Lecture 13: Fiscal Policy and Demand

Fiscal Policy and Demand Lecture Notes

It is the use of congress and the President

Long-Run Spending and Tax Policies

Impact of Spending and Tax Policies:

Can affect the supply side of the economy, expanding potential and increasing levels/growth rates of output over the longer run.

Examples of long-run policy impacts:

Public Research and Development: Could raise technology.

Corporate Tax Reform: May increase capital stock.

Increasing Educational Spending: Can raise human capital.

Other Goals for Money:

Spend it on climate maybe climate gets better, spend it on something expecting benefit in return.

1. Discretionary Fiscal Policy

Definition

Fiscal Policy: Changes in government spending or taxes to have a short-run impact on the demand side of the economy, often with a countercyclical motivation.

Example of Impact:

Increasing government spending (G) can increase output (Y).

The focus is on immediate effects on capital and labor utilization, not on longer-run supply-side effects.

Example Analogy: Digging holes and refilling them is equivalent to building a much-needed bridge.

Reasons for Expansionary Fiscal Policy

Uncertainty: The efficacy of monetary and fiscal policy suggests using a combination of both.

Double Benefits: To increase demand while addressing other issues, such as protecting vulnerable populations or investing in infrastructure.

Low Interest Rates: Situations where interest rates are at zero while the economy is still in deep recession.

Political Motivation: Political leaders may act during recessions or slowdowns, or due to other influences (e.g., wartime spending).

Contractionary Fiscal Policy

Typically not done for countercyclical reasons but due to concerns related to fiscal sustainability.

Aggregate Demand and Fiscal Stimulus

Rising Aggregate Demand: How stimulus is divided across output (Y) or inflation (P).

Model Relation: The relationship is shown as: If nominal demand increases significantly while supply does not, inflation may result without an increase in output.

Fiscal Policy Multiplier

Direct Effects:

If the government raises purchases, the output increases as follows:

Resulting change:

If the government cuts taxes or increases transfers:

Resulting change:

Indirect Effects of the Fiscal Multiplier

May differ from 1 due to:

Traditional Keynesian Multiplier: Depends on the composition of tax cuts or spending increases.

Crowding Out: Resulting from the central bank's choices and the state of the economy.

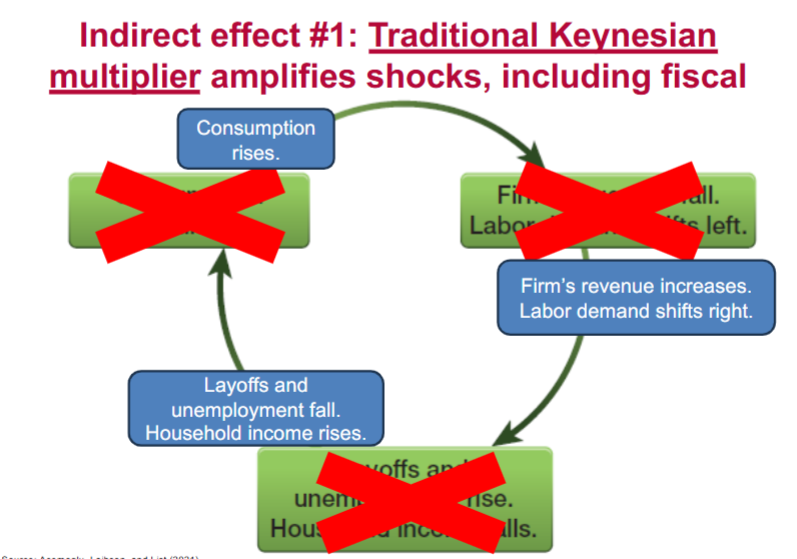

Indirect Effect #1: Traditional Keynesian Multiplier

Amplifies shocks related to fiscal policy.

Targeting Households with High Marginal Propensity to Consume:

Lower-income households, or those temporarily with lower income who wish to smooth consumption.

Loans for Businesses:

Support businesses experiencing temporary liquidity needs.

Quick Spending:

Infrastructure spending often has delays; policies that spend faster can have more immediate impacts.

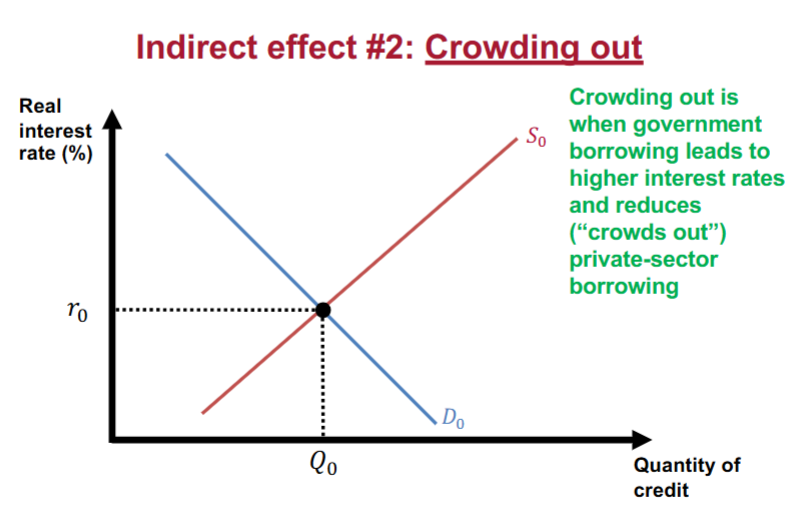

Indirect Effect #2: Crowding Out

Definition:

Crowding out occurs when government borrowing leads to increased interest rates, reducing private-sector borrowing.

Illustration of Crowding Out

i. Government Borrowing Example:

Government borrows $100 billion for infrastructure (increases G by $100 billion).

Resulting increase in interest rates causes:

Businesses cut investment (including homebuilding) and households cut consumption by $60 billion, resulting in a net demand increase of just $40 billion (ignoring the traditional Keynesian multiplier).

Central Bank's Role in Crowding Out

The degree of crowding out correlates with the central bank's actions:

Keep interest rates low → No crowding out → High multiplier. - covid, financial crisis

Allow interest rates to rise naturally → Partial crowding out → Medium multiplier.

Actively raise interest rates → Complete crowding out → Zero multiplier.

Summarizing Fiscal Policy and Demand

Equation:

Consumer Spending:

Generally increases positively with traditional Keynesian multiplier outweighing crowding out from rising interest rates.

Investment Decline:

Business and residential investment may decline if interest rates rise without counteraction from the central bank.

Multiplier Implication:

If increase in consumption (C) is greater than decline in investment (I), then the multiplier is greater than 1; otherwise, the opposite holds.

Multiplier Estimates

Estimates vary widely based on CBO (2020) and academic research:

Unemployment Insurance: 1.2

Checks for Individuals: 0.8

Assistance to States and Localities: 1.1

Business Tax Cuts: 0.1

First-year estimates range from:

Individual Tax Cuts: 0.6 to 1.2

Spending Increases: 0.3 to 1.2.

Limitations of Unlimited Fiscal Expansions

Inflation Risks:

May lead to increased inflation rather than real output, especially at potential output.

Central Bank Offset:

Likely to counter undesired fiscal policy due to inflation targets, potentially resulting in "full crowd out".

Costs of Deficits/Debt:

To be discussed in future classes.

2. Automatic Stabilizers

Definition

Discretionary Fiscal Policy: New legislation affecting spending or taxes based on macroeconomic conditions. Congress passes a law and the President signs it.

Automatic Stabilizers: Mechanisms that cause taxes to decrease, and spending (such as unemployment insurance benefits) to increase automatically when the economy weakens.

Examples of Automatic Stabilizers

Income Fall Impacts:

If family income declines, tax payments also decrease.

Loss of income may qualify families for low-income government benefits.

If a worker loses a job, they receive unemployment insurance benefits.

Potential Enhancements to Automatic Stabilizers

Increase in Economic Share:

Higher taxes and spending leading to larger automatic stabilizers.

Progressive Structures:

More progressive taxes/spending could enhance effectiveness.

Macro-Condition Triggering Programs:

More programs that activate based on economic conditions would strengthen stabilizers.

3. The Fiscal Response to COVID-19

Overview

The most substantial fiscal response to an economic crisis recorded, focusing on calendar years.

Fiscal Stimulus as a percent of GDP from 2008–2010 compared to 2020-2021 is highlighted:

Sources include calculations based on various economic boards and analysis organizations.

Comparative Stimulus Data

Much larger fiscal response during the COVID-19 crisis compared to other countries in 2020 and 2021.

Automatic stabilizers vs. discretionary fiscal stimulus during the crisis:

Notable increases reported across multiple countries.

Impact on Disposable Personal Income

Transfers during Pandemic: Resulted in a significant increase in real disposable personal income, with forecasts indicating trends in increase or decrease as compared to the projected growth rate.

Estimating Multipliers for Fiscal Response

Analysis of second wave of fiscal response may shed light on multiplier effects observed.

Estimated GDP impacts from fiscal stimulus initiatives over the specified period (2020-2023).

Comparison of actual increments seen in GDP against initial forecasts.

Post-Fiscal Stimulus Economic Evaluation

Illustration showing probable nominal GDP rise following fiscal stimulus against January 2020 forecasts.

Assessment of GDP and employment growth post-stimulus, with some aspects attributed to natural recovery trends.

Unemployment and Inflation Post-COVID Response

Rapid declines in unemployment rates accounted for; however, continued discussions around inflation pressures exist.

Analysis of overall price changes in Personal Consumption Expenditures (PCE) indexed against unemployment rates, with data spanning from 2007 to 2025.

Debated Issue Highlights

Factors contributing to economic recovery trajectories classified by nature of crisis vs. policy size.

Inquiries on the necessity for precision-targeting responses in future policy discourses.

Consequences of debt implications beyond inflation considerations, inviting further investigations into fiscal impact assessments.

4. How Activist Should Countercyclical Policy Be?

Fundamental Countercyclical Policy Capabilities

Monetary and Fiscal Policy Role:

Can be utilized to counteract shocks, thereby helping the economy return to full employment more rapidly than it might naturally.

Limitations on Growth:

While these policies help recover from current economic shocks, they cannot sustainably increase growth rates in economies operating at potential.

Relative Roles of Monetary vs. Fiscal Policy

Aspect | Monetary Policy | Fiscal Policy |

|---|---|---|

Technocratic | Yes (Independent) | No (Political cycles) |

Nimble/Reversible | Yes (Lagged Impact) | No |

Effective Unlimited Magnitude | No (cannot cut below zero) | Yes (Unlimited) |

Encourage Private Investment | Yes (Lowers Rates) | No (Crowd Out) |

Target Additional Goals | No | Yes |

Concerning Side Effects | Inflation and Stability | Inflation and Debt Sustainability |

Questions to Determine Policy Activism

Speed of Economic Adjustment:

Evaluate how quickly the economy would revert on its own.

Timing of Interventions:

Assess the precision of policy intervention timings by policymakers.

Side Effects Severity:

Understand how serious the collateral impacts of counter-cyclical policies are, such as inflation, financial stability, crowding out private investment, and public debt stability.

Conclusion on Activism Dependence

The degree of activism in countercyclical policy should depend on context, with the position being that it is not absolutely fixed, suggesting adaptability to prevailing circumstances and outcomes.