Ch 3 - Demand

Market: where buyers and sellers get together to trade

- Housing market (goods and services)

- Stocks (shares)

- Factor (factors of production)

- International markets (international currencies)

Demand: the quantity of a product which consumers are willing and able to buy

Quantity: numerical quantity of a product being demanded

Effective demand: by purchasing power, the purchaser has the money to pay for the product

Ineffective demand: do not have purchasing power

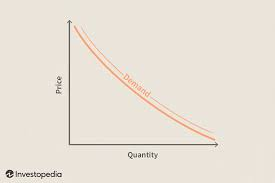

- Law of demand: states that as the price of product falls, the quantity demanded will increase

Based on the graph, we can see these trends:

- When the price goes up, there's a decrease in quantity demanded

- When price goes down, quantity demanded increases

Factors influencing demand (PINTE):

- Income: the income of all consumers

a. Income + demand have a positive relationship: * Increase in ability to pay equals increase in demand, If the ability to pay falls then less is demanded (direct relationship) * Inferior goods have a negative relationship (customers buy less, inverse relationship)

Price:

- Substitutes: alternative goods can satisfy the same want and need

- A change in the price of one has an impact on the demand

- Complements: goods which have a joint demand as they enhance the satisfaction derived from another good

- A change in the price/availability of either will have an effect on the demand for complementary goods

- Substitutes: alternative goods can satisfy the same want and need

Fashion, taste, and attitude: demand is affected by personal behaviour /preference. As consumer behaviour and preference changes, so does the degree of demand of a good or service.

- To increase demand:

- Income rises (normal goods)

- Price of substitution rises

- Price of complementary falls

- Encouraged buying

- Population likely to buy increases

- To decrease demand:

- Income drops

- Substitution falls

- Compliments rises

- Buying discouraged

PINTE:

- Prices

- Income

- Number of buyers

- Taste/preference

- Expectations

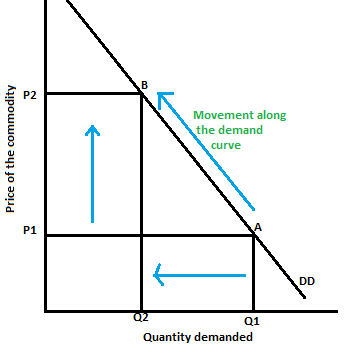

Movement along the Demand curve:

- Rise in price = drop in demand

- Drop in price = increase in demand

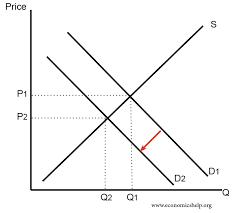

A demand shift can shift:

- Left (decrease demand)

- Right (increase demand)

Based on the graph, we can tell that these changes occur in the economy:

- D2: how quantity demanded responds to a change in prices

- D1 and D2: shows how demand responds to a change in a non-price factor

Bounded rationality: theory that consumers have limited rational decision making driven by cognitive ability, time constraint, and imperfect information

- Profit: total revenue - total costs

- Status quo: overwhelming amount of choices

- Complementary goods: demand decreases, quality demand decreases

- Substitute goods: demand increases, quality demanded decreases

Basic rules of movement along the demand curve and what it means:

- decrease in price = expansion in demand = increase in quality demanded

- increase in price = contraction in demand = decrease in quantity demanded