Better Money - 4. Fiat standard

Under a metallic standard, the monetary unit is conventionally defined as a specified mass of a particular metal.

In a fiat standard, the monetary unit established by fiat is merely one unit of itself.

It is not redeemable for any commodity that has non-monetary uses.

Governments issue units of basic fiat money in the form of coins and central bank currency notes.

A privately issued medium of exchange, such as bitcoin, is not fiat because it is not established by government.

It is money consisting of mere tokens which can neither be employed for any industrial purpose nor convey a claim against nobody.

However, inconvertible currency is not evidence of debt.

While the quantity of bank-issued money is limited by market forces, the quantity of fiat money is not.

Fiat money does not have a market-governed supply, or a standard upward-sloping supply curve.

The supply is exclusive to government.

There is not any non-monetary demand.

1. How fiat standards arose

Central government gave a legal monopoly of note-issue to a single institution, which became a central bank.

The liabilities of the central bank became so widely accepted that they displaced specie as the reserves for other banks.

Government suspended redemption of central bank liabilities permanently once they achieved wide circulation.

In no known historical case has an irredeemable money standard resulted from a free-market-driven evolution of bank reserves.

Economically, users prefer bank-issued money with a fixed value in units of the standard money.

If banks announced irredeemability, users would want to cash out.

Legally, only a bank that the government protects from ordinary contract enforcement has the immunity to unilaterally end its obligation to pay the bearer.

Fiat money gives an efficiency gain by not having to hold real goods in inventory in banks.

It saves the public real resources consumed by mining and storage of real gold.

However, given that fiat money is involuntarily imposed, we cannot presume a Paretian efficiency gain.

Governments concerned with real efficiency would have wanted to avoid the inefficiencies caused by inflation.

Further, a concern for reducing the resource cost does not explain the timing of the switch.

Most governments wanted to escape the constraints that gold redeemability put on expansionary monetary policy.

It also allows for social control of money, prices and higher tax revenue.

“Over the years, all the governments in the world, having discovered that gold is, like, rare, decided that it would be more convenient to back their money with something that is easier to come by, namely: nothing.”

2. Why is a Fiat money valued

Why do units of fiat money have a positive market value despite being intrinsically useless outside of a monetary role?

At one level, the answer is simply supply and demand.

It does not answer the question of how the convention arose of treating a particular intrinsically useless item as money.

People value fiat dollars because the US government compels creditors to accept it.

The historical developments habituate people to accept redeemable paper money, with the result that, when redemption ends, they continue accepting it so long as it works, so long as others follow the same strategy.

The Somali shilling is an unusual example of people accepting fiat money without backing by the government.

There are two potential equilibria: the item that would be currency can have a positive value (acceptance) or a zero value (non-acceptance).

Such fragility is what commentators have in mind when they speak of money as a “shared illusion” or an “arbitrary social construct.”

When the public abandons a fiat money in which prices are denominated, the result is a high or hyper-inflation.

A commodity like gold, valued for its usefulness, with additional units costly to produce, retains a positive value even when demonetized.

However, money is more readily or conveniently transactable than bonds.

3. Supply and demand for fiat money

A central bank controls the supply of a fiat money by expanding or contracting its own balance sheet.

The US monetary base is the sum of currency in circulation plus commercial bank reserve deposits at the Fed.

The central bank can create as many claims against itself as it chooses, being unconstrained by any obligation to redeem its liabilities for an asset it cannot create.

The stock of money held by the public, measured by M2, is a multiple of the monetary base.

Since 2008, the Fed strongly influences the money multiplier by choosing the interest rate it pays.

The Federal Reserve has two main tools for controlling the growth of M2:

The Fed can arbitrarily expand or contract the monetary base through bond purchases and sales.

The Fed can set the interest rate on reserves above or below other rates.

Although the commercial banks can take actions that (unintentionally) change the money multiplier, the central bank can offset any such change.

Because it can control the rate of growth of money supply, the central bank can control the rate of growth of the price level, also known as the rate of inflation.

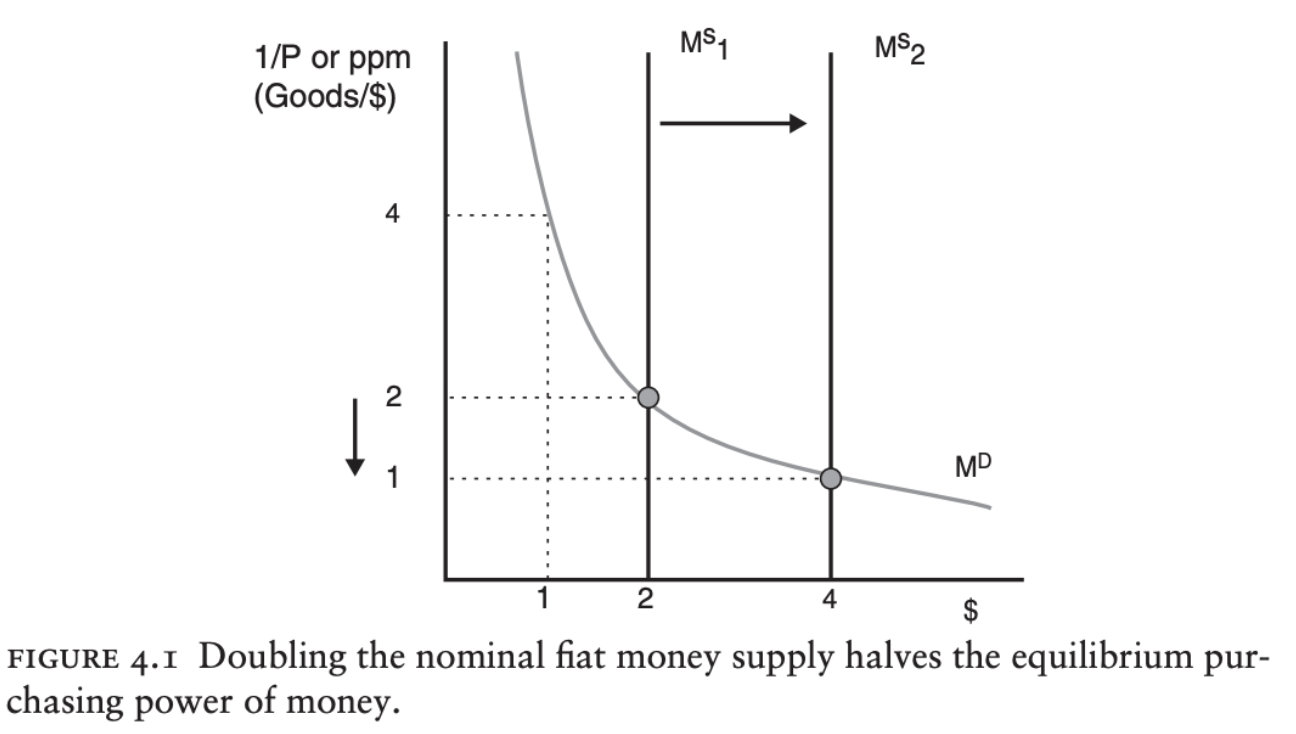

4. The quantity-of-money theory of the price level

The “quantity theory of money” (QTM) proposition that the price level is proportional to the quantity of money, other things equal, applies to a fiat standard.

MV = Py

5. How fiat standards have performed on inflation

In the US, the closing of the gold window followed a period of rising inflation rates after 1965.

The Federal Reserve had loosened monetary policy to reduce unemployment rather than maintaining moderate money growth to keep inflation close to zero.

Year-over-year inflation rate peaks were reached at 12.2% and 14.6%.

Fiat money regimes have resulted in even higher inflation rates in most other countries.

6. Inflation is burdensome even when the inflation rate is correctly anticipated

A monetary regime that produces a higher average inflation rate, imposes at least four burdens on money-holders:

The transfer from public to government: ongoing price inflation is normally due to ongoing expansion in the quantity of money.

Governments can produce new money units at practically zero cost.

Introducing new units dilutes the value of existing units.

The process transfers wealth from money-holders to the government.

The technical name for the government's profit from money creation is seigniorage.

The deadweight burden on money holders: at a higher inflation rate, a household or firm is more heavily penalized for holding currency and some deposits that do not pay interest.

Households lose consumer surplus, and business firms lose net income.

Unindexed taxes: higher inflation can significantly increase effective tax rates and amplify the distortive effects of those taxes.

The higher the inflation rate, the greater the real tax burden, and the greater the discouragement to investment and capital formation.

Ragged price adjustments: lower inflation rates are associated with less “raggedness” in price adjustments (some prices rising early in the process and others catching up later) and thereby less “noise” in relative prices.

7. Unanticipated inflation is even worse than anticipated inflation

Additional harms are added when the inflation rate is surprisingly high.

Risk surrounding the inflation rate means that the lenders and borrowers face an inflation risk in addition to a default risk.

When inflation is higher than anticipated, reducing the value of dollars repaid below what was reckoned, it harms the creditor (and benefits the debtor).

Fiat standard price levels drift with no tendency to return to a predictable underlying trend.

Savers and financial intermediaries are less able to predict what a dollar will be worth in ten to fifty years. They are accordingly less eager to buy.

8. Fiscal discipline under fiat money

Under a gold standard, government bonds are nearly free of inflation risk but not of default risk.

Under a fiat standard, the reverse is true.

9. Business cycles have not been milder under fiat money regimes

It has often been claimed that a fiat standard valuably enables a central bank to conduct a counter-cyclical monetary policy that dampens business cycles (reduces the volatility of real output or the average level of unemployment).

The Keynesian approach calls for a data-driven central bank to vary its monetary policy as needed to stimulate an economy.

Greater macroeconomic stability is not evident in the historical record of fiat standards, however.

Central banks in practice tend to err on the side of tightening policy too late rather than too soon

10. Seigniorage: the profit from issuing fiat money

A national fiat money offers a national government a quick and easy way to fund its spending.

Unlike the medieval process of generating seigniorage revenue by calling in the existing silver coins and reminting them into a larger number of coins with less silver in each coin, enlarging the stock of fiat money is easy.

A central bank can expand the nominal stock to whatever extent it desires, with practically zero production cost.

Hyperinflations in history have all happened under fiat regimes.

11. The danger of fiscal dominance over monetary policy

To analyze unpleasant monetarist arithmetic, we begin with a government budget constraint: G-T= \Delta D + \Delta M

G: government expenditure

T: tax revenue

D: change in government debt held by the public

M: change in government-issued money

A budget deficit requires financing from some combination of bond finance (borrowing) and seigniorage finance.

12. The case for a fiat standard

Given the checkered history of fiat monies, why do so many economists defend fiat standards?

Mostly they defend an ideal version of how a fiat standard could perform.

In principle, appropriate management of the quantity of fiat money can achieve whatever nominal target the economist thinks best for the macroeconomy.

Friedman's "optimum quantity of money" calls for a negative inflation rate to bring the nominal interest rate on Treasury bills down to the zero nominal rate paid on Federal Reserve Notes.

Under a gold standard or a Bitcoin standard, the supply of money is governed by market forces, and its behavior does not guarantee the achievement of any of these policy targets.

13. Can fiat central banks be credibly constrained?

But will a central bank in practice successfully pursue the nominal target assigned to it?

The problem is getting the central bank to stick to its assigned task rather than neglecting it while pursuing other goals.

14. Is a private fiat-like money feasible?

Monetary theorists at one time imagined systems where private irredeemable monies would promise a competitive interest return or stable purchasing power.

We have seen the launching of cryptocurrencies, which constrains expansion in the number of units and, at least before widespread monetary use, leaves their purchasing power unstable.