Chapter 3: Demand, Supply, and Market Equilibrium

- Markets - Bring together buyers + sellers

- Highly competitive markets have large #s of independently acting buyers + sellers of standardized products

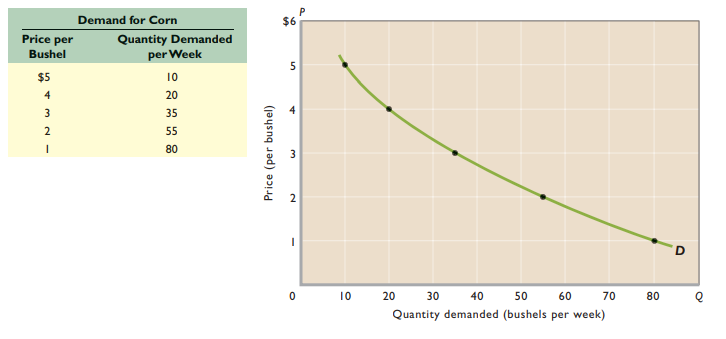

- Demand - Schedule/curve showing various amounts of product that consumers willing + able to buy at several possible prices during a specific period of time

- Statement of buyer’s plans/intentions of purchase of product

- Demand schedule - Illustrates quantity demanded of a good or service at different prices

- Law of demand - Other things equal, as price falls, the quantity demanded rises (and vice versa)

- Inverse relationship

- Diminishing marginal utility - Each successive unit of product consumed → Buyers get less satisfaction

- Income effect - Lower price increases purchasing power of income → Buyer can purchase more of product than before (and vice versa)

- Substitution effect - Buyer has incentive to substitute less expensive products for similar products that are relatively more expensive

- Demand curve - Quantity demanded on horizontal axis, price on vertical axis; downward slope reflects law of demand

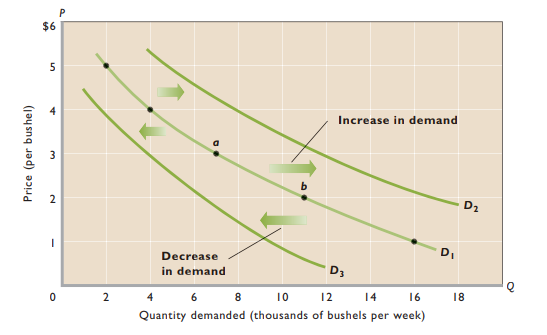

- Increase in demand → Curve shifts right

- Decrease in demand → Curve shifts left

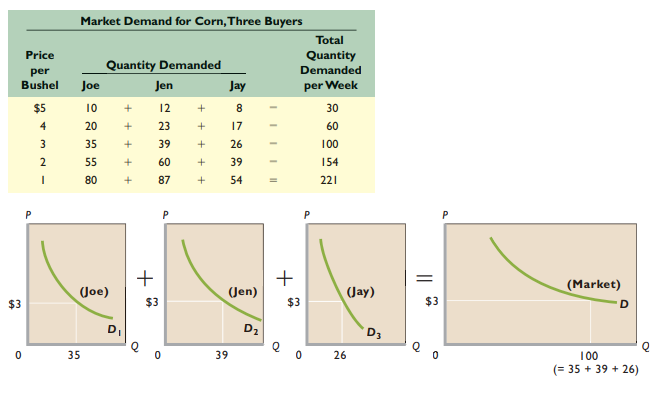

- Add quantities demanded by all consumers at each possible price → Market demand

- Determinants of demand - Other factors besides price that affect purchases; shifts the demand curve

- Consumer preferences

- Number of buyers

- Consumer incomes

- Normal goods - Rise in income causes increase in demand

- Inferior goods - Rise in income causes decrease in demand

- Prices of related goods

- Substitute goods - Increase in price of one related good → Demand for other good increases

- Complementary goods - Increase in price of one related good → Demand for other good decreases

- Independent/unrelated goods

- Consumer expectations

- Change in demand - Shift of demand curve to right/left

- Change in quantity demanded - Movement from one point to another on a fixed demand curve (the same demand curve)

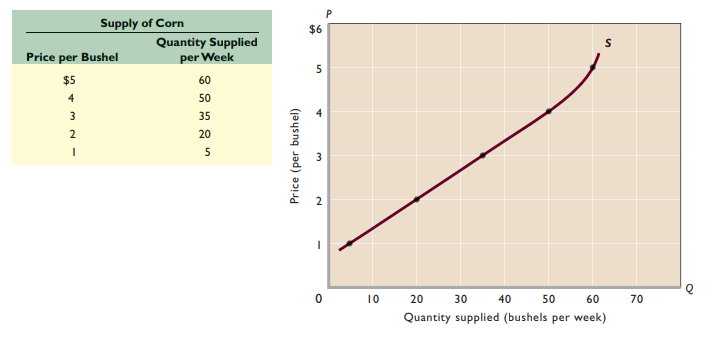

- Supply - Schedule/curve showing various amounts of product that producers are willing + able to make available for sale at several possible prices during a specific period of time

- Supply schedule - Illustrates quantity supplied of a good or service at different prices

- Law of supply - Other things equal, as price rises, the quantity supplied rises (and vice versa)

- Supply curve - Upward sloping; reflects law of supply

- Sum quantities supplied by each producer at each price → Market supply

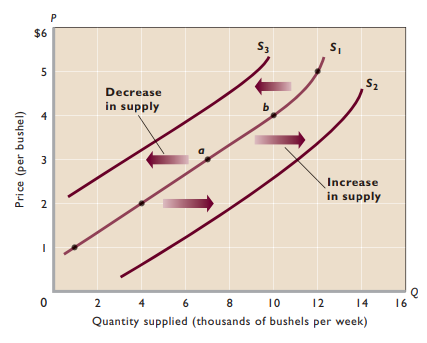

- Determinants of supply - Other factors besides price that affect supply; shifts supply curve

- Resource prices

- Technology

- Taxes and subsidies

- Prices of other goods

- Producer expectations

- Number of sellers in the market

- Change in supply - Shift of supply curve to right/left

- Change in quantity supplied - Movement from one point to another on a fixed supply curve (the same supply curve)

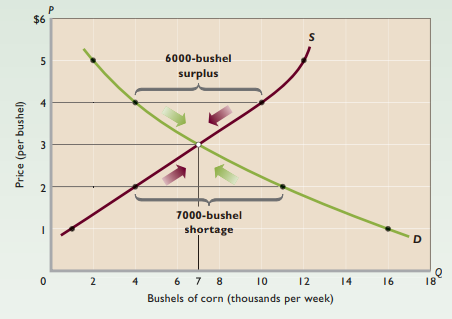

- Equilibrium price - Price where quantity demanded = quantity supplied

- Intersection of supply + demand curve

- Equilibrium quantity - Quantity demanded and quantity supplied at the equilibrium price

- Surplus - Quantity supplied exceeds quantity demanded; drives prices down

- Shortage - Quantity demanded exceeds quantity supplied; drives prices up

- Rationing function of prices - Competitive forces of supply + demand establish equilibrium price

- Productive efficiency - Production of a good in the least-costly way

- Allocative efficiency - Production of the particular mix of goods and services most highly valued by society

- Demand reflects marginal benefit, supply reflects marginal supply

- MB = MC → Allocative efficiency

- Changes in supply + demand

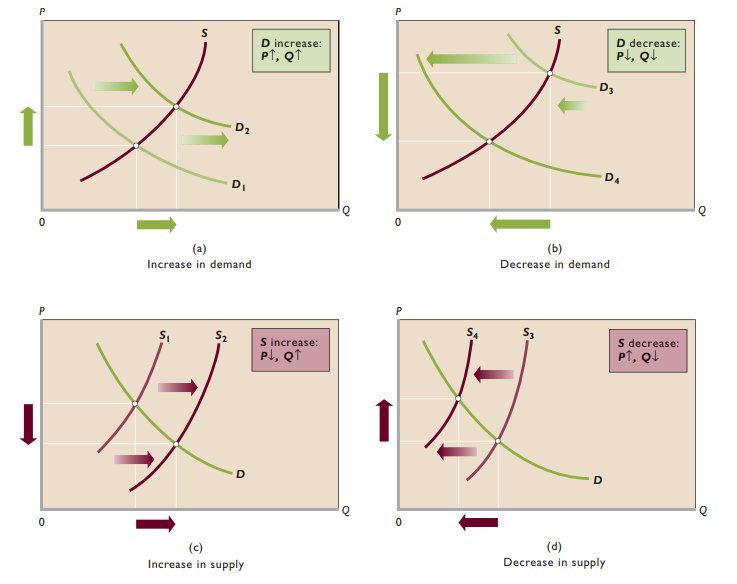

- Increase in demand → Increase in equilibrium price + equilibrium quantity

- Increase in supply → Decrease in equilibrium price + increase in equilibrium quantity

- Supply increase, demand decrease → Equilibrium price decrease, equilibrium quantity indeterminate

- Supply decrease, demand increase → Equilibrium price increase, equilibrium quantity indeterminate

- Supply increase, demand increase → Equilibrium price indeterminate, equilibrium quantity increase

- Supply decrease, demand decrease → Equilibrium price indeterminate, equilibrium quantity decrease

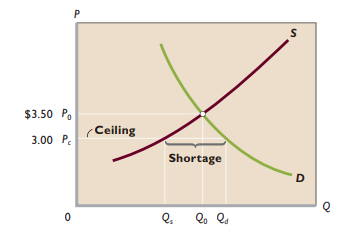

- Price ceiling - Maximum legal price a seller can charge for a good or service

- Must be below equilibrium price to be binding

- Shortage

- Rationing problem - Gov’t must establish formal system of rationing in order to solve inequitable distribution of gasoline

- Black markets - Goods illegally bought and sold at prices above the legal limits

- Rent controls - Maximum rents established by law

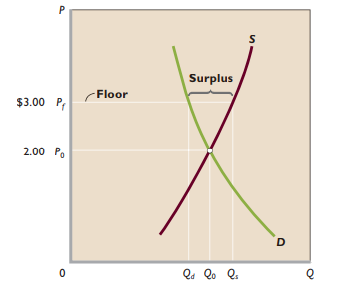

- Price floor - Minimum legal price a seller can charge for a good or service

- Must be above equilibrium price to be binding

- Surplus

- Gov’t can solve surplus by either restricting supply or purchasing surplus output

- Distorts resource allocation