ECON C11.docx

Chapter 11 – Money and Banking

11.1 The Nature of Money

What is money?

Any generally accepted medium of exchange.

Functions of Money

Medium of exchange

Store of Value

Unit of account

Medium of Exchange

Anything that is generally accepted in return for goods and services sold.

If there was no money, goods and services would have to be exchanged by barter.

If you have a good and want to buy something else, you must find someone that has what you want and wants what you have (Double coincidence of wants).

Money solves this problem and allows people to specialize.

What makes a good medium of exchange?

Easily recognizable

High value relative to weight

Divisible

Durable

Very hard if not impossible to counterfeit

Store of Value

Ability to store purchasing power

For money to be a good store of value, it needs to have a purchasing power that is relatively stable over time.

Unit of Account

Used for accounting purposes (Provides a way to measure revenue, costs, profit etc.)

Common measure of value.

For example, in Canada, when asked how much something is worth, we give our answer in Canadian dollars.

Money Need Not Be Physical

Money need not have a physical presence to serve as a medium of exchange, a store of value, and a unit of account.

Most Canadians hold most of their money in their bank accounts, and they can easily make a transaction with a debit card.

In the overall economy, there is much more money in the form of bank deposits than there is in the form of physical money.

Metallic Money

Many commodities have been used as money, but precious metals, particularly gold and silver proved to have great advantages (easily recognizable, divisible, durable etc).

Until the idea of coins came around, people would carry the metals around in bulk and every time a purchase was made the metals would have to be weighed.

The invention of coinage created a role for a central authority figure.

The coins were stamped guaranteeing the amount of precious metal contained within the coins.

Practice of clipping a thin slice off the edge became common.

To solve this problem the coins were minted with a rough edge (milling).

King or queen would often debase the coins for personal gain which eventually led to inflation.

Paper Money

Goldsmiths would keep people's gold in their safes and give them receipts promising to return their gold on demand.

Later, commercial banks issued bank notes that were convertible into gold.

There were bank notes from many different banks circulating.

Fractionally Backed Paper Money

Eventually goldsmiths realized that they didn’t need to hold enough gold to repay every claim made on that gold.

Banks realized the same thing.

They could issue more paper money convertible to gold than they had in their gold reserves.

They could then lend this money out through loans to households and firms.

The currency is fractionally backed by reserves.

Possibility of bank runs.

Fiat Money

Initially, national currencies like the Canadian and U.S. dollar were backed by gold.

Gold standard: A currency standard whereby a country’s currency is convertible into gold.

By around 1930 Canada left the gold standard.

Fiat money: Paper money or coinage that is not backed by nor convertible into anything but is decreed by the government to be legal tender.

Legal tender: Anything that by law must be accepted when offered for the purchase of goods or repayment of debt.

Modern Money: Deposit Money

Today if you want to make a purchase you can choose between physical currency, cheque, or electronic transfer (debit card).

Money held by the public in the form of deposits with commercial banks is deposit money.

Bank deposits are considered money.

Today, just as in the past, banks create money by issuing more promises to pay (deposits) than they have cash reserves available to pay out.

11.2 The Canadian Banking System

Two types of institutions make up a modern banking system:

Central bank (Bank of Canada)

Financial intermediaries

“Commercial banks” refer to financial intermediaries that are deposit accepting and loan granting.

The Bank of Canada

The Bank of Canada commenced operations on March 11,1935.

The organization of the Bank of Canada is designed to keep the operation of monetary policy free from day-to-day political influence.

The Bank of Canada has considerable autonomy, but the ultimate responsibility for the Bank’s actions rests with the government.

This system is known as “joint responsibility.”

The basic functions of the Bank of Canada:

Banker to the commercial banks

Banker to the federal government

Regulator of the money supply

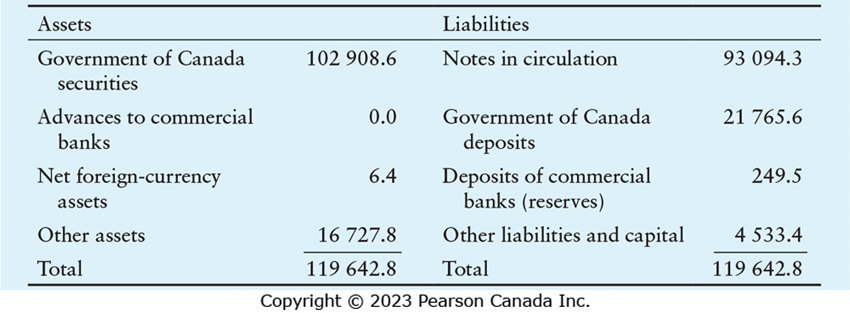

Table 11-1 shows the Bank of Canada’s balance sheet from December 2019, just before the pandemic began.

The balance sheet of the Bank of Canada shows that it serves as banker to the commercial banks and to the government of Canada, and as issuer of our currency; it also suggests the Bank’s role as regulator of the money supply. The principal liabilities of the Bank are the basis of the money supply. Bank of Canada notes are currency, and the deposits of the commercial banks give them the reserves they need to create deposit money. The Bank’s holdings of Government of Canada securities arise from its operations designed to regulate the money supply.

The Bank’s Balance Sheet During the COVID-19 Pandemic

Beginning early in 2020, the Government of Canada issued a massive amount of new bonds to provide financial relief to unemployed workers and businesses whose revenue had collapsed.

The Bank of Canada played an important role by purchasing a large amount of these newly issued bonds, thereby expanding the amount of money in the banking system.

Banker to Commercial Banks

The Bank of Canada accepts deposits from commercial banks and will on order transfer them to the account of another bank.

The Bank of Canada acts as a lender of last resort to commercial banks.

During times of uncertainty when banks are hesitant to lend to each other the Bank of Canada will often step in and provide that service.

Banker to the Federal Government

The Government of Canada also holds an account with the Bank of Canada in which they make deposits, write cheques, and make electronic transfers.

Regulator of the Money Supply

There are many different definitions of the money supply, but most definitions include at a minimum the currency in circulation plus deposits held at commercial banks.

The Bank of Canada can change the money supply by buying or selling Government of Canada bonds.

When the Bank of Canada purchases government bonds from commercial banks they credit their account.

When the Bank of Canada sells government bonds to commercial banks they reduce the balance of their account.

Commercial Banks in Canada

Commercial bank ‒ a privately owned, profit-seeking institution that provides a variety of financial services, such as accepting deposits from customers and providing loans, mortgages, and other financial products.

The Provision of Credit

The most important role played by commercial banks is that as financial intermediary.

They accept deposits from firms and households that have money they do not currently need, and they make loans to firms and households that need credit.

Households use credit to purchases things like houses and cars.

Firms use credit for things like paying workers before receiving payment for the goods they sell or financing capital investments.

Interbank Activities

Sometimes commercial banks share loans if the credit needs of a large firm are too much for one bank to handle.

Banks work together so depositors from one bank can pay or receive payment from depositors at other banks.

Commercial Bank Reserves

Commercial banks only keep enough physical currency on hand to meet depositors' day to day needs for cash.

They keep physical currency in their vaults and can convert their deposits with the Bank of Canada into physical currency on demand.

Physical currency + deposits with the Bank of Canada are what we call the banks reserves.

Bank run: A situation in which many depositors rush to withdraw their money.

Bank of Canada can help a bank during a bank run by lending them money directly or buying their government bonds.

Bank runs are rare in modern times as a large portion (up to $100,000 per deposit) of deposits are insured by the Canada Deposit Insurance Corporation (CDIC).

Reserves

The Canadian banking system is a fractional-reserve system.

Fractional-reserve system: A banking system in which commercial banks keep only a fraction of their deposits in cash or on deposit with the central bank.

Reserve ratio: The fraction of deposits that the bank actually holds as reserves.

Target reserve ratio: The fraction of deposits that the bank would ideally like to hold as reserves.

Excess reserves: Actual reserves minus target reserves.

11.3 Money Creation by the Banking System

Some Simplifying Assumptions

To focus on the essential aspects of how commercial banks create money, suppose that banks can invest in only one kind of asset—loans—and they have only one kind of deposit.

We assume that all banks have the same target reserve ratio, which does not change, and that there is no cash drain from the banking system.

What is a new deposit?

Person might immigrate to Canada and bring cash which they then deposit into a Canadian bank.

Person might find some long-lost cash in their couch and deposit that money into a Canadian bank.

Bank of Canada purchases a government bond from a person or a firm.

The Creation of Deposit Money

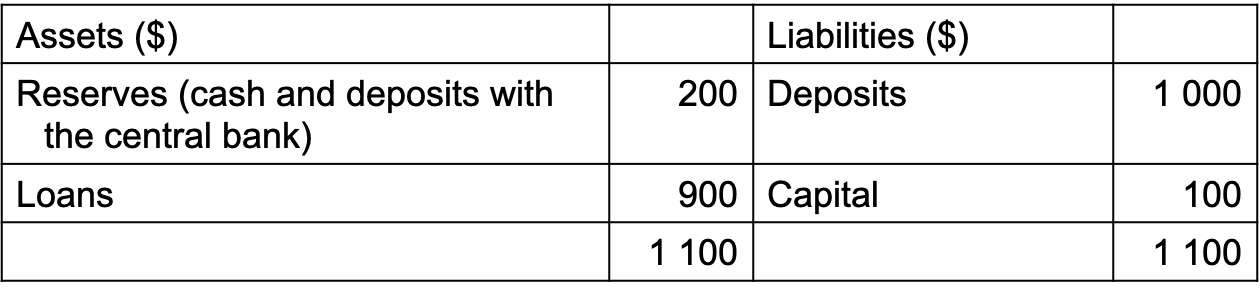

The bank initially has a reserve ratio of 20 percent.

TD has reserves equal to 20 percent of its deposit liabilities. The commercial bank earns profits by finding profitable investments for much of the money deposited with it. In this balance sheet, loans are its income-earning assets.

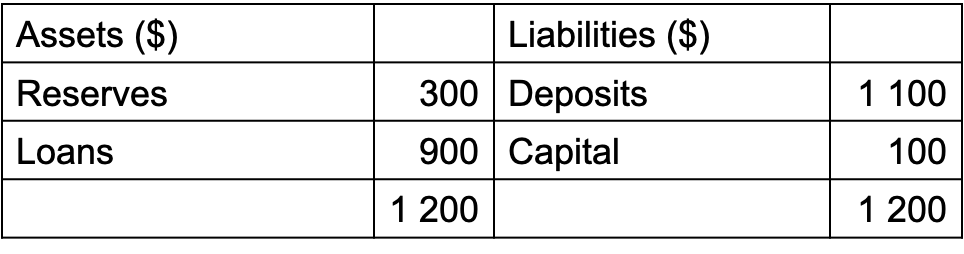

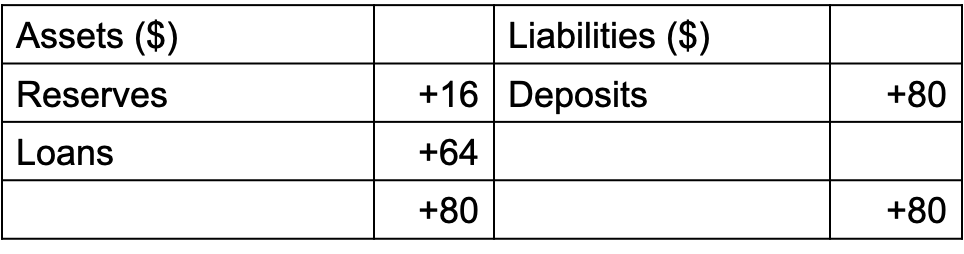

A new deposit of $100 raises the bank’s reserve ratio to 27%.

The new deposit raises liabilities and assets by the same amount. Because both reserves and deposits rise by $100, the bank’s actual reserve ratio, formerly 0.20, increases to 0.27. The bank now has excess reserves of $80.

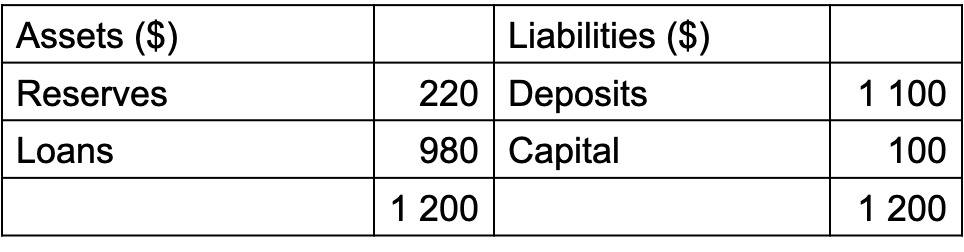

The bank now has $80 of excess reserves which it can lend.

TD converts its excess cash reserves into new loans. The bank keeps $20 as a reserve against the initial new deposit of $100. It lends the remaining $80 to a customer, who writes a cheque to someone who deals with another bank. Comparing Table 11-3 and 11-5 shows that the bank has increased its deposit liabilities by the $100 initially deposited and has increased its assets by $20 of cash reserves and $80 of new loans. It has also restored its target reserve ratio of 0.20.

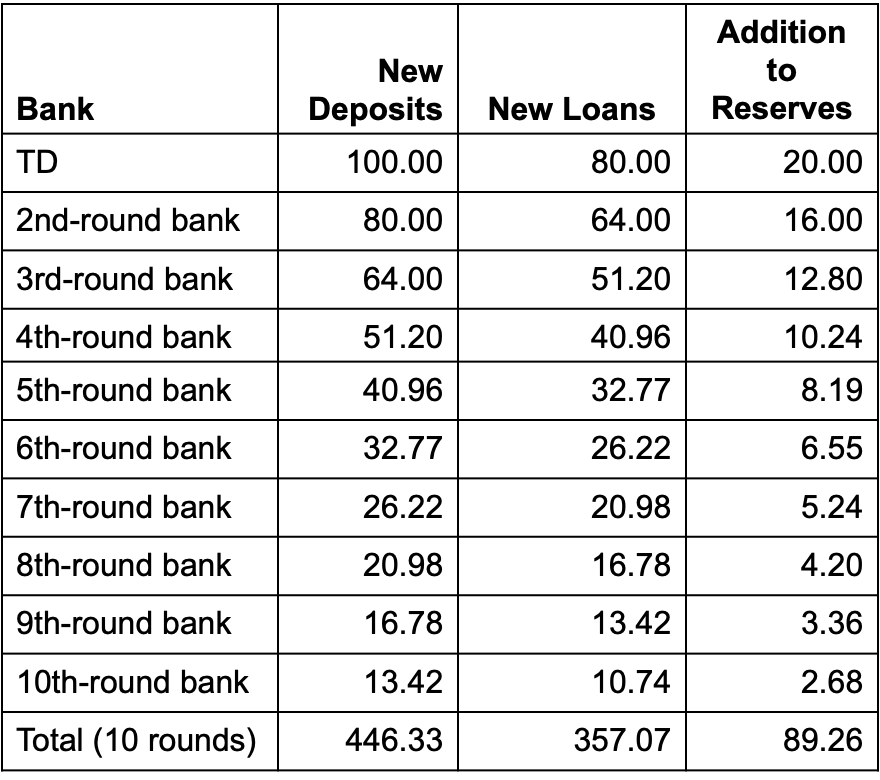

The second-round bank receives $80 in new deposits and expands its loans by $64.

Second-round banks receive cash deposits and expand loans. The second-round banks gain new deposits of $80 as a result of the loan granted by TD. These banks keep 20 percent of the cash that they acquire as their reserve against the new deposit, and they can make new loans using the other 80 percent.

The Sequence of Loans and Deposits After a Single New Deposit of $100

The Creation of Deposit Money

If ν is the target reserve ratio, a new deposit to the banking system will increase the total amount of deposits by 1/ν times the new deposit.

In our example, ν = 0.2 and the new deposit

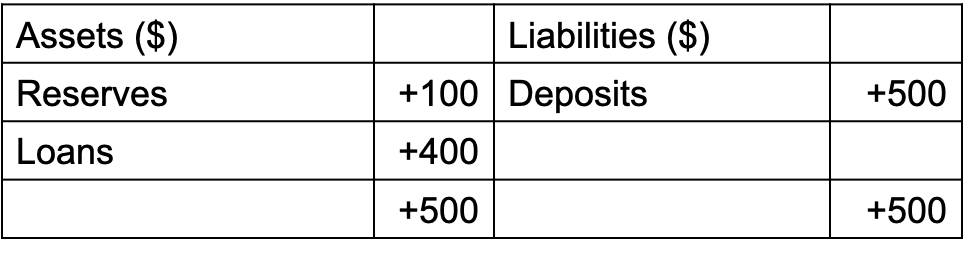

is $100. So total deposits eventually increase by $100 × 1/0.2 = $500.With no cash drain from the banking system, a banking system with a target reserve ratio of ν can change its deposits by 1/v times any change in reserves.

ΔDeposits = ΔReserves/ν

The total change in the combined balance sheets of the entire banking system is shown in Table 11-8

The reserve ratio is returned to 0.20. The entire initial deposit of $100 ends up as additional reserves of the banking system. Therefore, deposits rise by (1/0.2) times the initial deposit – that is, by $500.

Reserves and Cash Drains

Deposit creation depends on the decisions of bankers.

If commercial banks must choose to lend their excess reserves, otherwise, no deposit expansion.

If people decide to hold an amount of cash equal to a fixed fraction of their bank deposits, any multiple expansion of bank deposits will be accompanied by a cash drain.

If c is the ratio of cash to deposits that people want to maintain, the final change in deposits will be given by: ΔDeposits = (New Cash Deposit)/(c + ν)

11.4 The Money Supply

The money supply is the total quantity of money that is in the economy at any time.

Economists use several alternative definitions for the money supply.

Each definition includes the amount of currency in circulation plus some types of deposit liabilities of the financial institutions.

Money supply = Currency + Bank deposits

Kinds of Deposits

Demand deposit: Chequable deposits that are transferable on demand.

Term deposit: An interest earning bank deposit, subject to notice before withdrawal.

Definitions of the Money Supply

Two commonly used measures of money in Canada today are M2 and M2+.

M2 is currency plus demand and term deposits at the chartered banks.

M2+ is M2 plus similar deposits at other financial institutions.