Economics : Ultimate Review Guide (Excluding Units 6,7,8,9)

Microeconomics

Unit 1 : Basic Economic Concepts

Scarcity

Economics is a study of how an entity manages an allocates it’s resources in the most efficient way possible.

The economic problem states that while our wants and needs are unlimited, the resources available to supply those needs and wants aren’t unlimited.

Scarcity: unlimited wants, limited resources

Factors of Production

Resources that are scarce

Land: natural resources & raw material

Labor: physical labor, skills, and effort devoted into a task where workers are paid

Capital: referred to as the liquid asset, or monetary value

Physical Capital: tools and equipment used to produce a good or service

Human Capital: education and training an individual that is used in the production of a good or service

Entrepreneurship: the ability of an individual to coordinate the other categories of resources to produce a good/service

Trade-Offs and Opportunity Costs

Trade-Offs: the alternative choice which must be given up in order to make a decision

Opportunity Costs: the next best choice that is traded off

Positive vs. Normative Economics

Positive Economics: this approach to economics is based off of facts and figures

Normative Economics: this approach to economics is based on assumptions

Resource Allocation

3 big economic questions, what, how, and for whom?

Economic Systems

Command Economic System

the government makes all the economic decisions and answers the three questions on its own. they set the price for goods and services, as well as set wage rates. however, they don’t respond to consumer wants, and innovation is discouraged

Market Economic System

economic changes are guided by the changes in price which occur as individuals and sellers interact in the market. a lot of competition and variety of goods and services; however, there will be a wealth disparity in the market

Mixed Economic System

a system which has characteristics of both command and market economic systems.

Production Possibilities Curve

represents the best possible combinations of goods, given a fixed amount of resources.

illustrates the trade-offs that face an economy, compares only 2 goods

if the PPC is linear, it has a constant opportunity cost. if it is curved, it has an increasing opportunity cost.

Economic growth: a sustained rise in aggregate output and an increase in standard of living

Productive efficiency: lowest cost possible on the PPC

Allocative efficiency: the economy allocates resources so consumers are as well off as possible, producing what is demanded

Cost Benefit Analysis

Implicit costs: monetary or non-monetary opportunity costs in terms of making a choice

Explicit costs: traditional out of pocket costs which are associated with choosing one course of action

Marginal Analysis and Consumer Choice

Utility: the measure of personal satisfaction (util is a unit of utility)

Marginal utility: the change in total utility by consuming one additional unit of that good/service

Principle of diminishing marginal utility: additional units of a good/service add less total utility than the previous units do

Marginal utility per dollar: marginal utility of one unit of the good divided by the price of one unit of the good

Unit 2 : Supply and Demand

Demand

Demand: the quantity at which a consumer/buyer are willing and able to buy at different prices

Movement on the graph: downward sloping (\)

Demand slopes down on the graph due to

income effect

substitution effect

law of diminishing marginal utility

Law of demand: as price increases, quantity demanded decreases, and as price decreases, quantity demanded increases

Determinants of demand: PRICE

Preferences and tastes

Related goods price

Income of consumer

Consumer amount

Expectation in future price

Substitutes: goods/services that can be used in place of another

Complements: goods/services that are consumed together

Normal good: increase in demand when consumer income increases

Inferior good: increase in demand when consumer income decreases

Supply

Supply: different quantities of goods/services which sellers are willing and able to produce at a given price

Movement on the graph: upward slope (/)

Law of supply: as price increases, quantity supplied also increases

Determinants of supply: SPENT

Subsidies and Taxes

Price of inputs/resources

Expectations of future price by producer

Number of producers

Technology and Productivity

Market Equilibrium, Consumer and Producer Surplus

Equilibrium: occurs when no one is better off doing something else

Consumer surplus: price consumers are willing to pay - actual price

Producer surplus: actual price - price the producer is willing to sell for

Demand increase: price and quantity increase

Demand decrease: price and quantity decrease

Supply increase: price decreases, quantity increases

Supply decrease: price increases, quantity decreases

Market Disequilibrium and Changes in Equilibrium

Market Disequilibrium:

Shortage: Qs < Qd, price is lower than equilibrium

Surplus: Qs > Qd, price is above equilibrium

Price floor: minimum price a supplier can charge, price is set above equilibrium (causes shortage)

Price ceiling: maximum price a supplier can charge, price is set below equilibrium (causes surplus)

Short-run Production Costs

Fixed cost: cost that doesn’t change with amt of output produced

Variable Cost: cost that changes with amount of output produced

Total Cost: fixed cost + variable cost

Marginal Cost: cost difference of one additional unit of output (∆TC/∆Q)

Average fixed cost: FC/Q

Average variable cost: VC/Q

Average total cost: TC/Q

Long-run production Costs

Long run average total cost: same as short run ATC, but bigger

Economies of Scale: LRATC declines as output increases

Diseconomies of Scale: LRATC increases as output increases

Constant returns to scale: output increase directly in proportion to an increase in all inputs

Types of Profit

Economic Profit: revenue - explicit cost - implicit cost

Accounting Profit: revenue - explicit cost

Implicit Cost: not an actual cost, a cost that you could’ve been earning

Marginal Revenue: additional revenue gained by producing one more unit

Profit Maximization

Marginal revenue = marginal cost

Entering and Exiting Markets

Short Run:

Shutdown rule: as long as P > AVC, continue to produce

If AVC > P, shutdown

Firms can make profit or losses

Long run:

Exit rule: if P < ATC, exit the market

Firms make normal profit ($0), unless monopoly/oligopoly

Shut down rule: a firm should not produce unless it can cover its variable costs.

Types of Markets

Perfect Competition | Monopolistic Competition | Monopoly | Oligopoly | |

# of firms | many | many | 1 | few |

type of product | standard | differentiated | unique | standard or differentiated |

price control | none | little | yes | interdependent |

barriers to entry | none | none (few) | high | high |

Externalities

Externality: when external costs/benefits is placed on members of society who did not pay for them

Negative Externality: when someone uses a product, it decreases the benefit of others (smoking)

Positive Externality: when one uses a product, others benefit

Taxes

Proportional: everyone pays the same percentage of their income

Progressive: taxes are higher on people earning a higher income

Regressive: taxes are lower on people earning a higher income

Macroeconomics

Comparative Advantage and Trade

Absolute Advantage

the absolute advantage is producing goods/services more efficiently, using fewer inputs

Comparative Advantage

the comparative advantage in something is the product that a company/nation can produce at a lower opportunity cost than the other

Countries export what they have a comparative advantage in and import what they don’t have a comparative advantage in.

To determine absolute advantage, you are looking for the country that uses the least number of resources (i.e., the lower number)

To determine comparative advantage, you have to calculate the per unit opportunity cost using the formula gain/give up. Once you have calculated the per unit opportunity cost, the country with the lowest one has a comparative advantage.

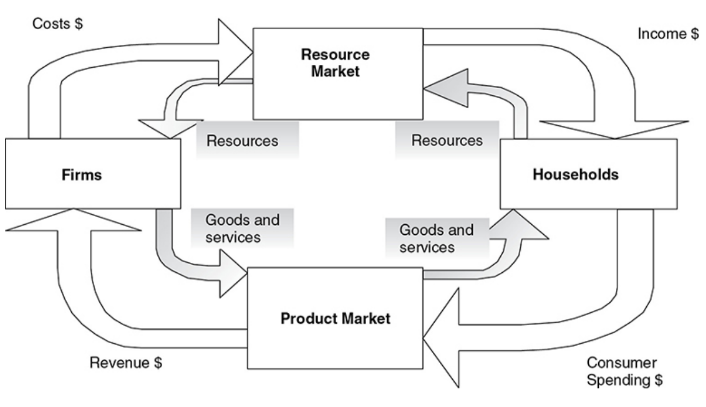

Circular Flow

Unemployed

Discouraged Workers: citizens who have been without work for so long that they become tired of looking for work and drop out of the labor force. These citizens are not counted as unemployed.

Types of Unemployment

Frictional: occurs when someone new enters the labor market or switches jobs.

Structural: the result of fundamental, underlying changes in the economy such that some job skills are no longer in demand

Cyclical: rises and falls within the business cycle.

This is all I’m going to make as I already have Units 6, 7, 8, and 9 in other knowts (i moved them to this folder)