 95%

- Overstating sales is an important part of our testing to ensure that all of the sales actually occurred

- Tolerable deviation rate = 6%

- Expected population deviation rate = 1%

- This is based on past experience

- Sample size = 78 contracts

- Desired confidence level = 95%

- Pat of the table used to determine sample size when the auditor specifies a 95% desired confidence level

- If there are 125,000 items in the population numbered from 1 to 125,000, the auditor can use Excel to generate random selections from the population for testing

- The auditor examines each selected contract for credit approval and determines the following:

- Number of deviations = 2

- Sample size = 78

- Sample deviation rate = 2.6% (# of deviation/sample size = 2/78)

- Computed upper deviation rate = 8.2%

- Tolerable deviation rate = 6.0%

- Part of the table used to determine the computed upper deviation rate at 95% desired confidence level:

|

|

Which of the following statements is correct concerning statistical sampling in tests of controls? |

- Deviations from controls at a given rate usually result in misstatements at a higher rate

- There is no linear relationship

- As the population size doubles, the sample size should also double

- Population size does not matter when we do these tests

- Our sample size is based on expected population deviation rate and the tolerable deviation rate

- The qualitative aspects of deviations are not considered by the auditor

- There is an inverse relationship between the sample size and the tolerable deviation rate

Nonstatistical Sampling for Tests of Controls

Determining the Sample Size

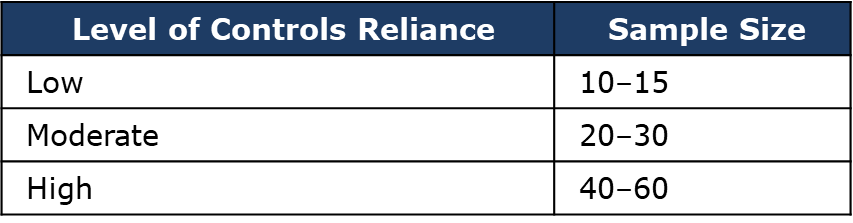

- An auditing firm may establish a non-statistical sampling policy like the one below:

- Such a policy will promote consistency in sampling applications

- We want our sample size to be approximately comparable to the factor tables (we don’t want to go too far below or too far above)

Selecting the Sample Items

- Non-statistical sampling allows the use of random or systematic selection, but also permits the use of other methods (ex: haphazard sampling)

- When haphazard sampling selection is used, sampling units are selected without any bias without a special reason for including or omitting items from the sample

- This is only used under non-statistical sampling

- This is difficult because humans tend to select things that are easy

- Key: have enough samples

Calculating the Upper Deviation Rate

- With a non-statistical sample, the auditor can calculate the sample deviation rate, but cannot mathematically quantify the computed upper deviation rate and sampling risk associated with the test

- Tables can be used to guide conclusions but cannot be used to verify conclusions

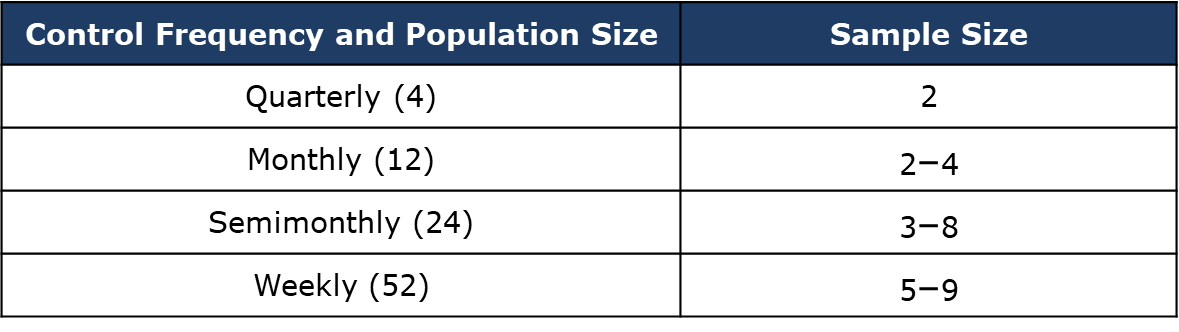

Control Tests for Low Control Frequency

- The sample size tables in the chapter assume a large population

- Sample size can be adjusted using the “finite correction factor” in the Advanced Module or by using the table below for very small populations (control performed less frequently):

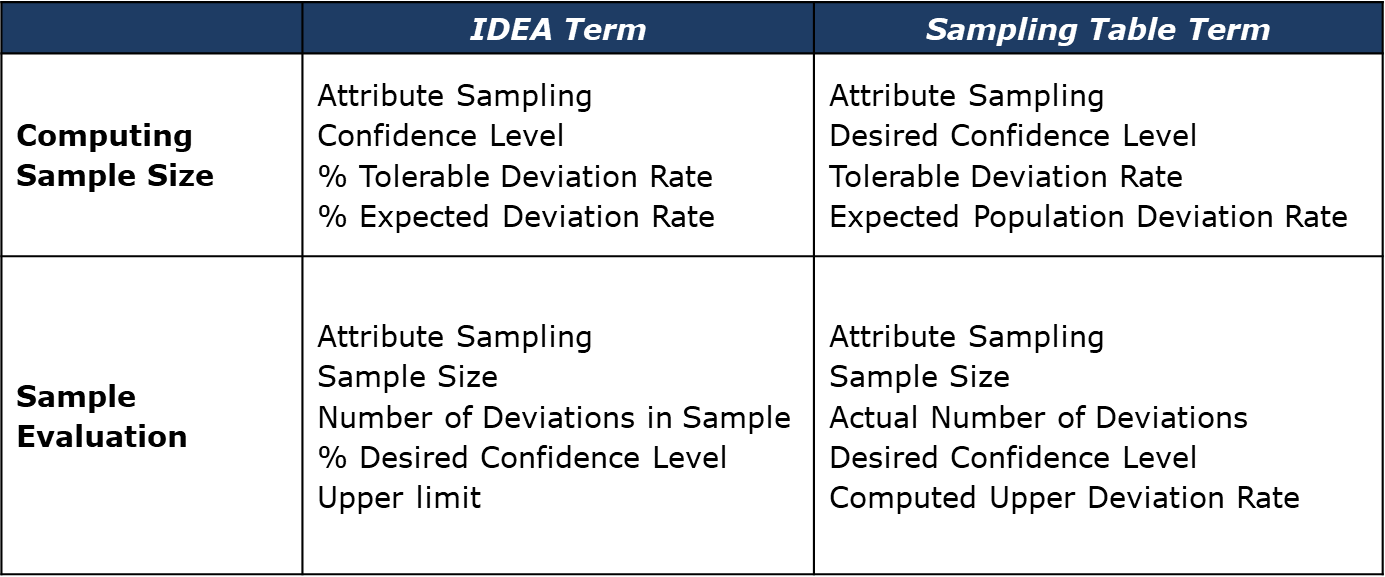

Advanced Module 2: Comparing Terminology for Attributable Sampling between IDEA and Sampling Tables

Audit Sampling: An Application to Substantive Tests of Account Balances

November 06, 2023

Substantive Tests of Details of Account Balances

- The statistical concepts we discussed in the last chapter apply to this chapter as well

- Three important determinants of sample size are:

- (1) Desired confidence level

- (2) Tolerable misstatement

- (3) Estimated misstatement

- Population plays a bigger role in some of the sampling techniques used for substantive testing

- Misstatements discovered in the audit sample must be extrapolated to the population, and there must be an allowance for sampling risk

- Consider the following info about the inventory account balance of an entity:

- The ratio of misstatement in the sample is 2% ($2,000/$100,000)

- This is the sample misstatement

- We can use this ratio (ratio projection) to project what the dollar error in a population is

- Applying the ratio to the entire population produces a best estimate of misstatement of inventory of $60,000 ($3,000,000*2%)

- The ratio of misstatement in the sample is 2% ($2,000/$100,000)

- The results of our audit test depend upon the tolerable misstatement associated with the inventory account

- If the tolerable misstatement is $50,000, we cannot conclude that the account is fairly stated because our best estimate of the extrapolated misstatement is greater than the tolerable misstatement

Monetary-Unit Sampling (MUS)

- MUS uses attribute-sampling theory to express a monetary conclusion rather than a rate of occurrence

- It is commonly used by auditors to test accounts such as AR, loans receivable, investment securities, and inventory

- MUS uses attribute-sampling theory (used primarily to test controls) to estimate the percentage of monetary units in a population that might be misstated and then multiplies this percentage by an estimate of how much the dollars are misstated

Advantages of MUS

- These advantages are important – we need to understand when it is appropriate to use this technique

- When the auditor expects a little misstatement, MUS usually results in a smaller sample size than classical variables sampling

- When applied using the probability-proportional-to-size procedure, MUS automatically results in a stratified sample

- This is a systematic selection process

- MUS does not require the user to make assumptions about the distribution of misstatements

Disadvantages of MUS

- The selection of zero or negative balances generally requires special design consideration

- When more than a few misstatements are detected, the sample results calculations may overstate the allowance for sampling risk

Steps in MUS Application

- Planning

- (1) Determine the test objectives

- (2) Define the population characteristics:

- Define the population

- Define the sampling unit

- Define a misstatement

- (3) Determine the sample size using the following inputs:

- Desired confidence level or risk of incorrect acceptance

- Tolerable misstatement

- Expected population misstatement

- Population size

- Performance

- (4) Select sample items

- (5) Perform the auditing procedures

- Evaluation

- (6) Calculate the extrapolated misstatement and the upper limit on misstatement

- (7) Draw final conclusions

Planning

- (1) Determine the test objectives:

- Sampling may be used for substantive testing to:

- Test the reasonableness of assertions about a financial statement amount (ie., accuracy, existence) – most common use of sampling for substantive testing

- Develop an estimate of some amount

- Sampling may be used for substantive testing to:

- (2) Define the population characteristics

- Population: for MUS, the population is defined as the monetary value of an account balance, such as accounts receivable, investment securities, or inventory

- Sampling unit: an individual dollar represents the sampling unit

- A misstatement is defined as the difference between monetary amounts in the entity’s records and amounts supported by audit evidence

- (3) Determine the sample size

Performance

- (4) Select sample items

- The auditor selects a sample for MUS by using a systematic selection approach called probability-proportional-to-size selection

- Sampling interval = book value of the population/sample size

- Each individual dollar in the population has an equal chance of being selected and items or “logical units” greater than the interval will always be selected

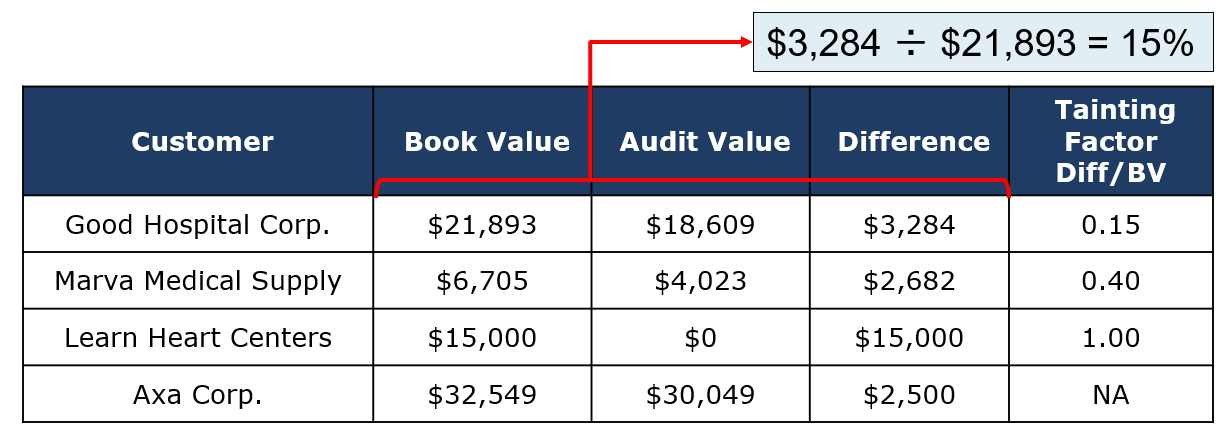

Example: Assume an entity’s book value of AR is $2,500,000, and the auditor determined a sample size of 93. The sampling interval will be $26,882 ($2,500,000 ÷ 93). The random number selected is $3,977, so the auditor would select the following items for testing: |

- Figuring out how we got a sample size = 93

- (a) What percentage of our tolerable misstatement is divided by our total population value?

- TM = 125,000

- Population size = 2,500,000

- Expected misstatement = 25,000

- (b) Change the book values into percentages

- TM = 125,000/2,500,000 = 5%

- Estimated misstatement = 25,000/2,500,000 = 1%

- (c) What sample size do we get when we look at table 8.5?

- With a TM of 5% and estimated misstatement of 1%, we get a sample size of 93

- Figuring out our sampling interval

- BV of population = 2,500,000/93 = $26,882

- Find the cumulative dollar amount (previous total balance + next balance)

- Find the cumulative dollar amount that contains the random sample amount

- In our case, it would be the cumulative value of $17,825

- (a) Add the sampling interval

- We are looking for the $30,859 ($3,977 + $26,882)

- This is found in the cumulative dollar amount $40,683

- (b) Add the sampling interval again

- We are looking for the $57,741 ($30,859 + $26,882)

- This is found in the cumulative dollar amount $77,200

- (5) Perform the auditing procedures

- After the sample items have been selected, the auditor conducts the planned audit procedures on the logical units containing the selected dollar sampling units

Evaluation

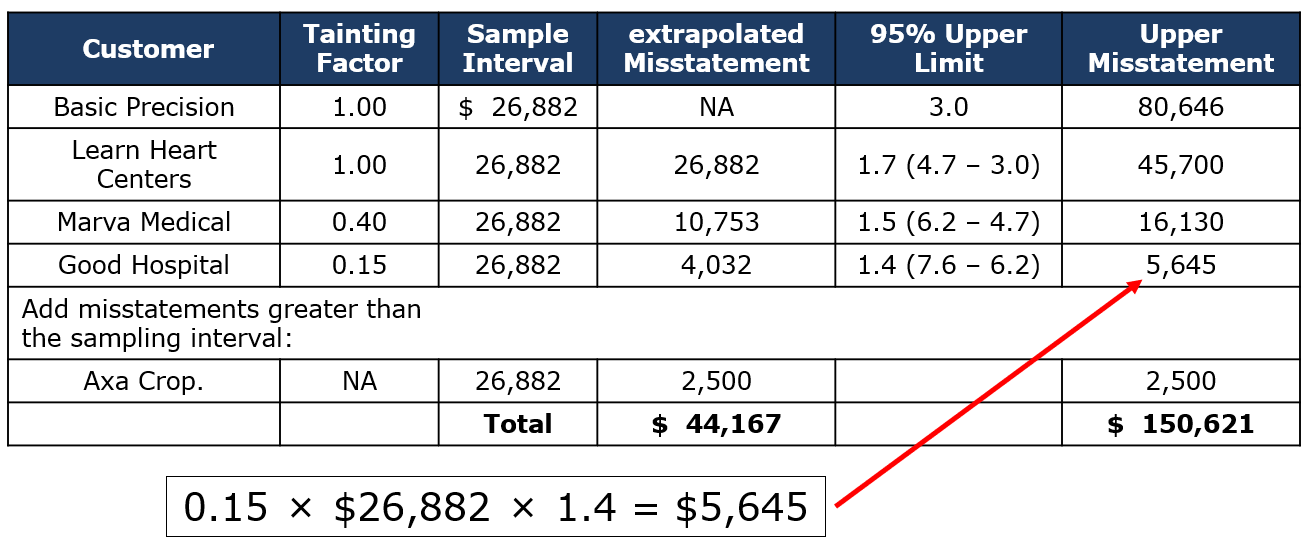

- (6) Calculate the extrapolated misstatement and the upper limit on misstatement

- The misstatements detected in the sample must be extrapolated to the population

Example:

|

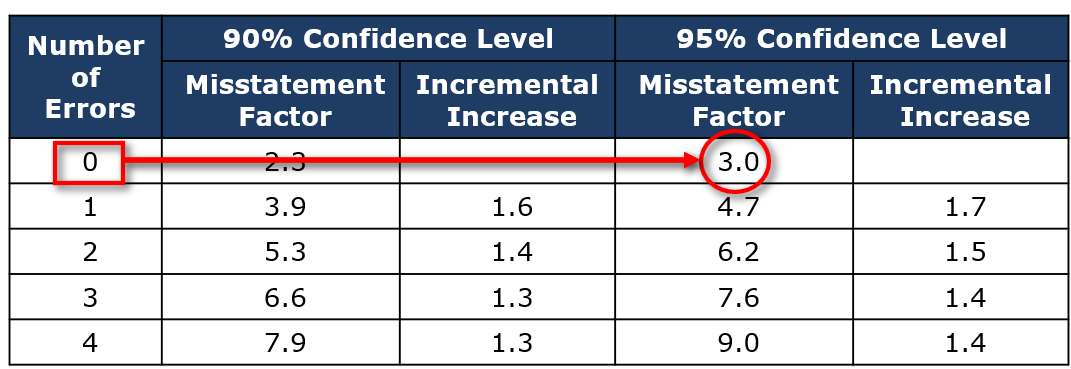

- Basic precision using the table (9.4): if no misstatements are found in the sample, the best estimate of the population misstatement would be $0

- This table is giving us the info we need to calculate the allowance for sampling risk which is added to the extrapolated error that we calculated

- Upper misstatement limit: $26,882 (sampling interval) *3.0 (misstatement factor) = $80,646

- If our upper limit is greater than our tolerable statement = the account is not fairly stated

- Misstatements detected: in the sample of 93 items, the following misstatements were found:

- The tainting factor is the % of misstatements in the logical unit

- Tainting factor = (book value – audit value)/book value

- Because the Axa balance of $32,549 is greater than the interval of $26,882, no sampling risk is added

- Since all the dollars in the large accounts are audited, there is no sampling risk associated with large accounts

- Computed upper misstatement limit: we compute the upper misstatement limit by calculating basic precision and ranking the detected misstatements based on the size of the tainting factor from the largest to the smallest 🡪 see table 9.4

- Basic precision always goes first

- We extrapolate the misstatement (sample interval/tainting factor)

- We use table 9-4 to find the 95% upper limit by finding the increment

- (7) Draw final conclusions

- In our example, the final decision is whether the AR balance is materially misstated or not

- We compare the tolerable misstatement to the upper misstatement limit

- If the upper misstatement limit is less than or equal to the tolerable misstatement = balance is not materially misstatement

Steps in MUS Application

- In our example, the upper misstatement limit of $150,621 is greater than the tolerable misstatement of $125,000, so the auditor concludes that the accounts receivable balance is materially misstated

- When faced with this situation, the auditor may:

- Increase the sample size

- Perform other substantive procedures

- Request the entity adjust the accounts receivable balance

- If management refuses to adjust the account balance, the auditor would consider issuing a qualified or an adverse opinion

Risks When Evaluating Account Balances

Effect of Understatement Misstatements

- MUS is not particularly effective at detecting understatements

- An understated account is less likely to be selected than an overstated account

- The most likely error will be reduced by $2,688 (-0.10*$26,882)

November 08, 2023

Nonstatistical Sampling for Tests of Account Balances

- The sampling unit for nonstatistical sampling is normally a customer account, an individual transaction, or a line item on a transaction

- When using nonstatistical sampling, the following items must be considered:

- (1) Identifying individually significant items

- (2) Determining the sample size

- (3) Selecting sample items

- (4) Calculating the sample results

- Nonstatistical sampling differences from statistical sampling:

- Test objective

- Define population

- Monetary value of the account balance

- When we are defining the sampling unit, our sampling unit may be a customer account, a transaction, line in the transaction (ex: sale discounts, price discounts)

- Misstatement will be the same

- We will extract the large accounts and the remaining amounts will be tested using sampling

- Example: if AR balance is $10,000,000 then we will test 10 accounts greater than $200,000

- The book value of those accounts = $2,400,000

- Proportion = 24% (2,400,000/10,000,000)

- The remaining amounts will be our sample population = $7,600,000 (10,000,000 – 2,400,000)

- Proportion = 76% (7,600,000/10,000,000)

- The book value of those accounts = $2,400,000

Identifying Individually Significant Items

- The items to be tested individually are items that may contain potential misstatements that individually exceed the tolerable misstatement

- These items are tested 100% because the auditor is not willing to accept any sampling risk

Determining the Sample Size and Selecting the Sample

Table 9.6 – confidence factors for nonstatistical sampling (page 316)

- Auditing standards require that the sample items be selected in such a way that the sample can be expected to represent the population

Calculating the Sample Results

- (1) Ratio projection is the method of projecting the sampling results to the population is to apply the misstatement ratio in the sample to the population

- Example: Assume the auditor finds $1,500 in misstatements in a sample of $15,000

- The misstatement ratio is 10% (15,000/1,500)

- If the population total is $200,000, the extrapolated misstatement would be $20,000 (200,000*10%)

- Example: Assume the auditor finds $1,500 in misstatements in a sample of $15,000

- (2) Difference projection is a method that projects the average misstatement of each item in the sample to all items in the population

- Example: Assume misstatements in a sample of 100 items total $300, and the population contains 10,000 items

- Average misstatement is $3 (300/100)

- The extrapolated misstatement would be $30,000 (3*10,000)

- Example: Assume misstatements in a sample of 100 items total $300, and the population contains 10,000 items

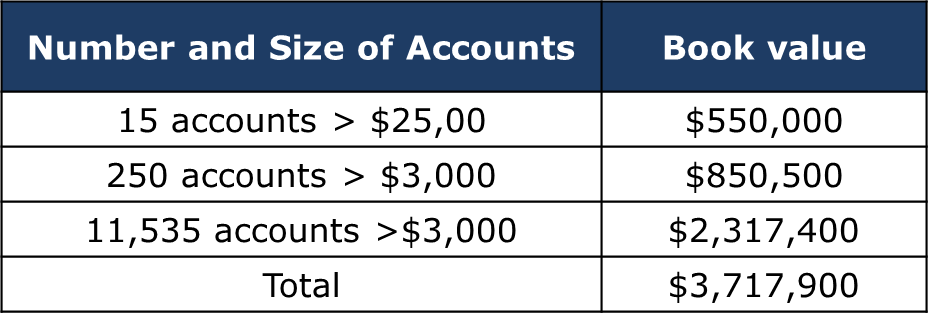

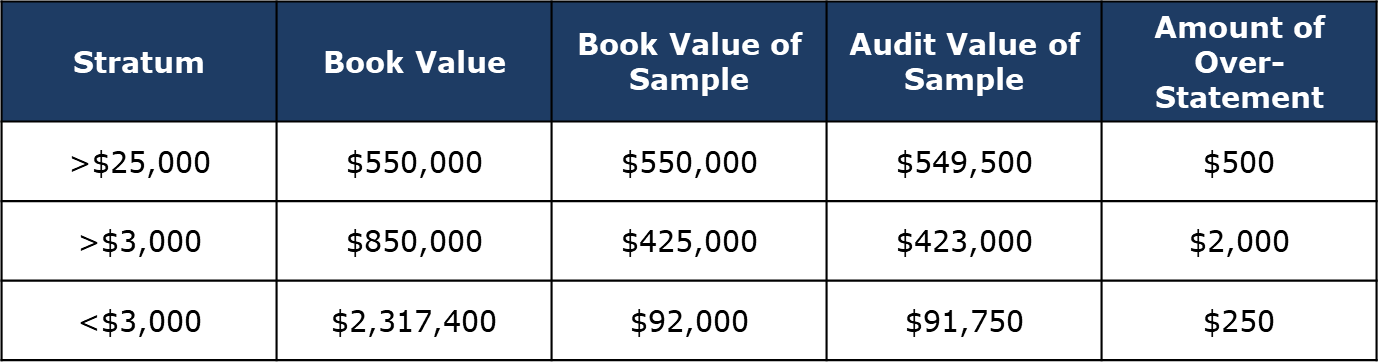

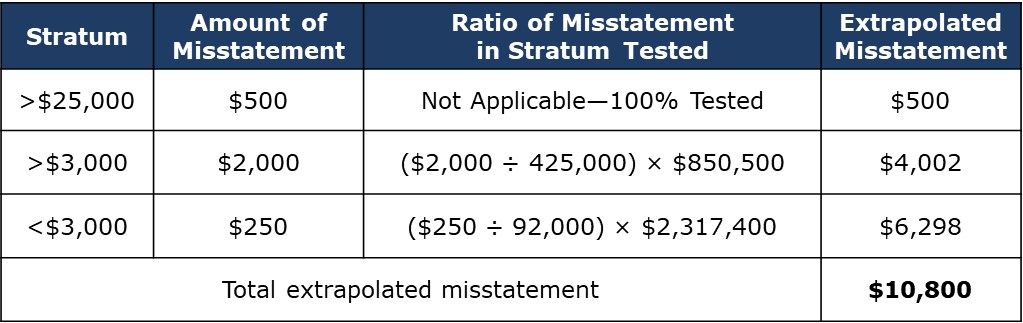

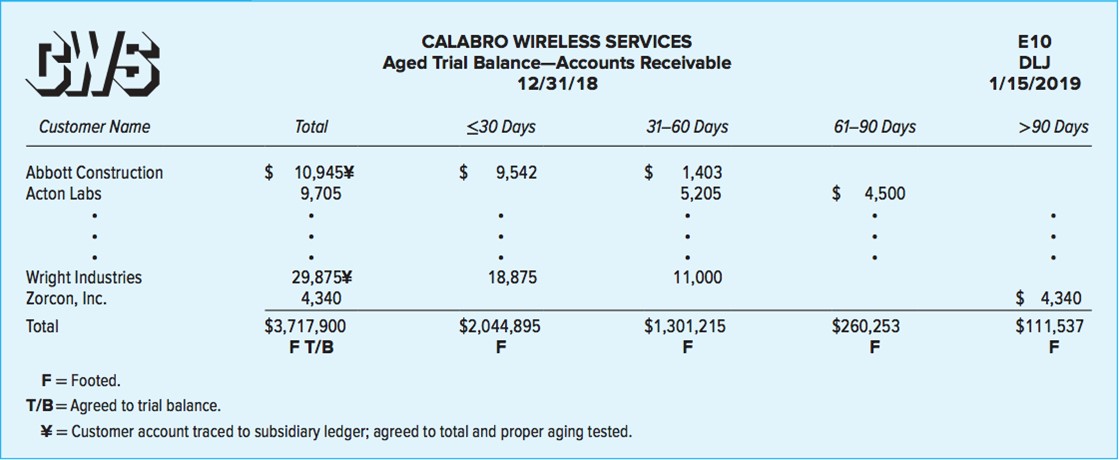

Non-statistical sampling example: The auditors of Calabro Wireless Service have decided to use nonstatistical sampling to examine the AR balance. Calabro has a total of 11,800 (15+250+11,535) accounts with a balance of $3,717,900. |

- The auditors stratify the accounts as follows:

- The auditor decides …

- Based on the results of the tests of controls, the RMM is assessed as low

- The tolerable misstatement is $55,000, and the expected misstatement is $15,000

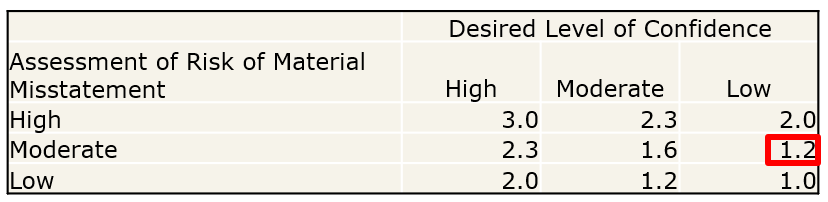

- The desired level of confidence is moderate based on the other audit evidence already gathered

- All customer account balances greater than $25,000 are to be audited

- The auditor sent positive confirmations to each of the 110 (95+15) accounts selected

- Either the confirmations were returned, or alternative procedures were successfully used

- 4 customers indicated that their accounts were overstated, and the auditors determined that the misstatements were the result of unintentional error by entity personnel

- Results of the audit testing:

- When we are doing nonstatistical sampling, we will project the error to the population

- As a result of the audit procedures, the following extrapolated misstatement was prepared: