B4555 - Chapter 20

Legal Liability

December 4, 2023

Overview

- There are 4 general stages in the initiation and disposition of audit-related disputes:

- (1) The occurrence of events that result in losses for users of the FS

- (2) The investigation by plaintiff attorneys before filing a suit o link the user losses with allegations of material omissions or misstatements of FS

- (3) The legal process that commences with the filing of the suit

- (4) The final resolution of the dispute

- Classes of law:

- (1) Common law – case law developed over time by judges

- (2) Statutory law – written law enacted by the legislative branch of government

Key Legal Terms

- Breach of contract is when a client or auditor fails to meet the terms and obligations established in a contract (expressly or implied), which are normally finalized in the engagement letter

- Third parties may have privity or near-privity of contract

- Civil law all law that does not relate to criminal matters

- Class action is a lawsuit filed by one or more individuals on behalf of all persons who may have invested on the basis of the same false and misleading info

- Criminal law is statutory law that defines the duties citizens owe to society and prescribes penalties for violations

- Fraud are actions taken with the knowledge and intent to deceive

- Gross negligence is an extreme, flagrant, or reckless departure from professional standards of due care

- Aka., constructive fraud

- Ordinary negligence is an absence of reasonable or due care in the conduct of an engagement

- Due care is evaluated in terms of what other professional accountants would have done under similar circumstances

- Privity is the fact that a contract or specific agreement exists only between the parties directly involved

- Absent a contractual or fiduciary relationship, the accountant does not owe a duty of care to be injured partly

- Scienter is acting with intent to deceive, defraud, or with knowledge of a false representation

- Tort is a wrongful act, other than a breach of contract, for which civil action may be taken

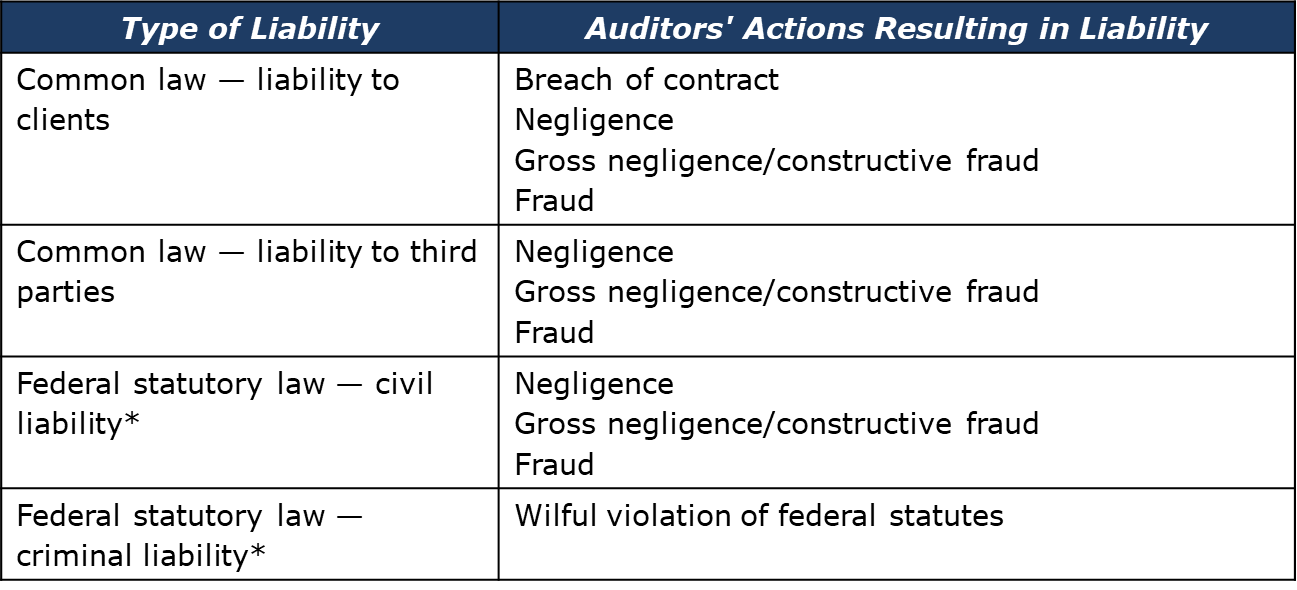

Table 20.2 – Summary of Types of Liability and Auditors’ Actions Resulting in Liability

| *Auditors may also be civilly and criminally liable under provincial statues. Coverage of liability under specific provincial statutes is beyond the scope of this book Note: review this |

Common Law – Clients

- Requires due care

- Follow the process & procedures

- Use your common sense for accounting – your work should speak for itself

- Types of liability to the client:

- (1) May be held liable for breach of contract

- (2) Negligence, gross negligence, fraud

- Note: these two points are important

- Note: refer to case laws

Breach of Contract

- Breach of contact liability is based on the auditor’s failing to complete the services agreed to in the contact with the client

Negligence

- Negligence is if an engagement is performed without due care, the CPA may be held liable for an actionable tort in negligence

- Does not require due care

Note: everything under this was not talked about in class

Common Law Negligence – Client

- Client must prove:

- (1) A duty was owed to the client

- (2) Failure to act in accordance with that duty

- (3) A causal connection between the auditor’s negligence and the client’s damage

- (4) Actual loss or damage to the client

- Auditor’s defense:

- (1) No duty was owed to the client

- (2) The client was negligent

- (3) The auditor’s work was performed in accordance with professional standards

- (4) The client suffered no loss

- (5) Lack of casual connection between auditor negligence and the client loss

- (6) The claim is invalid because the statute of limitations has expired

Common Law – Third Parties Ordinary Negligence

- Four legal standards for third parties:

- (1) Privity

- (2) Near privity are third parties whose relationship with the CPA approaches privity

- (3) Foreseen third parties are third parties whose reliance should be foreseen, even if the specific person is known to the auditor

- (4) Reasonably foreseeable third parties are third parties whose reliance should be reasonably foreseeable, even if the specific person is unknown to the auditor

Fraud

- Fraud is if an auditor has acted with knowledge and intent to deceive a third party

- Some courts have interpreted gross negligence as an instance of fraud

- Third party must prove:

- (1) A false representation by the CPA

- (2) Knowledge or belief by the CPA that the representation was false

- (3) The CPA intended to induce the third party to rely on the false representation

- (4) The third party relied on the false representation

- (5) The third party suffered damages

Provincial Securities Commissions

- The Canadian provinces and territories each have their own securities commission or authority

- These provinces and territory regulators joined to form Canadian Securities Administrators, an umbrella organization, with the intent to harmonize securities regulations

Provincial Statutory Legislation

- As securities regulation falls under provincial legislation, auditors look to two national self-regulatory organizations for guidance

- (1) Investment industry regulatory organization of Canada (IIROC)

- (2) Mutual fund dealers’ association (MFDA)

Stock Exchanges in Canada

- Toronto Stock Exchange (TSX)

- Canadian Securities Exchange

- Montreal Exchange

- NASDAQ Canada

- NEO Exchange

- TSX Venture Exchange

US Impact on Canada

- There are a significant number of Canadian companies listed on the US Exchanges

- Canadian auditors need to understand the landscape of American securities rules and regulations

Securities Exchange Act of 1934

- Negligence third party must prove:

- (1) The auditor had a duty to the plaintiff of exercise due care

- (2) The auditor breached that duty by failing to act with due professional care

- (3) There was a direct casual link between the auditor’s negligence and the third party’s injury

- (4) The third party suffered an actual loss as a result

- Negligence auditor’s defense:

- (1) No duty was owed to the third party (level of duty required depends on the case law followed by the courts)

- (2) The third party was negligent

- (3) The auditor’s work was performed in accordance with professional standards

- (4) The third party suffered no loss

- (5) Lack of casual connection between auditor negligence and the client loss

- (6) The claim is invalid because the statute of limitations has expired

Statutory Liability

- There are 3 major statutes that provide sources of statutory liability for auditors:

- (1) Securities Act of 1933

- (2) Securities Exchange Act of 1934

- (3) Sarbanes-Oxley Act of 2002

Securities Act of 1933

- Regulates the disclosure of info in a registration statement for a new public offering of securities

- Section 11 imposes a liability on issuers and others, including auditors, for losses suffered by third parties when false or misleading info is included in a registration statement

- Third party must prove:

- (1) The third party suffered losses by investing in the registered security

- (2) The audited FS contained a material omission of misstatement

- Burden of proof is shifted to the auditor to prove that they were not negligent

Securities Exchange Act of 1934

- Concerned with ongoing reporting by companies whose securities are listed and traded on a stock exchange – covers all documents filed with the SEC

- Section 18 imposes liability on any person who makes a materially false or misleading statement in documents filed with the SEC

- Section 10(b) and Rule 10b-5 are the greatest source of liability for auditors under this act

- Third party must prove:

- (1) A material, factual misrepresentation, or omission

- (2) Reliance on the FS

- (3) Damages suffered as a result of reliance on the FS

- (4) Scienter (gross negligence or recklessness may be enough)

Sarbanes-Oxley Act of 2002

- Creation of PCAOB

- Stricter independence rules

- Audits of internal controls

- Increased reporting responsibilities

- Most sweeping securities law since 1934

Canadian Business Corporations Act “CBCA”

- Liability structure defined to be a modified proportionate liability with respect to certain financial info of a CBCA corporation

- If an auditor is found responsible for financial loss, their damages are limited to their degree of responsibility for the loss

Foreign Corrupt Practices Act (FCPA)

- Passed in 1977 in response to the discovery of bribery and other misconduct on the part of more than 300 American companies

- An auditor may be subject to administrative proceedings, civil liability, and civil penalties

- Auditing standards required violations of the FCPA to be communicated to management immediately

- To mitigate corruption and bribery in Canada, there are 2 Canadian laws:

- (1) The Corruption of Foreign Public Officials Act – prohibit bribes to or from foreign public officials

- (2) The Criminal Code – prohibits various forms of corruption

Criminal Liability

- Auditors can be held criminally liable under the laws discussed in the previous section

- Criminal prosecutions require that some form of criminal intent be present (ex: fraud)

- However, gross negligence can also be deemed criminal