TOPIC 5: Price Elasticity, Income Elasticity, Cross Elasticity, & Elasticity of Supply

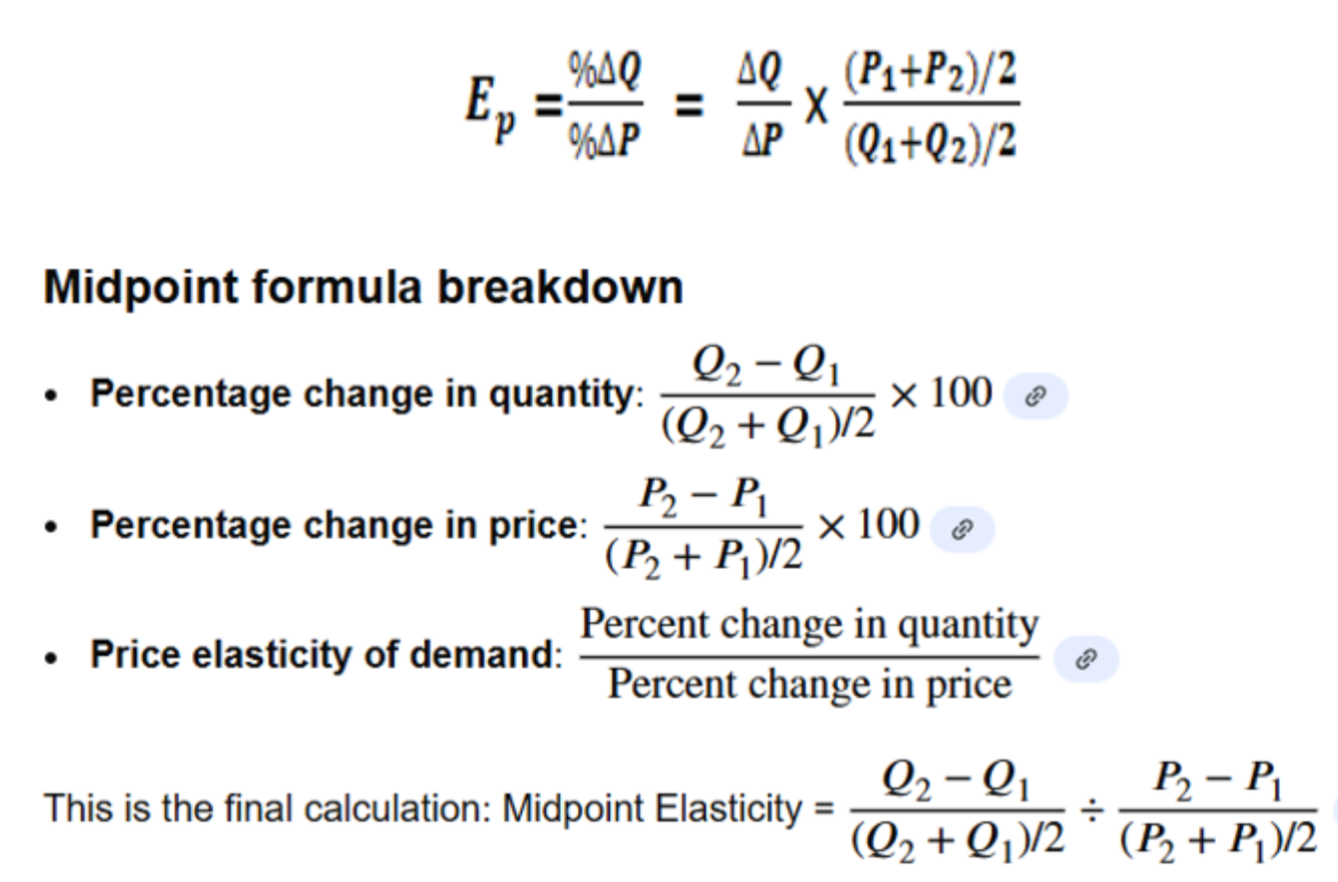

Price Elasticity

Elastic when the percentage change in price resulted in a larger percentage change in quantity demanded or supplied (responsive)

Inelastic when the percentage change in price resulted in a smaller percentage change in quantity demanded or supplied

Unit Elastic when the percentage change in price resulted in an equal percentage change in quantity demanded or supplied

Perfectly elastic when a small change in price might cause the consumers or producers to be highly responsive

Perfectly inelastic means consumers and producers are not responsive at all to any price changes

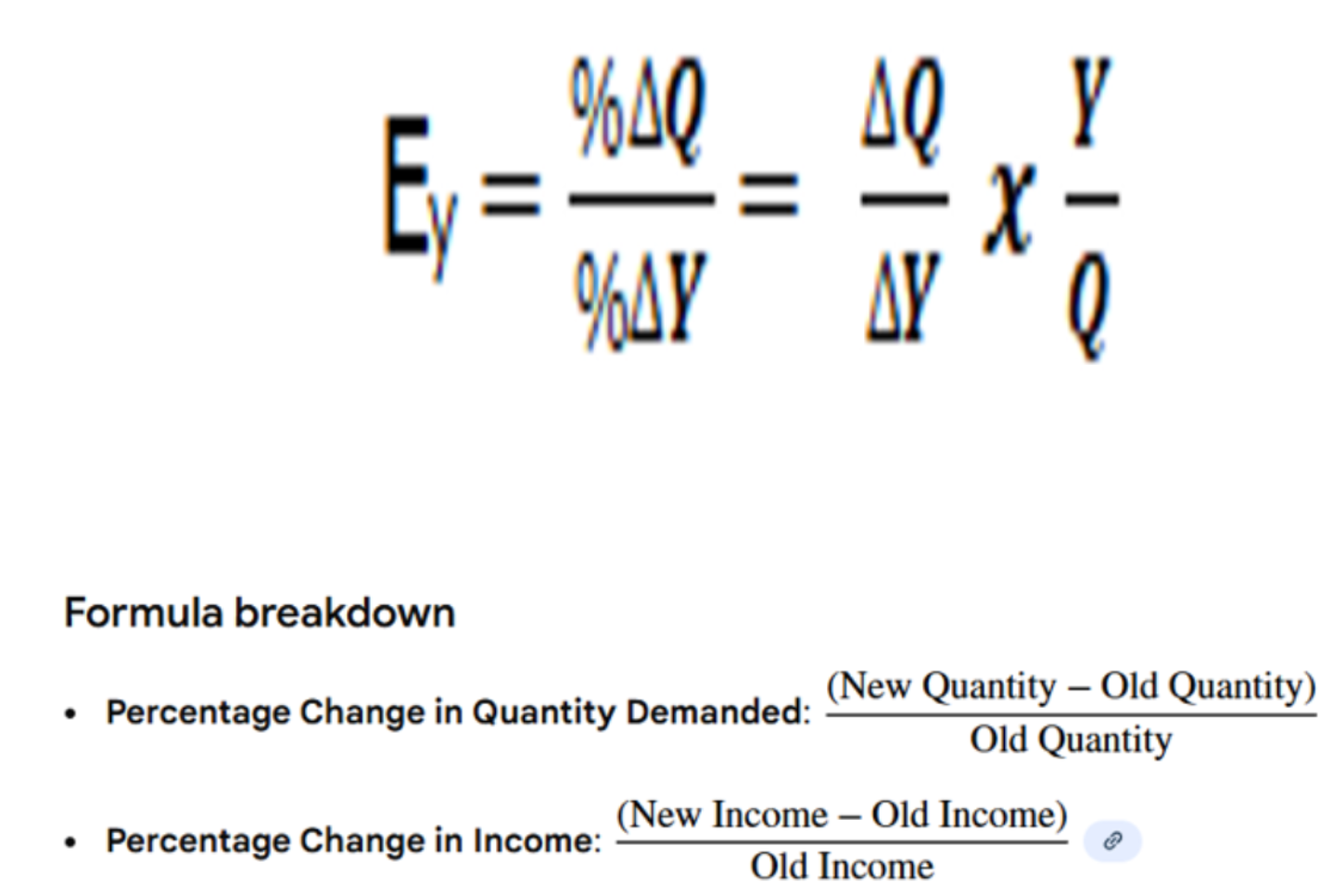

Income Elasticity

Income elasticity of Demand is the percentage change in quantity demanded caused by a 1 percent change in income. Y = income

Income-Elastic: positive income elasticity (normal good - luxury)

Ey > 1

(%) Quantity demanded > (%) Income

Income-Inelastic: positive income elasticity (normal good - necessity)

0 < Ey < 1

(%) Quantity demanded < (%) Income

Negative Income Elasticity: inferior good

Ey < 0

When quantity demanded decreases as income increases

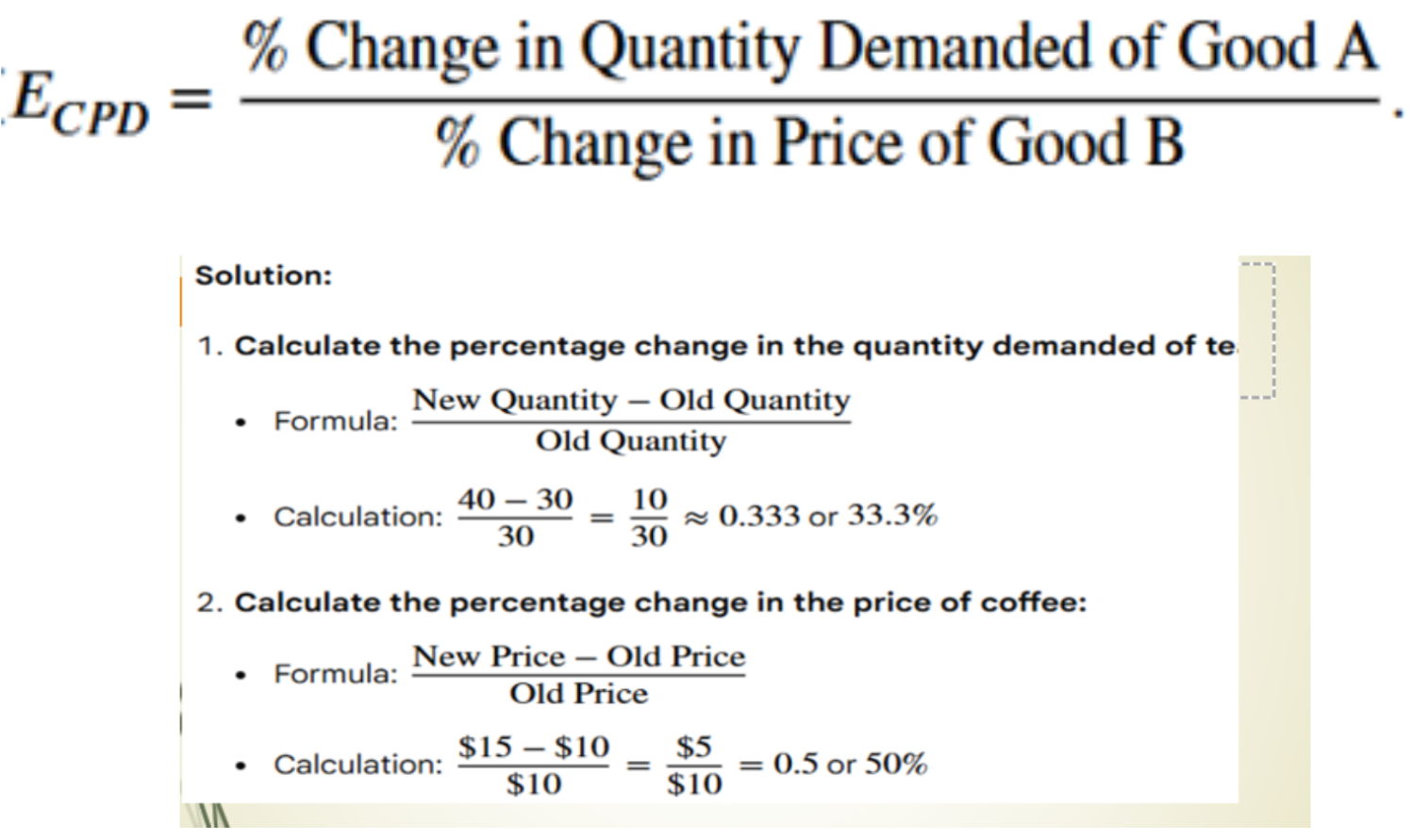

Cross Elasticity

Cross Elasticity of demand shows the percentage change in the quantity demanded of one good when the price of another good changes

Substitutes (+) A price increase in one leads to a rise in demand for the other

Exy > 0

Complements (-) A price increase in one leads to a decrease in demand for the other

Exy < 0

Non-related: A change in the price of one does not affect the demand for the other

Exy = 0

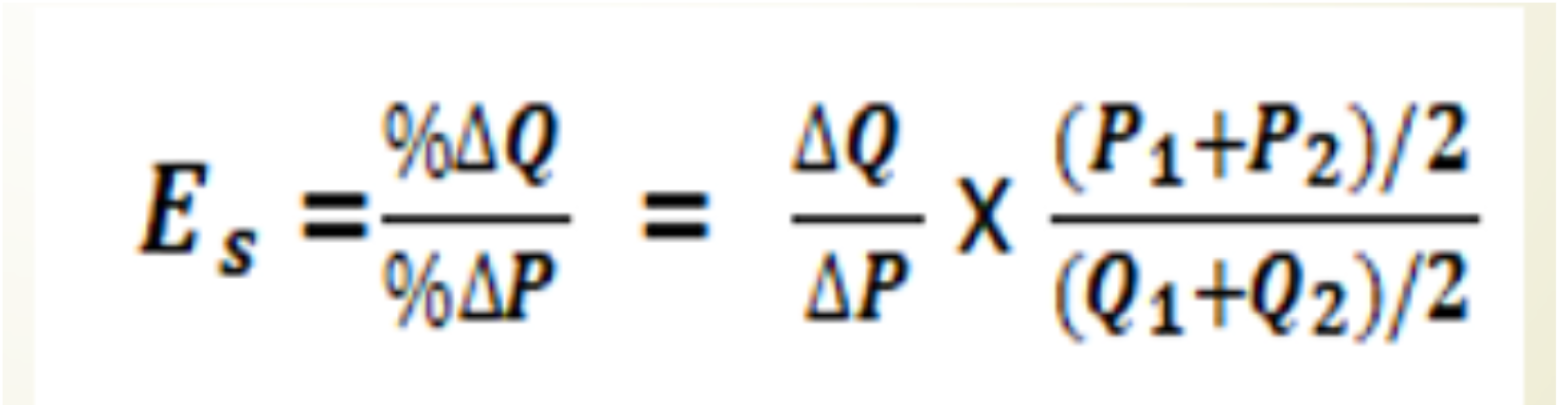

Elasticity of Supply

Price elasticity of supply is the measure of the responsiveness of the quantity supplied of a good to changes in price

Perfectly Inelastic Supply

Es = 0 (absolutely unresponsive)

Unique Goods that have no substitutes or alternatives

Inelastic Supply: the producers limit their production even if the price increases

The percentage change in price is insignificant

0 < Es < 1

(%) Quantity demanded < (%) Price

Unit Elastic

Es = 1

Elastic Supply: There is an increase in output produced, even if the cost incurred by the entrepreneur in making the good increases

There is a considerable increase in the price of goods being sold

Es > 1

(%) Quantity demanded > (%) Price

Perfectly Elastic Supply

Es = ∞

Determinants of the Price Elasticity of Supply

Length of Time: the shorter the time period, the more inelastic the supply for a product, because it is harder to get additional inputs to increase production. Inversely, a longer time period results in an elastic supply

Production Capacity:

A flexible production capacity is more elastic

An inflexible production capacity is more inelastic