Ch 5 - Supply

Supply: the quantity of a good or service that producers are willing and able to supply at different prices in a given time period

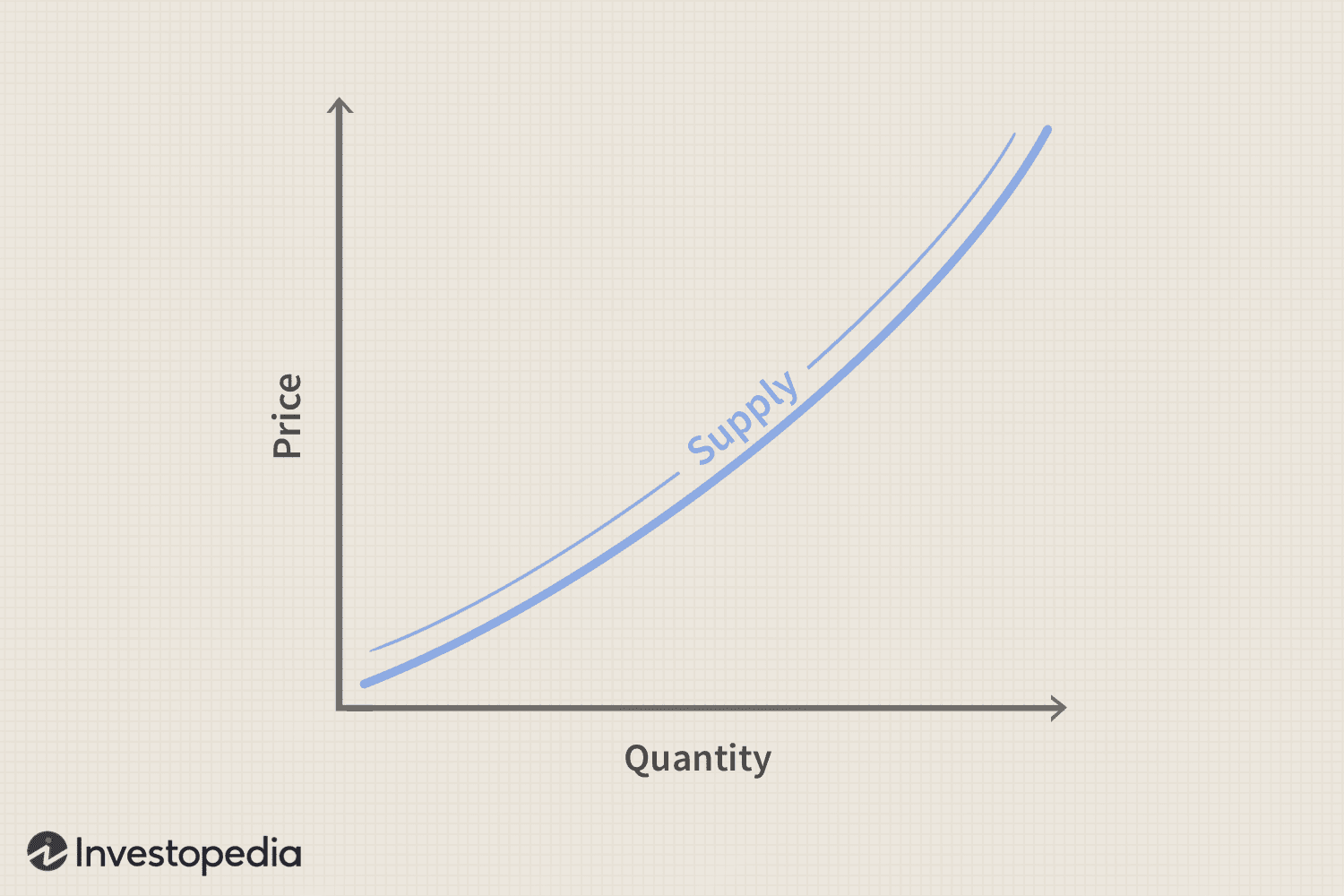

Law of supply: as the price of a product rises, the quantity supplied of the product will eventually increase

- The supply curve normally slopes upwards

- Price rises but costs don't change → profitability increases → supply more

Supply curve: represents the relationship between the price and the quantity supplied of a product

- Non-price determinants of supply:

- Changes in factors of production: (supply shifts to left) → land, labour, capital, entrepreneurship

- Improvements in tech (supply shifts to the right)

- Expectations: supply increases if product is expected to gain profit

- Indirect taxes → increase costs → supply shifts left

- Competition: if another product is produced with higher profit, supply for existing product decreases

- Subsidies → reduce costs → supply shifts right

- More firms → supply shifts to the right → more being supplied at each price level

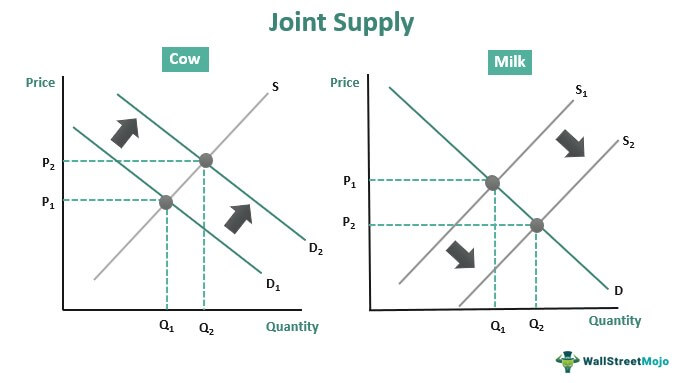

- Joint supply:

The law of diminishing marginal returns: as more variable factors are added to a given quantity fixed factors, holding tech constant, marginal product eventually drops

Fixed factor: employment remains constant

Variable factor : employment increases as output increases

Short run: period with fixed + variable factors

- firms can expand output by employing variable factors only

Long run: period when all factors are variable

- firms can expand output by increasing the use of all factors

Marginal Product (MP): change in total product as a result of change in input

- Formula: MP of the nth unit = TP of n units - TP of (n-1) units

- MP = △TP /△V

Why does this happen?

- Workers fully utilise fixed factors initially so MP rises

- when more workers are added, too many workers relative to the amount of fixed factors, MP eventually drops

Total product: total output that a firm producers using variable and fixed factors in a given time period

Average product: output that is produced, an average, by each unit of the variable factors

- Formula: AP = TPV

Rules:

- As supply increases, price decreases, and demand increases

- As supply decreases, price increases, and demand decreases