Microeconomics 1

The basic economic problem

-Scarcity is the basic economic problem, finite resources but infinite wants

So how to allocate scarce resources given unlimited wants?

There are factors of production

1) Capital - man made aids to production (machinery, tractors and vehicles)

2) Enterprise - entrepreneurship, people, risk takers that innovate goods & services to make profit

3) Land - farmland like where goods can be produced

4) Labour - workers to produce

All of these things are finite resources, which forces choices to be made: what to produce,how to produce, and for whom to produce

Opportunity cost - the cost of the next best alternative when a choice is made

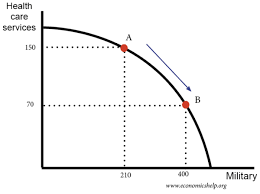

Production possibility frontiers

PPF curve shows:

1) maximum possible production of 2 goods/services with given factors of production

2)various combination of 2 goods/services that can be produced with given factors of production

linear line - constant opportunity cost

concave line - increasing opportunity cost

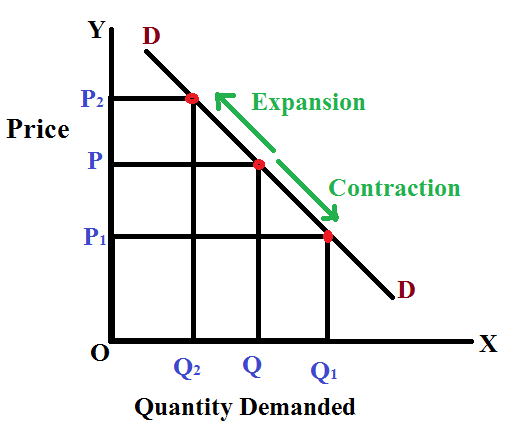

Demand in economics

Demand - the quantity of a good/service consumers are willing & able to buy at a given price in a given time period

An increase in price is a contraction of demand, which makes the price go up, a movement left along the demand curve

A decrease in price is an extension of demand, as there is more quantity demanded, movement right along the demand curve

This is for price related factors

Law of demand - theres an inverse relationship between price and quanitity demanded. As price increases, demand decreases and vice versa. ASSUMING CETERIS PARIBUS - all other factors stay the same.

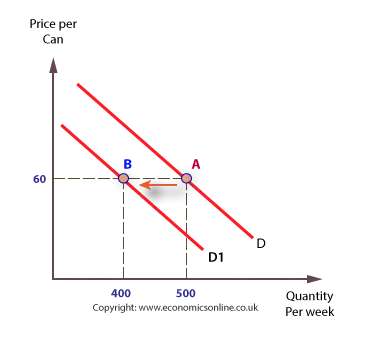

Non price related factors SHIFT the curve, rather than a movement along the curve.

Non price related factors:

Population

Advertising

Substitutes price

Income

Fashion/tastes

Interest rates

Complements price

Non price related increase in demand: right shift

Decrease in demand: left shift

Supply in economics

Supply - the quantity of a good or service producers are willing and able to produce at a given price in a given time period

Law of supply - theres a direct relationship between price & quantity supplied. When price increases, quantity supply increases (assuming ceteris paribus)

There is a direct relationship because of profit motive - if a goes up, theres an opportunity for more profit to be be made

An extension of supply happens when the price goes up, so supply will move right along the curve.

A contraction of supply happens when price decreases, so supply will move left along the curve.

When a non price factor changes supply, the curve will shift.

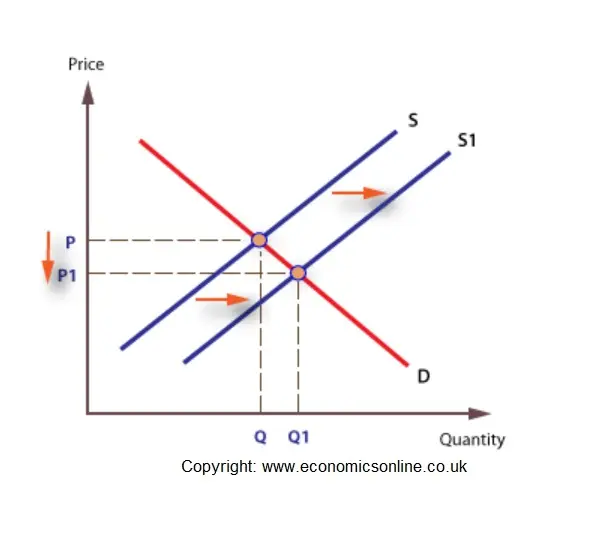

An increase in supply = shifts to the right

A decrease in supply = shifts to the left because producers are less willing and able to produce.

Costs of production:

Productivity

Indirect tax

Number of firms

Technology

Subsidy

Weather

Costs production (utilities, transport, regulation, labour, raw material, oil)

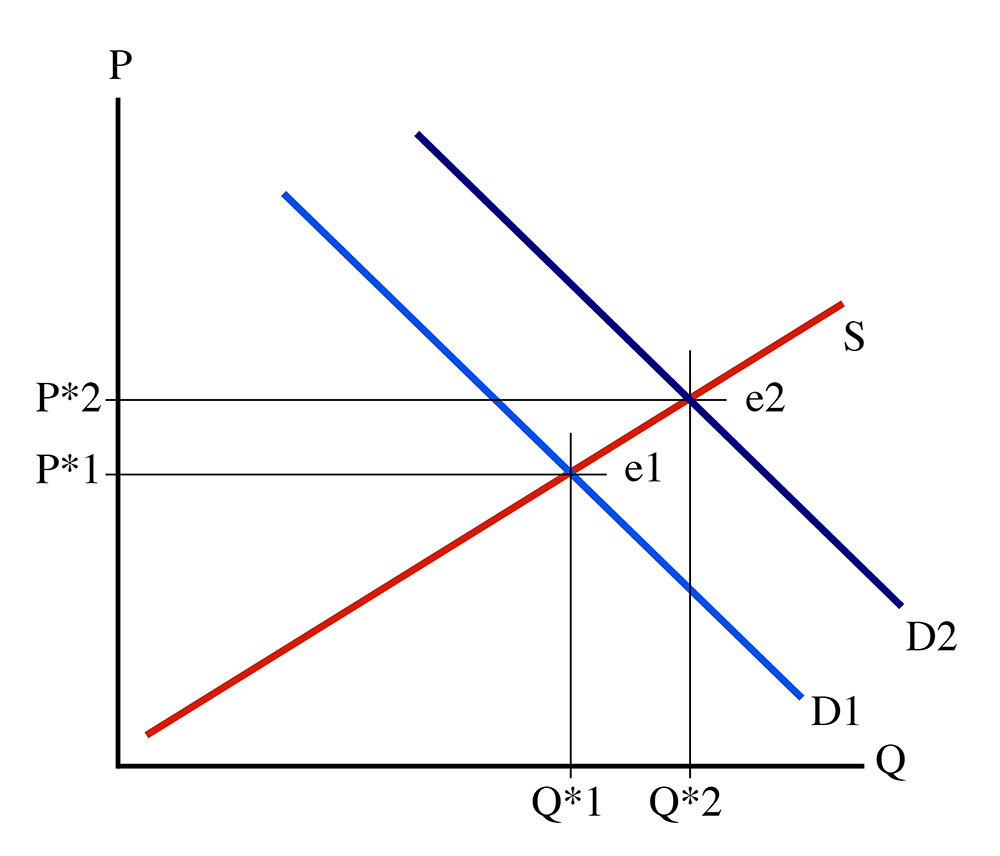

Market equilibrium

Free market - any place where buyers meet suppliers to exchange goods and services, free from market intervention, it can be physical or digital.

Equilibrium - where demand = supply (allocative efficiency)

Disequilibrium is the opposite

Excess demand - prices rise

Excess supply - prices fall