APMACRO UNIT4

3/3: 4.3 -definition, measurement and functions of money

Why money?

What would happen if we didn't have money?

The Barter System: goods and services are traded directly. No money exchanged

Problems:

- Double Coincidence of Wants: each trader had to have something the other wanted

-ex. 1 goar us with 5 chickens, how do you exchange if you want 1 chicken.

-ex. A doctor accept certain goods so you need to find a doctor

What is money

Money is anything that is generally accepted in payment for goods and services

- money is NOT the same as wealth/income

Wealth: Total collection of assets

-Incole: flow of earnings per unit of time

Commodity Money: something that performs the function of money and has intrinsic value (ex. Wedding ring, gold)

Fiat Money: something that serves as money but has no other value or uses (ex. Paper money, coins, digital currency)

Functions of Money

A medium of exchange: money can easily be used to buy good and services with no complications of barter system

A Unit of Account: Money measures the value of all goods and services. Money acts as a measurement of value

Ex. 1 goat = $50 = $5 chickens or 1 chicken =$10

A store of Value: money allows you to store purchasing power for the future

Money supply- what makes money, money

Money is essentially an I.O.U. from the government “for all debts, public and private.”

Generally Accepted: buyers and sellers have confidence that it IS legal tender.

Scarce: Money must not be easily reproduced.

The Purchasing Power of money is the amount of goods and services an unit of money can buy.

-Inflation (+/-) purchasing power.

-Rapid Inflation (+/-) acceptability.

Classifying Money

Liquidity: ease with which an asset can be accessed and used as a medium of exchange

M1 (Highest Liquidity)

Currency in circulation

Checkable bank deposits (checking accounts)

Travelers checks

M2 (Near-Moneys) - M1 plus the following

Saving deposits (money market accounts)

Time deposits (CDs = certificates of deposit) saving accounts that give you interests.

Money market funds

M1 and M2 money often earn little to no interest so the opportunity cost of holding liquid money is the interest you could be earning.

6. Monetary base

Total amount of money that is in circulation and in the bank reserves

This includes money in your wallet right now and money that banks must keep in its reserves

Referred to as MO or MB

Money Supply: Total amount of money that is in circulation and in your personal checking account

3 / 4 : 4.2 - Real and Nominal Interest Rates

1.The Fiscal Sector

Individuals, Businesses, and Govs borrow and save so they need institutions to help

Financial Sector: Network of institutions that link borrowers and lenders including banks, mutuals funds, and other financial intermediaries

Assets: Anything tangible or intangible that is owned

Liability: Anything that is word

Loan: An agreement between a lender and borrow. Usually at a fee called the interest rate

A loan is an asset for the lender and a liability for the borrower

2. Interest Rates and Inflation

Interest Rates

“Cost” of money

If the nominal interest rate is 10% and the inflation rate is 15%, how much is the REAL interest rate?

Real Interest Rates

% increase in purchasing power that a borrower pays (adjusted for inflation)

Real = nominal interest rate - expected inflation

Nominal Interest Rates

% increase in money that the borrower pays not adjusting for inflation

Nominal = Real interest rate + expected inflation

3. Causes of Inflation

Demand-Pull Inflation

Demand pulls up prices!

“Too many dollars chasing few too goods”

An overheat economy with excessive spending but same amount of goods

Cost Push Inflation

High production cost increases prices

A negative supply shock increase the costs of production and forces producers to increase prices

4. Nominal v Real interest Rates

Getting paid back an amount with less purchasing power

5. How do changes in the interest rates affect bond price?

When you buy bonds, you can wait for them to mature or sell them early

Ex. bond at 5% IR will mature in 10yrs

If bond had a 10% IR, buyers would be less interested in bond so the price decreases.

Interest rates and bond prices are inversely related!

4.1 - Fiscal Assets

1. Liquidity

Cash: Actual cash on hand, it can be spent right away

Demand deposit: Zelle transfer

2. Other Financial Assets

Stocks and Bonds: Also Liquid-- you can transfer money to purchase stocks and bonds, can sell them to get your money back + interest. Bonds have an interest rate

3. Bond v Stocks

Bonds: loans, or IOUs, represent debt that gov, business, or individuals need to repay to lender

The bond holder has NO OWNERSHIP of company

To get money back, you could sell half of your company and issue shares of stocks

Stocks: Represent ownership of corporations and the stockholder is often entitled to a portion of the profits.

4. Bonds Prices and Interest Rates

A bond is Issued at a specific interest rate that doesn't change throughout the life of the bond

Bond price and interest rates are inversely related

5. Opportunity Cost of Cash

Putting Money under your mattress does not help you because it can't gain interest and can lose value, it loses value due to inflation and rising costs.

You can determine the future value of any amount ($X) if you now the interest rate (ir) and the number of years (N)

Equation: $X in N Years = $X (1 + ir)^N

Present Value: current worth of some future amount of money

Equation

Present Value of $X in 1 year = FV X 1 .

(1 + IR)n

3 / 5 : 4.4 - Banking and the expansion of the money supply

1. How can banks loan out money?

By using your money

The money you deposit gets loaned out to other borrowers

Does all the money get loaned out?

2. Bank Regulations

Deposit Insurance: A guarantee that depositors will be paid even if the bank can't come up with the funds back by FDIC. ($250,00)

Capital Requirements: Bank owners are required to hold more assets than the value of bank deposits.

Reserve Requirements: Required reverse ratio - 10%

Discount Window: Banks cannot be forced to sell off assets if there is a bank run, but can rather borrow money from the FDIC.

3. Fractional Reserve Banking

Banks can't loan out all your money

Banks hold only a small portion of your deposit to cover potential withdrawals and then loan out the rest of your money

Essentially, this is how banks can offer interest and to hold your money --> basically a contract you make with the bank

4. Bank Balance Sheets

Demand Deposit: money deposited in a commercial bank in a checking account

Required Reserves: The % that banks must hold by law (10%)

Excess Reserves: amount that the banks can load out (90%)

Balance Sheet: A record of bank assets, liabilities, and net worth.

Demand deposits in a bank is a liability for the bank and an asset to the depositor.

5. Money Multiplier

Equation:

1

Money Multiplier = -----------------------------

Reserve Requirement (Ratio)

3/6 : 4.5 - The Money Market

1. Demand For Money

Any time, people demand a certain amount of liquid assets (money) for two different reasons:

Transaction Demand for Money: people hold money for everyday transactions

Assets Demand for Money: People hold money since it is less risky than other assets

What is the opportunity cost of keeping money in your pocket or checking account?

The interest you could be earning from other financial assets like stocks, bonds, and real estate

What happens to the quantity demanded of money when interest rates increase?

Quantity demanded falls because individuals would prefer to have interest earning assets instead

What happens to the quantity demanded when interest rates decrease?

Quantity demanded increases. There is no incentive to convert cash into interest earning assets

There is an inverse relationship between the interest rates and the quantity of money demanded.

Inverse relationship between interest rates and the quantity of money demanded

----------------------------------------------------------------------

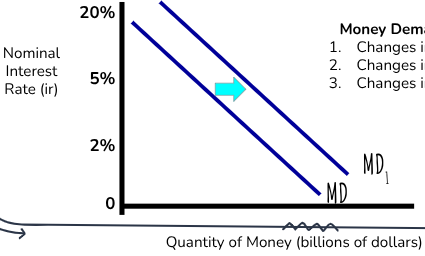

Money Demand Shifters:

Changes in price levels

Changes in income

Changes in technology

----------------------------------------------------------------------

2. The Supply For Money

The US Money Supply is set by the Board of Governors of the Federal Reserve System (FED)

Monetary Policy: The FED is a nonpartisan government office that sets and adjust the money supply to adjust the economy

Federal Reserve: Created in 1913, its job is to regulate banks and make sure people have faith in our financial system.

When is Equilibrium Achieved?

- When the nominal interest rate is such that the quantity demanded and supplied of money are equal

Shifters of the Money Supply: Interest on Reserves

------------------------------------------------------------------------

3. Increasing The Money Supply

If the FED increases the money supply, a temporary surplus of money will occur at 5% interest. The surplus will cause the interest rate to fall to 2%

(+) money supply ➡ (-) interest rate ➡ (+) investment ➡ (+) AD

------------------------------------------------------------------------

If the FED decreases the money supply, a temporary shortage of money will occur at 5% interest. The shortage will cause interest rate to rise to 10%

(-) money supply ➡ (+) interest rate ➡ (-) investment ➡ (-) AD

Fed is the only thing that controls the money supply

3/7 : 4.6 - Monetary Policy

1. Money Supply

The FED decreases the money supply to slow down the economy

Interest Rates increase

Investment Decreases

AD, GDP, and PL Decrease

Slow down the economy to fight inflation

How the FED stabilize the economy

2. 4 Shifters of the Money Supply

The FED adjusting the money supply by changing any one of the following:

Setting Reserve Requirements

Lending Money to banks and thrifts (Discount Rate)

Open Market Operations (Buying and selling Bonds)

Interest on Reserves

3. The Reserve Requirement (least used tool)

Fractional Reserve Banking: where only a small amount of your money is actually held and the rest is loaned out

The Fed sets the amount that banks must hold - 10%

The reserve requirement (reserve ratio) is the percent of deposits that banks must hold in reserve (% they can NOT loan out)

When the FED increases the money supply it increases the amount of money held in bank deposits

Banks keep some of the money in reserve and loans out their excess reserves

The loan eventually becomes deposits for another bank that will loan out their excess reserves

4. Using the reserve requirement

Recession = Decrease the reserve requirement

Banks hold less money and have more excess reserves

Banks create more money by loaning out excess

5. The Discount Rate

Discount Rate: the interest rate that the FED charges commercial banks

Ex.

Easy Money Policy: To increase the money supply, the FED should decrease the discount rate

Tight Money Policy: To decrease the money supply, the FED should increase the discount rate

6. Open Market Operations (most used tool)

Open Market Operations: the FED buys or sells gov bonds (securities)

Most important and widely used monetary tool

To increase the Money supply, the fed should buy gov securities

To decrease the money supply, the fed should sell gov securities

Buy- Big: buying bonds increase money supply

Sell- Small: selling bonds decrease money supply

7. Federal Funds Rate

The federal funds rate is the interest rate that banks charge one another for one-day loans of reserves

The FED cant simply tell banks what interest rate to use. Banks decide on their own

Fed influences them by setting a target rate and using open market operations to hit target

Federal funds rate fluctuates due to market conditions but it is heavily influenced by monetary policy (buying or selling of bonds)

8. Modern changes to banking

Interest on Reserves (IOR): The Interest rates that the federal reserves pay commercial banks to hold reserves

IOR and the discount rate are examples of administered rates

Administered Rates: Interest rate set by the FED rather than determined in a market

Reserved at the FED have no risk. Therefore, banks have no incentive to lend money at an interest rate that is lower than what they can get from the FED.

Stop banks from lending out all their money!

9. Limited Reserves v Ample Reserves

The tools used by central banks depend on if the banking systems has limited reserves or ample reserves

Limited Reserves:

Banks deposit few reserves with the central bank

Small changes in the money supply can affect interest rates

The central bank conducts monetary policy by changing the reserve requirement or the discount rate or by using open market operations

Ample Reserves:

Banks deposit a lot of reserves with the central bank

Changing the money supply has little or no effect on interest rates

The central bank conducts monetary policy by changing its administered rates (IOR or discount rate)

Overall Concept: The 3 tools of monetary policy are used when there are limited reserves. When there are ample reserves, the primary tool is interest on reserves. (IOR)

Limited Reserves

Reserve Ratios

Discount Rate

Open Market Operations

Ample Reserves

Interest on Reserves

4.7

1. Loanable Funds Market

Loanable funds market: is the private sector supple and demand of loans

This market shows the effect on REAL INTEREST RATE

Demand: Inverse relationship between real interest rate and quantity loans demanded

Supply: Direct relationship between real interest rate and quantity loans supplied

This is NOT the same as the money market (supply is not vertical)

2. Loanable Funds Market Graph

At the equilibrium real interest rate the amount borrowers want to borrow equals the amount lenders want to lend

Gov increase deficit spending

Gov borrows from private sector increasing the demand for loans

Real interest rates increase causing crowding out

3. Loanable Funds Market Shifters

Demand Shifters

Changes in perceived business opportunities

Changes in government borrowing

Budget deficit

Budget surplus

Supply Shifters

Changes in private saving behavior

Changes in public savings

Changes in foreign investment

Changes in expected profitability

4. Quantity Theory of Money

If the real GDP in a year is $400 billion but the amount of money in the economy is only $100 billion, how are we paying for things?

The velocity of money is the average times a dollar is spent and re-spent in a year

How much is the velocity of money in the above example?

Quantity Theory of Money Equation

- M x V = P x Y

- M- Money Supply P = price level V = Velocity Y+ Quantity of output

Notice that P x Y is Nominal GDP

Why does printing money lead to Inflation?

Assume the velocity is relatively constant because people's spending habits are not quick to change

Assume that output (Y) is not affected by the amount of money because it is based on production, not the value of the stuff produced

If the gov increases the amount of money (M) what will happen to prices (P)?

If the velocity and output stay the same, what will happen if the amount of money is increased to $10?

Doubling the money supply doubles prices. This is how increasing the money supply creates inflation