2d. Production

Total, average and marginal product

Total product is the quantity of outputs produced by a given number of inputs over a period of time

Average product is the quantity of output per unit of input (the total product divided by the quantity of inputs)

Marginal product is the addition to outputs produced by an extra unit of input

Average product (AP) = Total product/variable input

Marginal product (MP) = Change in TP/Change in variable input

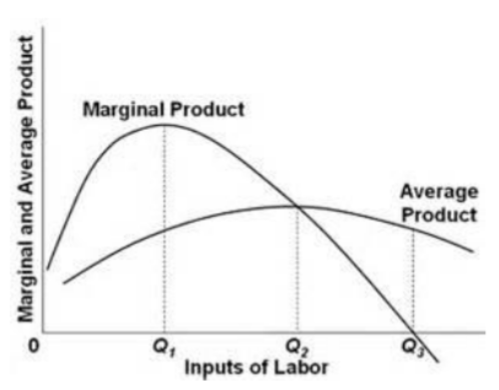

Marginal diminishing returns

This is a short-run concept that occurs because one factor of production is fixed.

Initially, output per worker is likely to rise. But at the point where it begins to fall, we find the ‘optimum’ level of production.

For example ‘too many cooks spoil the broth

At Q1 there is a marginal diminishing return

At Q3 it is negative

At Q3 Total Product is at its

Long run returns to scale

In the long run, firms can vary all of their factors of production:

Increasing returns to scale occurs if an equal percentage increase in inputs to production leads to a more than a proportional increase in output

Constant returns to scale occur when the same output occurs as the input

Decreasing returns to scale occurs when a percentage increase in input actually leads to a lower output