Chapters 28.7-28.8: Money, banking, financial institutions

The Policy Response to the Financial Crisis

The Treasury Bailout: TARP

- In late 2008, Congress passed the Troubled Asset Relief Program (TARP)

- allocated $700 billion to the U.S. Treasury to make emergency loans to critical financial and other U.S. firms

- major recipients: AIG, Citibank, Bank of America, JPMorgan Chase, and Goldman Sachs

- TARP saved financial institutions whose bankruptcy would’ve brought down other financial firms and frozen credit throughout the economy

- demonstrated moral hazard

- moral hazard::

- the tendency for financial investors and financial services firms to take on greater risks because they assume they are at least partially insured against losses

- large firms assumed they were simply too big for government to let them fail which gave them the incentive to make riskier investments

The Fed’s Lender-of-Last-Resort Activities

- Under Fed Chair Ben Bernanke, the Fed designed and implemented new lender-of-last-resort facilities to pump liquidity into the financial system

- this was in addition to both the TARP efforts by the U.S. Treasury and the Fed’s use of standard tools of monetary policy designed to reduce interest rates.

- All the new Fed facilities had the single purpose and desired outcome of keeping credit flowing.

- the Fed bought securities from financial institutions

- The purpose was to ^^increase liquidity in the financial system^^ by exchanging illiquid bonds (that the firms could not easily sell during the crisis) for cash, the most liquid of all assets

- Total Fed assets rose from $885 billion in February 2008 to $1,903 billion in March 2009

- Many economists believe that TARP and the Fed’s actions helped to avert a second Great Depression.

- But they also ^^intensified the moral hazard problem^^ by limiting the losses that would have resulted from bad financial assumptions and decisions

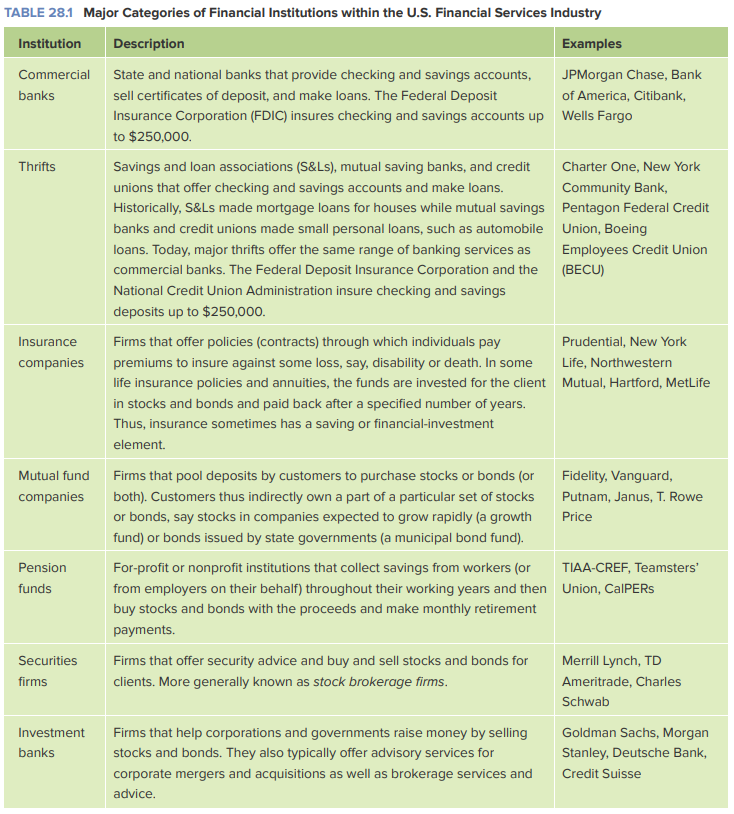

The Postcrisis U.S. Financial Services Industry

- the main categories of the financial services industry are

- commercial banks

- thrifts

- insurance companies

- mutual fund companies

- pension funds

- security firms

- investment banks

- financial services industry::

- The broad category of firms that provide financial products and services to help households and businesses earn interest, receive dividends, obtain capital gains, insure against losses, and plan for retirement.

- before the financial crisis of 2007–2008, the financial services industry was consolidating into fewer, larger firms, each offering a wider spectrum of services.

- In 1999, Congress ended the Depression-era prohibition against banks selling stocks, bonds, and mutual funds.

- even when institutions take on services in more than 1 category, the main lines of a firm’s businesses often are in one category or another

- ex. even though Goldman Sachs is licensed and regulated as a bank, it is first and foremost an investment company

- In mid-2010 Congress passed and the president signed the Wall Street Reform and Consumer Protection Act which included:

- Eliminate the Office of Thrift Supervision and give broader authority to the Federal Reserve to regulate all large financial institutions.

- Create a Financial Stability Oversight Council to be on the lookout for risks to the financial system.

- Establish a process for the federal government to liquidate (sell off) the assets of failing nonbank financial institutions, much like the FDIC does with failing banks.

- Provide federal regulatory oversight of mortgage-backed securities and other derivatives and require that they be traded on public exchanges.

- Require companies selling asset-backed securities to retain a portion of those securities so the sellers share part of the risk.

- Establish a stronger consumer financial protection role for the Fed through creation of the Bureau of Consumer Financial Protection.

- Proponents of the law say that it will help prevent many of the practices that led up to the financial crisis of 2007–2008

- sends a warning to stockholders, bondholders, and executives of large financial firms that they’ll suffer high losses if they get into financial trouble again

- Skeptics of the law say that regulators already had all the tools they needed to prevent the financial crisis.

- government’s own efforts to promote home ownership, via quasi-government institutions that purchased mortgage-backed securities, greatly contributed to the financial crisis

- Critics of the law say that it will simply impose heavy new regulatory costs on the financial industry while doing little to prevent future government bailouts