CIE AS Level Accounting: Reconciliation and Correction of Errors

Bank Reconciliation

The closing balance of the bank statement may be different to the closing balance in the cash book due to a numberof reasons. These reasons include:

cheques not banked

bank charges not known until bank statement released

cheques credited but not debited

Unpresented cheques: cheques drawn and presented in the cash book but not yet presented to the bank

Uncredited/Outstanding bankings: cash/cheques received and paid into the bank and recorded in the cash book but have not yet appeared on the bank statement

Direct debits: an authority granted by the business to a third-party for a fixed or variable payment to be made of the request of the third-party e.g water bill

Standing orders: a fixed payment made at regular intervals by the bank

The bank reconciliation statement is important for the following reasons:

identifies errors in the cash book

however, there are errors that the trial balance will not identify, such as:

ommission — records are completely left out

compensating — errors on incorrect sides cancel each other out

commission — incorrect accounts of the same class

principle — incorrect accounts of different class

original entry — transferring amounts from source documents

reversal — accounts wrongly posted on their sides

identifies errors in the bank statement

enables missing entries to be accounted for

identifies out-of-date cheques

identifies dishonoured cheques

acts as a fraud deterrent

Method

update the cash book with any items appearing on the bank statement but not appearing in the cash book

pepare a bank reconciliation statement as follows:

Balance as per bank statement | XXX |

|---|---|

Less: Unpresented cheques | (XXX) |

Add: Oustanding bankings | XXX |

Balance as per cash book | XXX |

OR

Balance as per cash book | XXX |

|---|---|

Add: Unpresented cheques | XXX |

Less: Outstanding bankings | (XXX) |

Balance as per bank statement | XXX |

Suspense

When errors are identified either in the trial balance or in various accounts, a suspense account will be opened.

Suspense accounts are used for the following reasons:

as a place for unusual items to be put until a decision can be made about the correction

as a temporary account to deal with errors that have caused a difference between debit and credit accounts

for single entry errors — only half of the financial transaction has been posted

for same side entry errors — both entries have been posted to the same sides rather than its respective debit and credit entry (duality concept)

for unequal entry errors — entries have been made on the correct sides but the figures differ

for arithmetical errors — one or more accounts being over or understated and therefore, the trial balance is not balancing

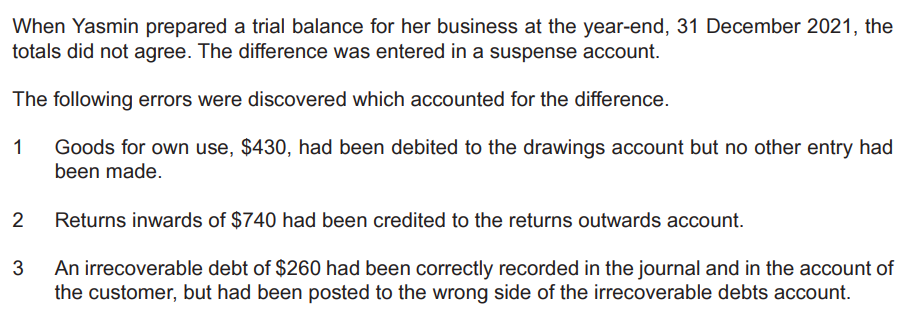

E.g.