Ch 15 - Aggregate Supply

Aggregate supply: total amount of goods and services that all industries in the economy will produce at a given price level

- Positive slope: AS has a positive slope because the price level and AS have a direct relationship. The price level increases real AS increases.

- Movement along the supply curve: an increase in price will cause an increase in the price level which leads to an increase in output in the short run, as an increase in prices will make it more profitable to produce.

- Short run aggregate supply curve: when factors of production change.

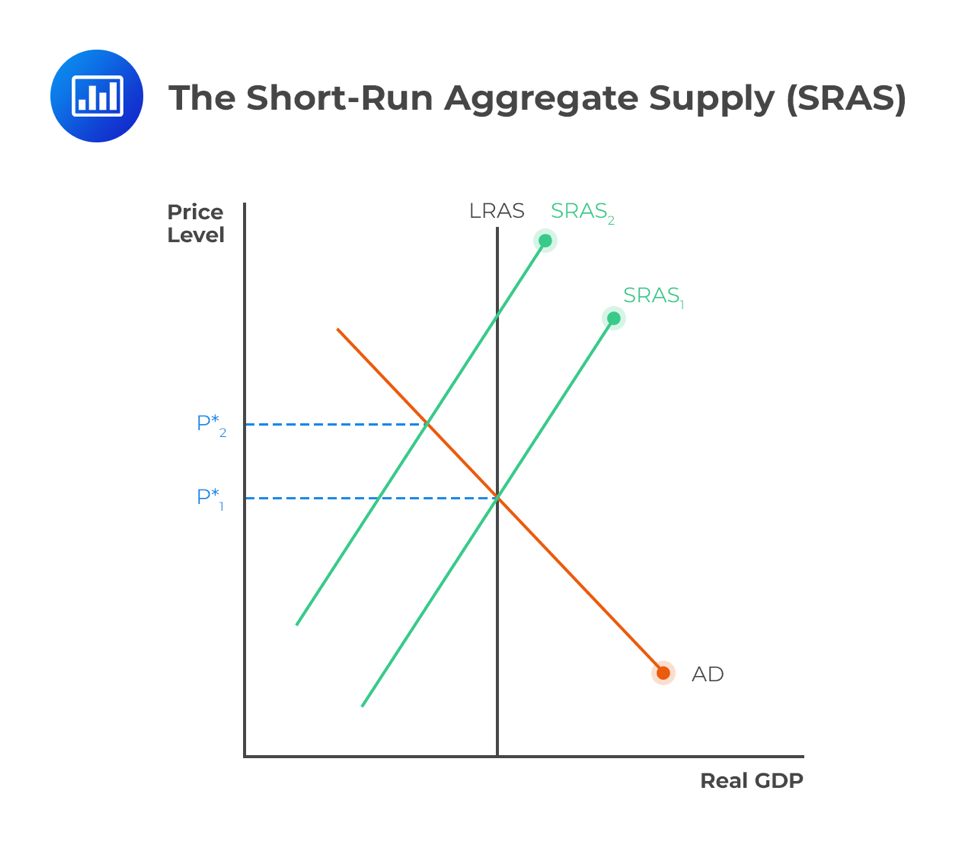

Short run aggregate supply: SRAS

SRAS curve is upward sloping, higher the level of prices, more products will prepare to produce

- Higher outputs → higher marginal costs

Factors that cause a shift to the SRAS curve are known as supply shocks

- Supply shocks can only be shifted by:

- Rent wages

- Cost of raw material

- Price of imports

- Government policy

Long Run Aggregate Supply LRAS:

New classical view (free market view):

- Its position depends upon the quantity and productivity (quantity) of factors of production. National outputs may only be increased by adopting supply-side policies to shift the LRAS to the right

The Keynesian View: there are three phases:

- LRAS is perfectly elastic. Producers in the economy can raise their own level of output without higher average costs

- The economy approaches its potential output, the spare capacity is used up, available factors in the economy become scarce. As producers increase output, they bid for the increasingly scarce factors and prices begin to rise

- When the economy is at full capacity, all factors are being used and so output cannot increase. LRAS is perfectly inelastic

- Spare capacity: the resources (land, labour, capital and enterprise) are not fully employed. It is possible to increase output without expecting an increase in costs and price level will remain constant.

- Approaching full employment: as the economy approaches full employment shortages start to occur in the economy they have the effect of bringing up the price/cost of the resources.

- Full employment: all resources are being used fully and it is not possible to increase output. Any attempt to increase output will simply result in higher prices.

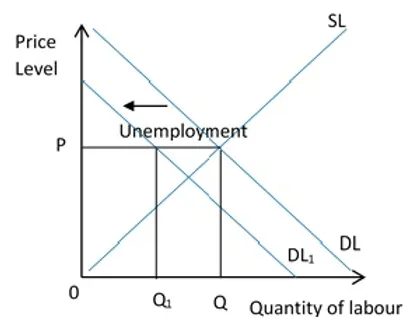

- The Keynesian economists believe that unemployment can exist in the long-run in an economy as the labour market does not always reach equilibrium resulting in unemployment.