Aggregate Demand and Aggregate Supply

Short-Run Economic Fluctuations

Economic activity varies from year to year.

In the short run, GDP oscillates around its trend.

Most years see an increase in the production of goods and services.

Recessions occur when normal growth is disrupted.

Recession: A period marked by declining real incomes and increasing unemployment.

Depression: A severe and rare form of recession.

Short-run economic fluctuations are often referred to as business cycles, representing the natural rise and fall of economic growth over time.

Three Facts About Economic Fluctuations

FACT 1: Economic fluctuations are irregular and unpredictable

FACT 2: Most macroeconomic variables fluctuate together, however they fluctuate by different amounts

FACT 3: As output rises, unemployment falls

Explaining Short Run Economic Fluctuation

The theory of economic fluctuations is complex and contentious.

Most economists utilize the aggregate demand and aggregate supply model to analyze these fluctuations.

This model contrasts with classical economic theories used for long-run analysis.

The Basic Model of Economic Fluctuations

Two variables used to develop a model

The economy’s output of g&s measured by real GDP

The overall price level measured by CPI/GDP deflator

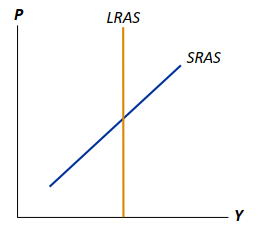

=> The model of AS - AD

The economy’s output of goods and services, measured by Y.

The overall price level, measured by P.

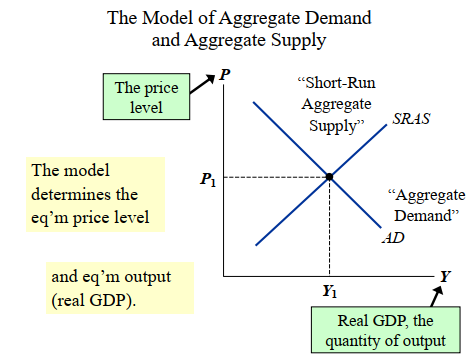

Model of Aggregate Demand and Aggregate Supply:

The model determines the equilibrium price level and equilibrium output (real GDP - many kinds of output).

AD represents "Aggregate Demand."

SRAS represents "Short-Run Aggregate Supply."

Reminder: SRAS is short-run because in the long run, supply curve is vertical

Long-run output (Y) does not depend on price PPF

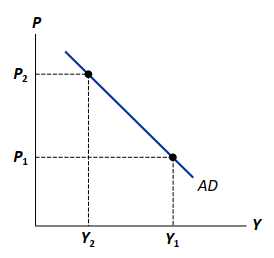

The Aggregate-Demand (AD) Curve

The AD curve illustrates the quantity of all goods and services demanded in the economy at any given price level.

Why the AD Curve Slopes Downward

The four components of GDP (Y) contribute to the aggregate demand for goods and services.

This equals to GDP, but different from GDP

GDP is actual expenditure, while AD is planned expenditure, but based on current price level and demand

Assume G is fixed by government policy (exogenous).

To understand the slope of AD, we must determine how a change in P affects C, I, and NX.

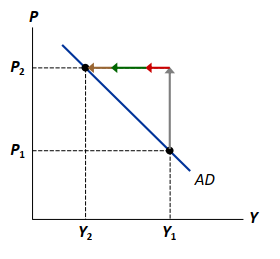

The Wealth Effect (P and C)

Mechanism:

P falls → real value of money falls → C falls → AD falls

P rises → real value of money rises → C rises → AD rises

A lower price level increases the real value of money holdings (cash, bank accounts). Consumers feel wealthier and spend more on goods and services.

Example:

If P falls by 20%, the same amount of money buys 20% more goods. Households increase consumption (C).Effect on AD:

Lower P → Higher real wealth → Higher C → Increased quantity of output demanded (Y).

The Interest-Rate Effect (P and I)

Mechanism:

P rises → demand for money rises (more money is needed for transactions now that things become more expensive) → deposit less money in banks → higher interest rates → discouraged borrowing for investment

A lower price level reduces the demand for money (since less money is needed for transactions). People lend excess money (e.g., buy bonds), lowering interest rates (r). Lower r encourages borrowing for investment (I) and big-ticket consumer purchases.

Example:

If P falls, households deposit more money in banks → banks lower interest rates → firms borrow more to build factories.Effect on AD:

Lower P → Lower r → Higher I and C → Increased Y.

The Exchange-Rate Effect (P and NX)

Mechanism:

P rises → demand for money rises → people lend less, sell bonds and hold more money → higher interest rates

Higher domestic interest rates attract investors → Foreigners buy domestic assets (US bonds) → increasing demand for domestic currency → domestic currency appreciates

A stronger currency makes exports more expensive for foreigners and imports cheaper for domestic buyers → X falls, M rises → NX falls

A lower price level reduces interest rates (r), making domestic assets less attractive. Investors sell domestic currency to buy foreign assets → domestic currency depreciates. Cheaper domestic goods boost exports (XX), while foreign goods become more expensive, reducing imports (MM). Net exports (NX=X−M) rise.

Example:

Lower P in the U.S. → Lower U.S. interest rates → Dollar depreciates vs. euro → U.S. goods cheaper for Europeans → U.S. exports increase.Effect on AD:

Lower P → Lower r → Currency depreciation → Higher NX → Increased Y.

The Slope of the AD Curve: Summary

An increase in P reduces the quantity of goods and services demanded due to:

The wealth effect (P rises → C falls)

The interest-rate effect (P rises → I falls)

The exchange-rate effect (P rises → NX falls)

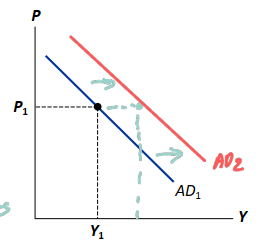

Why the AD Curve Might Shift

Any event that alters C, I, G, or NX (excluding a change in P) will cause the AD curve to shift. (AD does not depend on P)

Changes in C

Stock market boom/crash (Household wealth rises/falls → AD shifts right/left)

Preferences: consumption/saving tradeoff (S rises → C falls → AD shifts left)

Tax hikes/cuts (Disposable income ) => fiscal

Changes in I

Firms buying new computers, equipment, factories

Expectations, optimism/pessimism

Interest rates, monetary policy

Investment Tax Credit or other tax incentives

Changes in G

Central spending, e.g., defense

Local spending, e.g., roads, schools

Changes in NX

Booms/recessions in countries that buy our exports.

Appreciation/depreciation resulting from international speculation in the foreign exchange market.

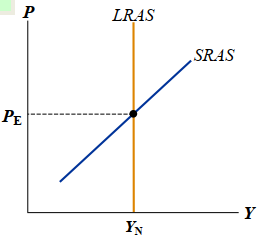

The Aggregate-Supply (AS) Curves

The AS curve shows the total quantity of goods and services firms produce and sell at any given price level.

AS is upward-sloping in the short run.

AS is vertical in the long run.

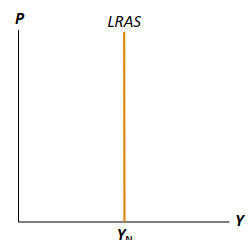

The Long-Run Aggregate-Supply Curve (LRAS)

The natural rate of output () is the amount of output the economy produces when unemployment is at its natural rate.

is also called potential output or full-employment output.

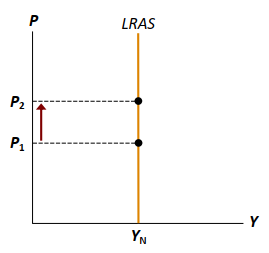

Why LRAS Is Vertical

is determined by the economy’s stocks of labor, capital, and natural resources, and on the level of technology.

An increase in P does not affect any of these, so it does not affect (Classical dichotomy).

Why the LRAS Curve Might Shift

Any event that changes any of the determinants of will shift LRAS.

Eg: Immigration rises → L rises → LRAS shifts right

Changes in L or the natural rate of unemployment

Immigration

Baby-boomers retiring

Government policies reducing the natural unemployment rate

Changes in K or H

Investment in factories, equipment

More people obtaining college degrees

Factories destroyed by a hurricane

Changes in natural resources

Discovery of new mineral deposits

Changes in technology

Productivity improvements from technological progress

Short Run Aggregate Supply (SRAS)

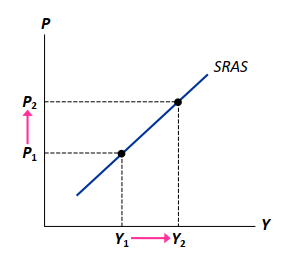

The SRAS curve is upward sloping.

Over a period of 1-2 years, an increase in P causes an increase in the quantity of goods and services supplied.

Three Theories of SRAS

Each theory involves some type of market imperfection.

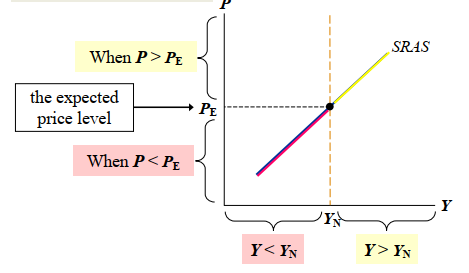

Result: Output deviates from its natural rate when the actual price level deviates from the price level people expected.

Why the SRAS Curve Slopes Upward

Common element of all 3 theories

Y deviates from when P deviates from PE

Y: Output

YN: Natural rate of output (long-run)

a > 0, measures how much Y responds to unexpected changes in P

P: Actual price level

PE: Expected price level

The Sticky-Wage Theory

Imperfection: Nominal wages are sticky in the short run, adjusting slowly due to labor contracts and social norms.

Firms and workers set the nominal wage in advance based on , the price level they expect.

If P > P^E, revenue is higher, but labor cost is not. Production is more profitable, so firms increase output and employment.

Hence, higher P causes higher Y, so the SRAS curve slopes upward.

The Sticky-Price Theory

Imperfection: Many prices are sticky in the short run due to menu costs (the costs of adjusting prices).

Firms set sticky prices in advance based on .

If the central bank increases the money supply unexpectedly, P will rise in the long run.

In the short run:

Firms without menu costs can raise prices immediately.

Firms with menu costs wait to raise prices. Consequently, their prices are relatively low, increasing demand for their products, and they increase output and employment.

Hence, higher P is associated with higher Y, so the SRAS curve slopes upward.

The Misperceptions Theory

Imperfection: Firms may confuse changes in P with changes in the relative price of their products.

If P rises above , a firm sees its price rise before realizing all prices are rising. The firm may believe its relative price is rising and may increase output and employment.

Thus, an increase in P can cause an increase in Y, making the SRAS curve upward-sloping.

SRAS vs. LRAS

The imperfections in these theories are temporary. Over time:

Sticky wages and prices become flexible.

Misperceptions are corrected.

In the long run:

AS curve is vertical

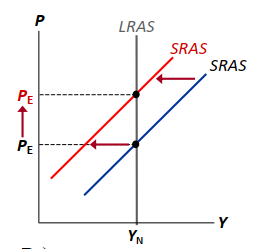

Why the SRAS Curve Might Shift

Everything that shifts LRAS shifts SRAS, too.

shifts SRAS: If rises, workers & firms set higher wages. At each P, production is less profitable, Y falls, and SRAS shifts left.

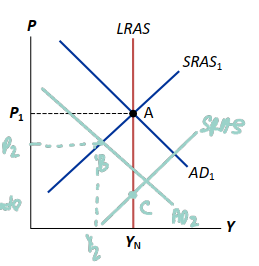

Equilibrium

In the long-run equilibrium, , , and unemployment is at its natural rate.

In the short-run equilibrium, SRAS intersects AD.

Analyzing Economic Fluctuations

Caused by events that shift the AD and/or AS curves.

Four steps to analyzing economic fluctuations:

Determine whether the event shifts AD or AS.

Determine whether the curve shifts left or right.

Use the AD-AS diagram to see how the shift changes Y and P in the short run.

Use the AD-AS diagram to see how the economy moves from the new SR equilibrium to the new LR equilibrium.

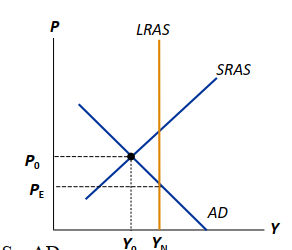

The Effects of a Shift in AD

Event: Stock market crash

Affect C → AD curve

Crash → less wealth → C falls → AD shifts left

Short run equilibrium at C

P and Y lowers => Unemployment higher

In the long run, unemployment rate > natural rate → Firms hold power → Wages fall → SRAS shifts to the right, eventually restoring full employment as the economy adjusts at initial levels

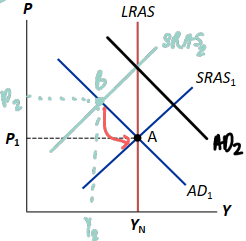

The Effects of a Shift in SRAS

Event: Oil prices rise

Rising production costs → Affect SRAS curve

Firms supply less output → SRAS shifts left

Short run equilibrium at B. P higher, Y lower, unemployment higher

From A to B, stagflation a period of falling output and rising prices

John Maynard Keynes

(1883-1946)

Argued recessions and depressions can result from inadequate demand; policymakers should shift AD.

Famous critique of classical theory:

Economists set themselves too easy, too useless a task if in tempestuous seasons they can only tell us when the storm is long past, the ocean will be flat.

"The long run is a misleading guide to current affairs. In the long run, we are all dead."

“time will heal all wounds” ???

Conclusion

This chapter introduced the model of aggregate demand and aggregate supply, which helps explain economic fluctuations.

Keep in mind: these fluctuations are deviations from long-run trends

In the next chapter, we will learn how policymakers can affect aggregate demand with fiscal and monetary policy.