Chapter 1: Business Decisions and Financial Accounting

Objective 1.1: Describe various organizational forms and business decision makers.

The Three Types of Businesses

- 1.) Sole Proprietorship

- Business that is .

- The owner is liable for the debts of the business.

- It is the easiest form of business to start.

- No special legal maneuvers are required.

- The profits or losses from the business become a part of the owner’s tax return/income.

- 2.) Partnership

- Business .

- Each partner is personally liable for the debts of their business.

- It is slightly more expense to create and needs a lawyer to come up with a partnership agreement.

- The profits or losses are split between the owners.

- 3.) Corporation

- Considered a separate legal entity and is formed by documents filed with a state.

- A lawyer is required and legal fees are high.

- The owners of the corporations, stockholders, are not personally liable for the debts.

- Income taxes are paid by the corporation and the owners (dividends).

- :

- Public company: Your stock is readily available for people to buy

- Private company: The stock is owned by individuals and privately conducts the process of buying and selling to others

- Corporations commonly start as a private company, but can “go public” if needed.

- Initial Public Offering (IPO) - “Going public”. This is the very first day that stock is traded on an established stock market.

Limited Liability Companies

- Limited Liability Companies (LLC) - A company that is a combination of a corporation and a sole proprietorship or a partnership.

- It can have characteristics from the three types of business, depending on the number of owners.

- You to become a LLC.

- Primary characteristics:

- Has limited liability like a corporation.

- Has access to pass through income taxation like a partnership or sole proprietorship.

- If there are two owners, it can be taxed as a partnership.

The Accounting System

- In accounting, you are analyzing, recording, and summarizing financial information and reporting the outcome of business activity.

- There are two types of reports that can be produced:

- 1.) Managerial Reports

- For internal users

- Reports on the operating activities of a business

- Includes financial plans

- 2.) Financial Statements

- For external users (those who are not employed at the company)

- Periodic statements

- There are four types of external users:

- 1.) creditors (ex: banks)

- 2.) investors (the stockholders)

- 3.) directors ( aka the board of directors)

- 4.) government (ex: IRS, SEC)

- Different types of business activities can be reported:

- Operating activities generate profit and involve short term expenses. These are the simple actions of running a business (buying supplies, paying employees).

- Investing activities involve the process of buying and selling assets that are considered long term (ex: equipment, land, buildings).

- Financing activities are more formal actions (not day to day) such as borrowing money from the bank, paying loans, receiving cash, or paying dividends.

Objective 1.2: Describe the purpose, structure, and content of the four basic financial statements.

The Basic Accounting Equation

| Resources Owned = | Resources Owed | Resources Owed |

|---|---|---|

| by the company | to creditors | to stockholders |

| ^^Assets^^ = | ==Liabilities== + | %%Stockholders’ Equity%% |

- The Basic Accounting Equation:

- Assets = Liabilities + Stockholders’ Equity

- Must always be balanced.

- Separate Entity Assumption- The financial reports of a business are assumed to include the results of only that business’s activities**.**

^^Assets^^

- Resources and will benefit from in the future.

- Examples:

- Cash

- Supplies

- Equipment

- Accounts Receivable

- Software

- Buildings

==Liabilities==

- Measurable amounts a company .

- If you see the word “payable”, it is a liability.

- Examples:

- Notes Payable - This is when you borrow money from a bank. Considered a formal agreement (legal document, aka promissory note, is required).

- Accounts Payable - Less formal agreement. You are paying for something “on account”, no legal document is required.

%%Stockholders’ Equity%%

- What .

- Stockholders is interchangeable with shareholders.

- An owner’s claims to the business can arise from 2 sources:

- Common Stock - This is equity PAID by stockholders to get stock.

- Retained Earnings - This is equity EARNED by the company. It represents cumulative profit or loss of the company.

Revenues, Expenses, and Net Income

- Revenues are the amounts we earn from selling goods or services:

- They are recorded when earned (after doing a sale or service).

- Expenses are considered to be day to day operations:

- They are the cost of what is needed to earn revenue, such as paying employees, paying bills, paying for space/land, etc.

- They are recorded when they are incurred (to become liable or subject to).

- Revenues - Expenses = Net Income

- If Revenues > Expenses, it is Net Income and increases equity (Good)

- If Revenues are < Expenses, it is Net Loss and decreases equity (Bad)

- Example of Net Income:

- $6,000 (R) - $2,000 (E) = $4,000 (N/I)

- Example of Net Loss:

- $2,000 (R) - $6,000 (E) = -$4,000 (N/L)

Dividends

- Dividends are considered a financing activity that involves using the profits of the company to “repay” (usually in cash) shareholders as a return on their investments towards the business.

- Dividends are a .

- They help reduce Retained Earnings.

- Dividends are not considered to be an expense.

Using the Basic Accounting Equation:

- Example: Use the following information to plug into the basic accounting equation:

- Assets = 168

- Liabilities = 75

- Stockholders’ Equity = 93

- 75 + 93 adds up to 168, so the equation is balanced.

- 168 = 168

| 168 (Assets) = | 75 (Liabilities) + | 93 (S/E) |

|---|

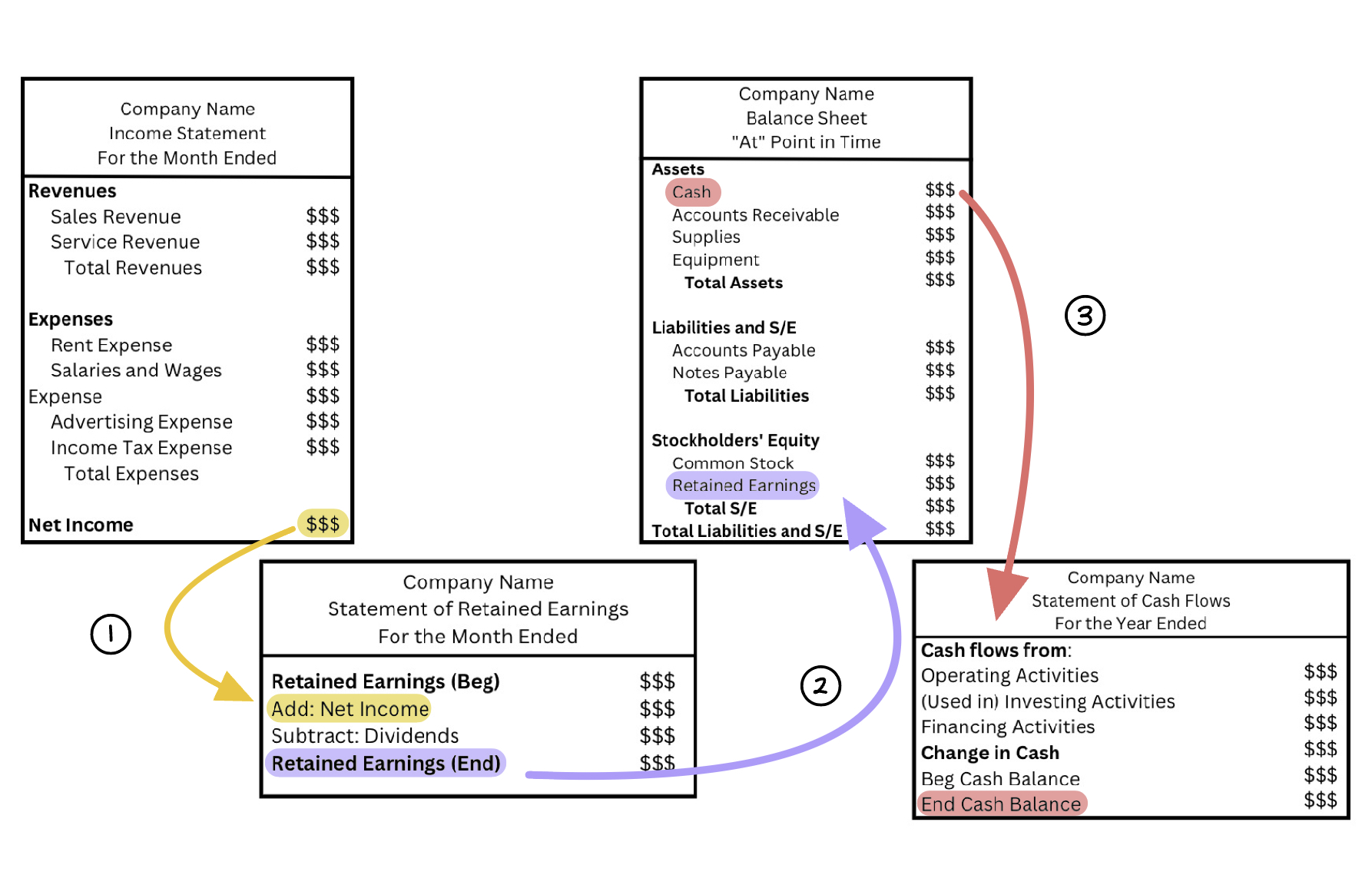

Financial Statements

- There are four types of financial statements and they are prepared in the following order:

- Income Statement

- Statements of Retained Earnings

- Balance Sheet

- Statement of Cash Flows

- They can be prepared monthly, quarterly, and annually.

- If they are annual reports, they can either be based on a calendar year or fiscal year:

- Both are reported in a 12 month period

- A calendar year ends on December 31

- A fiscal year ends on a day that is not December first (can be anytime during the year)

The Structure of Financial Statements

- Financial statements have headings that address who, what, and when.

- They include the name of the company, what type of report is being presented, and the accounting period for the report.

The Income Statement

- This report provides information regarding profitability for a specific period.

- :

- Heading (who, what, when)

- Company name

- Income Statement

- For the Month Ended

- Revenue

- Ex: Sales/Service Revenue

- Total Revenues

- Expense

- Ex: Rent Expense, Utilities Expense

- Total Expenses

- Net Income/Loss

- Expenses are listed from biggest to smallest.

- Income Tax Expense is always listed last.

- You want Revenues to be higher than Expenses to get Net Income.

- Unit of measurement assumption - the proper monetary unit must be used to report business activities (ex: United States = Dollar).

- The amount of Net Income/Loss with carry over into the next Financial Statements.

The Statement of Retained Earnings

- This report provides information regarding the company’s dividends and how their distribution affects the company’s financial position.

- Heading (who, what, when)

- Company name

- Statement of Retained Earnings

- For the Month Ended

- Retained Earnings (beginning)

- Add/Subtract: Net Income/Loss

- Subtract: Dividends

- Retained Earnings (ending)

- Retained Earnings (beginning) is the balance of the last period. If it is a new business, it will be $0.

The Balance Sheet

- In regards to source of financing, this sheet reports:

- Assets - What the business owns.

- Liabilities - Money borrowed and whats owed to creditors.

- Stockholders’ Equity - Money leftover to go to company’s shareholders.

- Balance sheets are considered to be a “snapshot” of a business’s resources on a specific date.

- Heading (who, what, when)

- Company name

- Balance Sheet

- “At” a specific date

- Assets

- Ex: Cash, Supplies, Equipment

- Total Assets

- Liabilities and Stockholders’ Equity

- Ex: Payables

- Total Liabilities (to creditors)

- Stockholders’ Equity

- Only 2: Common Stock and Retained Earnings

- Total Stockholder’s Equity (to stockholders)

- Total Liabilities and Stockholders’ Equity

- Assets must = liabilities + stockholders’ equity (it “balances”)

- Cost principle - Assets are recorded based on what we negotiated to pay for them.

The Statement of Cash Flows

- Reports the effects on cash balance based on operating, financing, and investing activities.

- Heading (who, what, when “For the Month Ended”)

- Company name

- Statement of Cash Flows

- For the Month Ended

- Cash Flows from Operating Activities

- Cash received from customers

- Cash paid to employees and suppliers

- Cash Provided by Operating Activities

- Cash Flows from Investing Activities

- Cash used to buy equipment and software

- Cash from Investing Activities

- Cash Flows from Financing Activities

- Cash received for stock issuance

- Cash dividends paid to stockholders

- Cash borrowed from the bank

- Cash Provided by Financing Activities

- Change in Cash

- Beginning Cash Balance (beginning of the month)

- Ending Cash Balance (end of the month)

- Cash from Statement of Cash Flows must be equal to the cash reported on the Balance Sheet

How These Statements Connect

- (1.) Net Income/Loss from the Income Statement carries over onto the Statement of Retained Earnings.

- (2.) On the Statement of Retained Earnings, the ending Retained Earnings moves to the “Stockholders’ Equity” section on the Balance Sheet.

- (3.) Cash amount reported under the “Assets” section of the Balance Sheet must be equal to the “Ending Cash Balance” on the Statement of Cash Flows.

Objective 1.3: Explain how financial statements are used by decision makers.

What Does Each Statement Do For Creditors and Stockholders?

- The Income Statement provides the stockholders with what the long term return is.

- The Statement of Retained Earnings shows the returns through dividends that are to be distributed to investors.

- The Balance Sheet allows creditors to see if the business’s assets will cover their liabilities.

- The Statement of Cash Flows shows if a business is making enough money to pay the amounts it owes.

Objective 1.4: Describe factors that contribute to useful financial information.

External Financial Reporting

- External users review and utilize the information of different financial statements.

- In order for decision makers to use these statements, it is important for the statements to be:

- Verifiable

- Timely

- Comparable

- Understandable

Accounting Standards

- FASB - Financial Accounting Standards Board (United States)

- GAAP - Generally Accepted Accounting Principles (United States)

- IASB - International Accounting Standards Board

- IFRS - International Financial Reporting Standard