ECON TEST 1

Econ - social science where due to finite amount of resources optimal choices are being made using the scientific method

Optimal choice based in scarcity

Consensus is bad

Micro vs Macro

Micro: Decisions made by individuals, firms, or governing bodies

Macro: Aggregates--totalling--and their limitations; HOW do the groups handle the issues as a whole

Classical vs Keynesians + other influences

Organizations must make decisions on allocating limited resources

“TINSTAAFL”

“There is no such thing as a free lunch”

Theories, Principles, and Models

Model - an attempt to form a graphical (mathematical) representation of a complex situation to predict something

Model human behavior

Some become theories and others law

What’s the difference?

Law can be proven over and over again

Theories are not yet proven to be laws

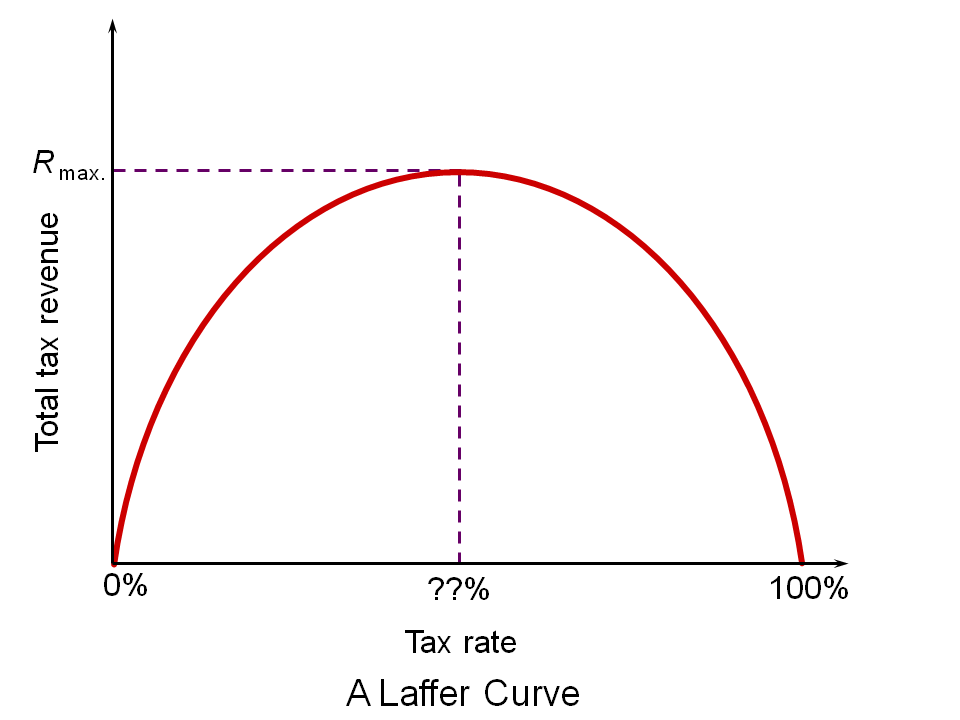

Laffer Curve

Can be used to demonstrate optimal tax rates to benefit the gov’t

Taxing more can be detrimental to revenue as it reduces the economy

Not a curve but still useful

Assumptions must be made for initial descriptions

Leads to peer review

Makes models less realistic

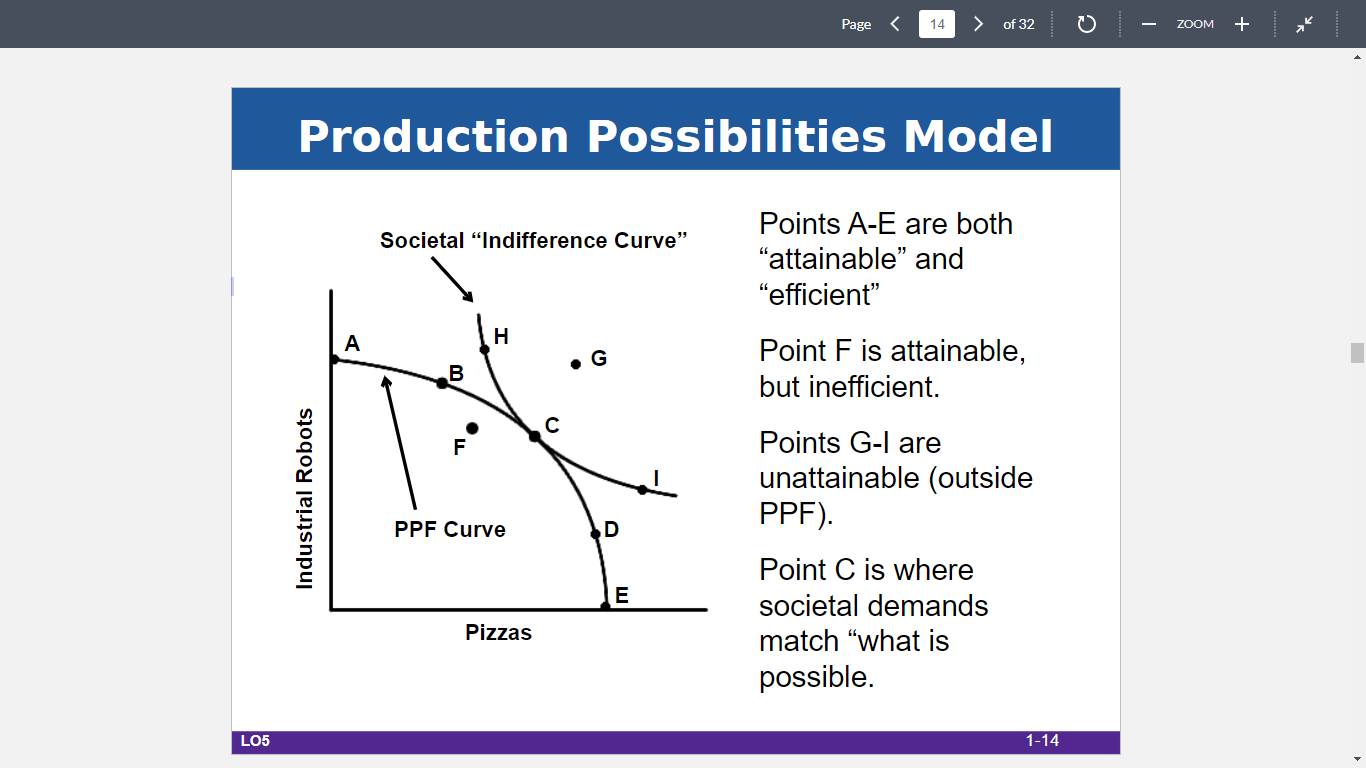

PPC/PPF illustrate production choices

Production-possibility frontier/curve

What can be produced is in the curve

Beyond the frontier (curve) is not possible unless expansion occurs

Economic Growth - makes the unattainable attainable

Increased efficiency

Better technology

Higher birth rates

Can also be shrunk (economic decay)

“Dark ages”

Theft, murder, etc

Loss of human knowledge

How much should we produce?

Does what we want as a society change over time?

Influenced by culture

game stop - loss of physical games

Assumes we are using all our resources

Closer to the curve = more efficient and things on the curve are equal

Further evaluated with judgment calls (i.e. resource 1 is better than resource 2)

Makes assumptions and explains production choices

Full employed resources

Fixed resources (quantity and quality)

Fixed tech

Two goods

Fixed time period

Advantages for deciding which efficient point to choose

Absolute Advantage - can produce more units of a good/service with fewer resources (better)

Gaston (from Beauty and the Beast) is better at everything, but shouldn’t necessarily do everything (constrained by time)

Comparative Advantage - can produce a good at a lower cost (cheaper)

China/Taiwan > US production due to cost

Increase in supply typically makes a decrease in wages

Substitution Effect - decrease in sales for a product as people go towards a cheaper alternative

Specialization of Trade

Gaston is the best at “everything,” but he should do whichever one he’s better at/more productive at

Everything else is left to comparative advantage

Division of Labor

Societal “Indifference Curve”

Represents a series of things that consumers would be indifferent to

Used in tangent with the PPF to determine which choice is the best

Alone, all points are equal/up to the consumer when on the line

Compares max usage of resources to society’s wants to find the best and actually attainable point along the PPF

Praxeology - study of human action, based on notion that humans engage in purposeful behavior (humans do things for a reason) with two main assumptions:

Individuals act rationally and self-interestedly in order to maximize their “utility”

Measured with utils--unit of measurement economists use to gauge satisfaction

Ceteris paribus - all else is held constant; all are equal

If you say this then you can “never” be wrong

Used to isolate one variable to study why it happens/changes

Redefined to ^^ by French social philosopher Alfred Espinas, developed by multiple schools

Holds flaws and disagreements due to the differences between sociologists and economists in understanding human behavior (economists generally require rationally-acting subjects)

Austrian School of thought - created by Ludwig von Mises

Irrational Action can be explained

Asymmetrical information - imbalance of information

Adverse selection

Group has little info and will enter markets they should avoid (make less than optimal decisions)

Uninformed/no guidance

2008 housing crash

Moral hazard

Believes that they are shielded from risk, so they engage in risky behavior

Football players - started to have more fatal injuries AFTER starting to wear protective helmets/pads

Utility - overall level of satisfaction (measured in utils)

Not always monetary profit, but is often substituted

Time Preference/MANY NAMES

Current valuation placed on receiving a good at an earlier/later date

Not necessarily good or bad

High Time Preference

Instant gratification

Child w candy bar

Will eat the candy bar at the present instead of waiting for another one

Low Time Preference

Adult w candy bar

Delayed gratification

Pitfalls to Sound Economic Reasoning

Biases

Logical Fallacies - breakdown in overall logic/reasoning

Fallacy of composition

What’s true for the part is true for the whole

Post hoc fallacy

High time preference pedo !

Post hoc, ergo, propter hoc (after this, therefore, because of this)

Something happened, thus it must be the cause

Broken Window Fallacy

NEW SUIT-AH 🥐🕺

Physical destruction of property destroys wealth

Requires stimulation of the economy to bring it back

Government spending has 3 sources:

Tax, borrowed, or printed

CORRELATION IS NOT CAUSATION 🗣

Leads to differing statements

Positive economic statements

Based on factual easy checked facts

Normative statements

Has value/judgment/opinions attached to them

Fact: soobin is the best Opinion: soobin is not the best

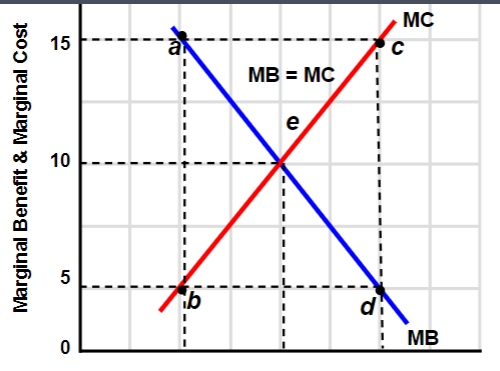

Marginal Analysis

Marginal = extra/additional

Marginal Benefit, MB

Satisfaction from a product or service

Marginal Cost, MC

The cost of the product/service

Marginal Utility = change in utility

With each increase in quantity, the benefit will be smaller and smaller until the cost overpowers it

Marginal cost increases; marginal benefit decreases as quantity increases

When the two lines meet, this is the optimal allocation; MB=MC

Individual’s Economizing Problem

Limited Income - linear model

Unlimited Wants

Budget line

Attainable and unattainable options

Tradeoffs and opportunity costs

Make the best choice possible

Change in income

Society’s Economizing Problem

Land

Fixed

Building up for more land

Labor

Capital (Physical/Human)

Human - ability to understand/overall skills current economic conditions

Entrepreneurial Ability

Finite amount of entrepreneurial ability

Innate or social 🤷

Time

Ch3 Market Systems

Market - where ppl come together for goods and services

Economic system

Coordinating mechanism of institutional/gov’t arrangements

Free Markets vs Socialism/Communism

Gov’t vs. Private Ownership

Central Planning vs. Market Signs

Central planning - designs of how things are meant to work

Pushed back by human’s desire to do what serves them

Some central planners work with users for optimal results

Presented in graphs with the opposing points^

Both ends of the spectrums will typically agree with each other but from different perspectives

US is in a mixed market of free and controlled

Adam Smith - Wealth of Nation (1776)

Written to investigate why some nations get ahead of others

Collection of observations

Viewing that countries that support certain ideas will get ahead

Private/Intellectual Property

Freedom of enterprise and choice

Self-interest

Competition

Markets and prices

The “Invisible Hand” vs. The “Iron Fist”

The people, processes, and drive that leads people to create things through cooperation

Firms exist in to solve the inefficiencies of free markets

Marxian comparatively saw growth through emotional motivators (potentially envy)

This MIGHT be envi

Bogourgieses - rich bitches 🔪

Goods and services that create a profit will be produced

Consumer Sovereignty (Dollar Votes)

How consumers determine which goods will be produced and what products/industries survive

Rights vs. entitlements

John Locke -

Positive rights: gov’t guarantees something

Housing, vacation time in employment

Negative rights: gov’t cannot take it away from you

Life, liberty, and property

Markets

Demand Function/curve

Schedule or curve

Amount consumers are willing and able to purchase at a given price

Is a negative curve as consumers want more products for less money

The first instance of the product has the most utility, from then on there is less and therefore “should cost less”

Other things equal (Ceteris Paribus)

Individual Demand vs. Market Demand

As you earn more money something

Ch4 Supply and Demand Model

Law of Demand

Other things equal, as price falls, the quantity demanded rises, and as price rises, the quantity demanded falls.

Ceteris paribus

Reasons:

Common sense

Law of diminishing marginal utility

Point where you don’t want to consume anymore

Income effect and substitution effects

Demand:

What someone is willing and able to pay for something

“Change In” and “Change In Quantity”

Change in (demand/supply)

ONE of the curves shifts to the left of the right along the quantity axis -- only one of the curves moves

A shift is caused by determinants

DEMAND DETERMINANTS

Change in consumer tastes and preferences

Tuna is more expensive now because people like sushi

Change in number of buyers

Change in income

Normal goods

When income goes up, demand goes up

Steak (you will buy more steak if you have more money)

Inferior goods

If income goes up, you won’t buy more

Kraft Mac and Cheese (you won’t buy anymore if you have more money)

Change in prices of related goods

Complements

Something you purchase together

NOT inputs (like eggs going into cake)

Substitutes

Change in consumers’ expectations

If there is a hurricane, people will stock up on water in expectation

Future prices

Future income

SUPPLY DETERMINANTS

Change in resource prices

Change in technology

Change in the number of sellers

More - right

Less - left

Change in taxes and subsidies

Change in producer expectations

Needing time to produce products that will be needed in the future

Change in quantity

When the “change in” curve moves, the quantity changes (horizontal axis)

Markets:

Bids lower than asking price

Only after a trade there is equilibrium

Price is only a determining factor if its in ANOTHER market--it is a product in any other situation

One change in quantity and one for demand/supply

Change in (increase of) demand -> increase of quantity/equilibrium

Market Equilibrium

Where a consummate trade is equal for supply and demand

Supply-side Failures:

When a firm does not pay the fullcost of producing its output

External costs of production is not reflected in supply

Private Goods

Produced in the market by private firms

Offered for sale

Characteristics (private goods do not struggle with)

Rivalry

2 individuals/firms can not consume the same good

Excludability

Individuals/firms that don’t pay can be excluded from consuming

Public Goods

Provided by government

Offered for “FREE” (TINSTAAFL)

Externalities

What is economics / the economizing problem?

The “economizing problem” is that individuals, firms, and governments have unlimited wants

but are bound by scarce resources. Economics is a social science concerned with making optimal choices under conditions of scarcity.

Opportunity Cost

the loss of potential gain from other alternatives when one alternative is chosen. HW question 4.Models / Theories / Laws & Assumptions (purposeful behavior, ceteris paribus, and various models)

ceteris paribus - all else is the sameModels - economists do it with models

Simpler models are often less realistic

Praxeology

Humans act rationally and logicallyCost / Benefit Analysis

Marginal Analysis

Asymmetric Information + Moral Hazard / Adverse Selection

Adverse selection - not enough info (people who entered the stock market w/o sufficient knowledge)Moral hazard - continues to do risky behavior when there are no consequences

Logical Fallacies (Post Hoc, Composition, etc)

Post hoc - fallacy in which an event is presumed to have been caused by a closely preceding event merely on the grounds of temporal successionThe fallacy of composition arises when an individual assumes something is true of the whole just because it is true of some part of the whole.

Correlation vs. Causation

Correlation is NOT causationPPF Curve + Assumptions. Basic understanding. What does it represent? Why does it bow from the origin?

Bows at origins because it takes more resources to switch to a new productRepresents the possible combinations of two product

Centrally Planned Economies (Command and Control) vs. Free Market (Invisible Hand / Adam Smith) Economic Systems

Self Interest. Dollar Votes. Consumer Sovereignty.

*** SUPPLY AND DEMAND *** (KNOW THE DETERMINANTS OF EACH!!!)

"Change In" vs. "Change in Qty", Increase / Decrease along Q (x axis)

Consumer vs Producer Surplus

Ceteris Paribus

Price Ceilings vs. Price Floors (Shortages / Surpluses)

Dead Weight Loss

Market Failures

Resources can be over-allocated/under-allocated and positive/negative externalities can affect it.

Demand-Side Failures: free rider problem + can’t charge consumers what they are willing to pay for the product

Supply-Side Failures: a firm doesn’t pay for full cost of producing output; costs of producing supply is not shown in supplyRivalry / Excludability / Free Rider Problem / Public vs Private Goods

Rivalry

2 individuals/firms can’t consume the same good

Excludability

firms/companies who do not pay are excluding from using

Free Rider Problem

People who enjoy benefits without paying or compensating.

Public vs Private Goods

Public Goods: goods that are non-excludable and non-rivalrous

Private Goods: goods that are excludable and rivalrous

Time Preference

High Time Preference: Instant gratification; spending immediately; Keynesians

Low Time Preference: Delayed gratification; savings/future plansLaffer Curve (basic understanding

Used to understand optimal rates (at the peak) for things like taxes