Cost of Capital

How can you calculate the discount rate if you are given the costs of equity and debt?

Tax rate: 35%

Asset 100

Equity 60 - 17%

Debt 40 - 8%

The weighted average cost of equity and debt -

𝟏𝟕% ∗ 𝟔𝟎 /𝟔𝟎+𝟒𝟎 + 𝟖% ∗ 𝟒𝟎/𝟔𝟎+𝟒𝟎*(1-0.35)

Calculate the expected return of a stock with a 1.6 beta if the expected return on the market portfolio is 8% and the risk free rate is 2 %.

Using the CAPM

E(r) = 2 % + 1.6(8 % – 2 %)

= 2 % + 1.6(6 %)

= 2 % + 9.6 %

= 11.6 %

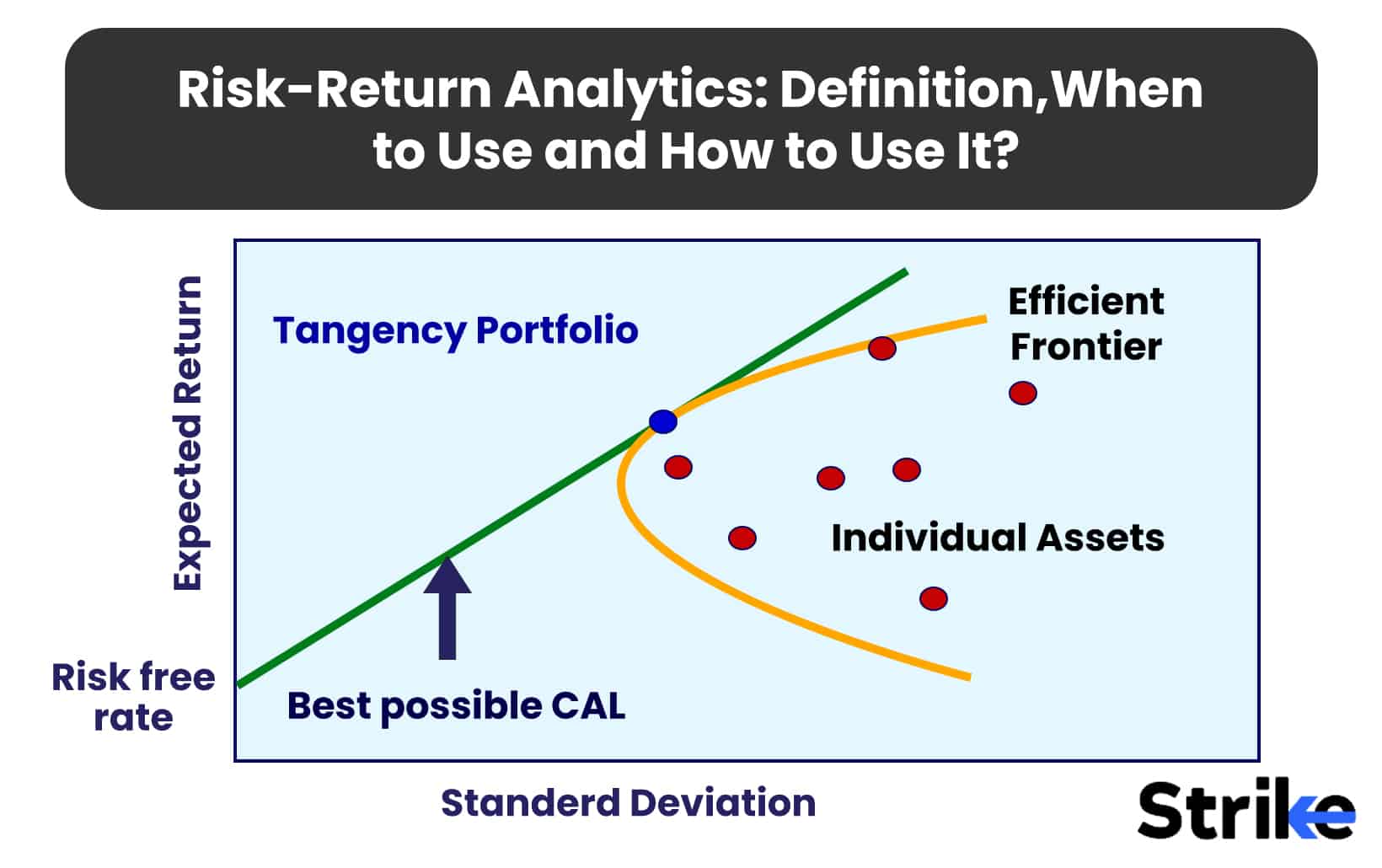

Risk → Mathematical Model → Return

Market portfolio - S&P 500

What is a portfolio that fluctuates solely due to systematic risk?

Market Portfolio that contains all shares and securities in the market, with each asset weighted in proportion to its total presence in the market

A good proxy for market portfolio is the S&P 500

Standard deviation → Total risk

Slope value = (re-rf)/(rm-rf) = B/I

re= rf + B x (rm-rf)

(re-rf) = B x (rm-rf)

Risk premium - additional return for taking that risk

Affects it:

Systematic

Non diversifiable

Relevant base market portfolio - global market portfolio as the benchmark

Relevant market portfolio - us market risk premium

r26 = (P26 + D26) − P25/ P25

Total risk - systematic and unsystematic

CAPM has merit when applied to a company with operation in integrated markets

Problem

Not fully integrated

Solution

Consider global and local costs

Know how to convert one discount rate to the other like in the case study

Look back at the spot exchange rate example in canvas

Know how to find it on a calculator