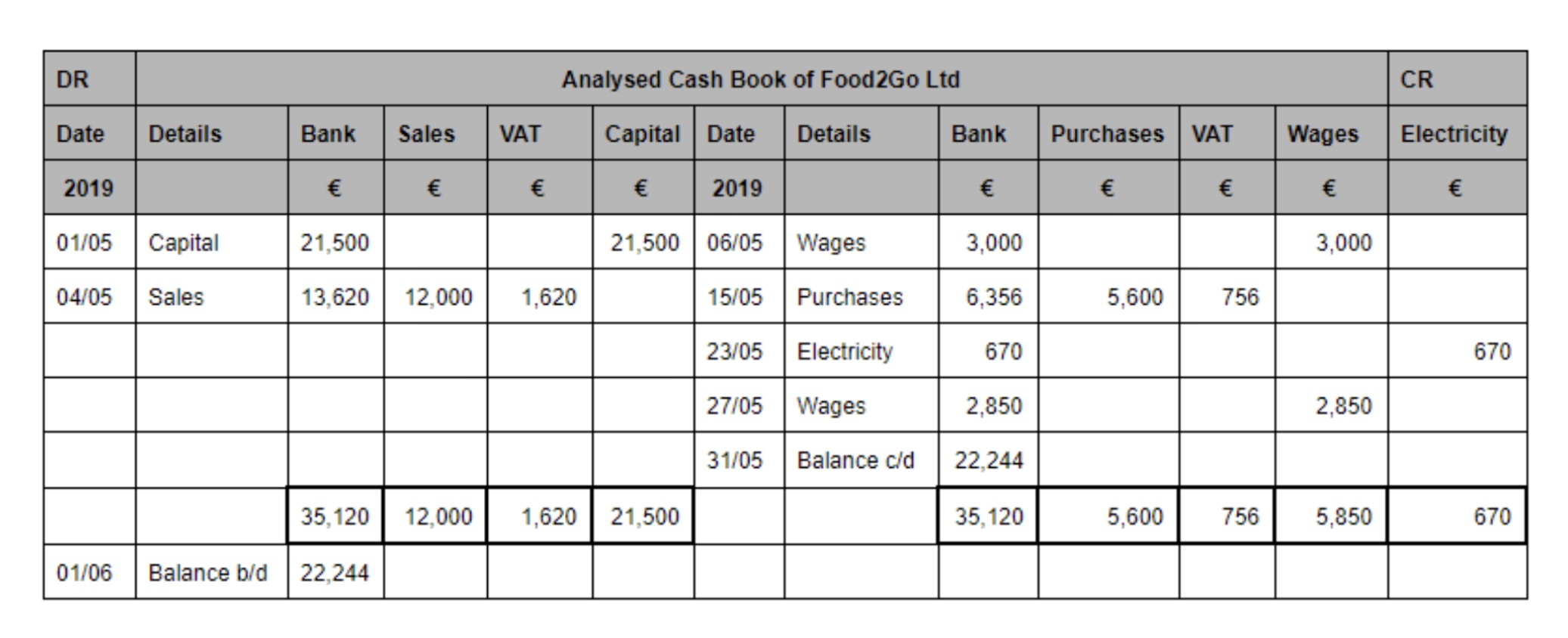

Analysed Cash Book and General Ledgers

Analysed Cash Book

An analysed cash book is used to record income and expenditure for a household or a business.

DR = Debit (income)

CR = Credit (expenditure)

Filling in an ACB

Put all the money coming in onto the debit side.

Put all the money going out onto the credit side.

Balance the amounts

How to Balance

Add up the total columns on both sides. Write the answer in your rough work space.

Subtract the smaller amount from the larger one.

Enter the difference on the smaller side with the title ‘balance c/d’ directly underneath the last entry on that side with the date of the last period e.g. 31/7

Show the totals on both sides on the same line. The first total should be the same (the bigger amount)

Enter the same balance for balance c/d underneath the totals on the opposite side, this time with the title ‘balance b/d’.

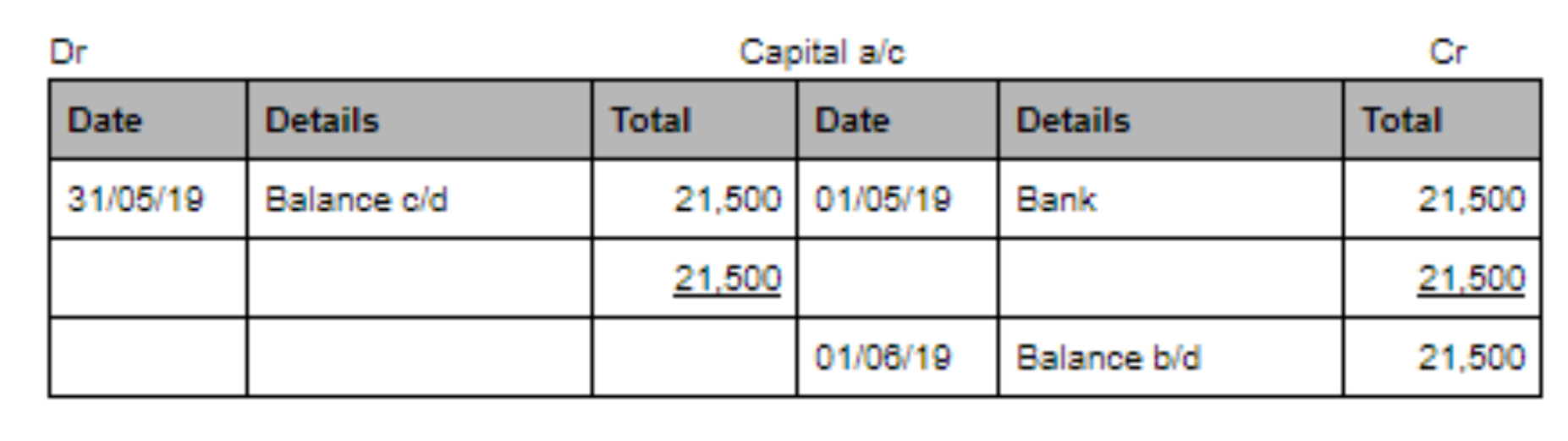

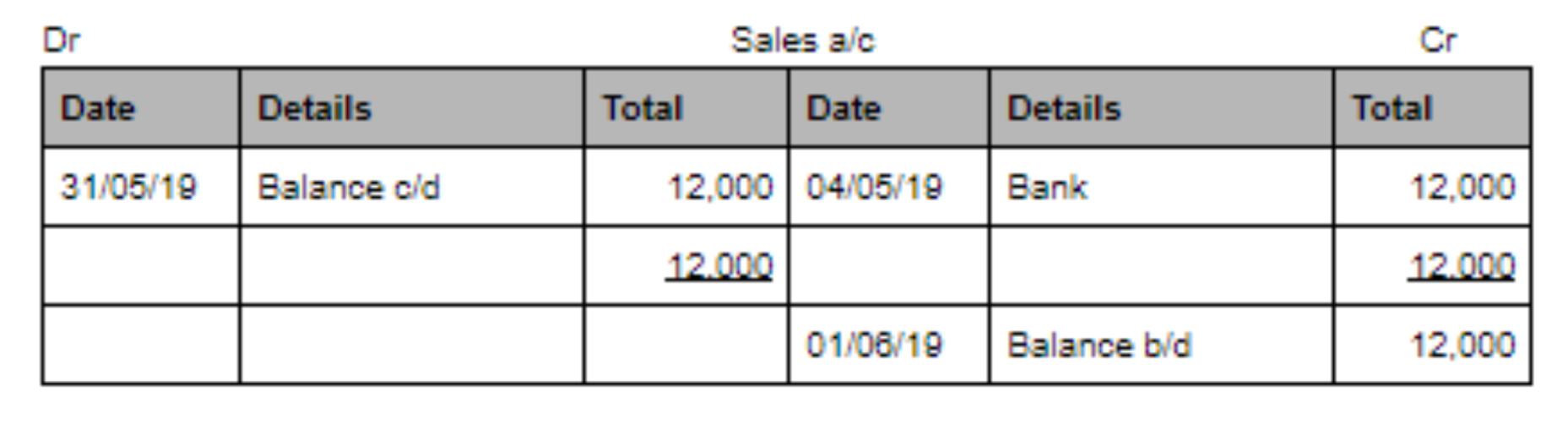

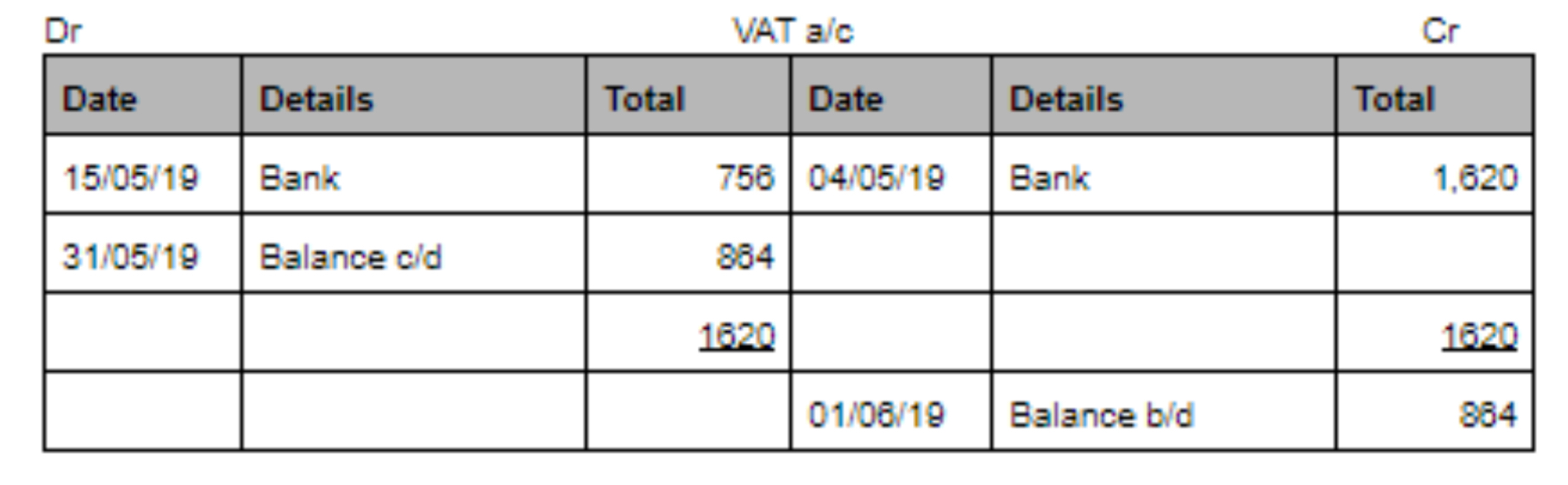

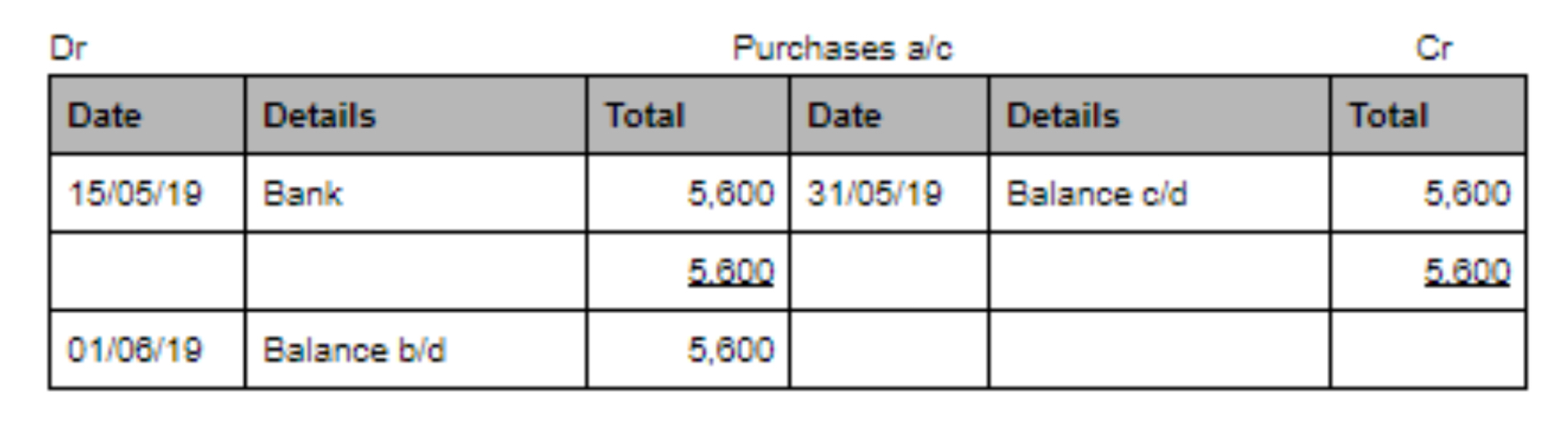

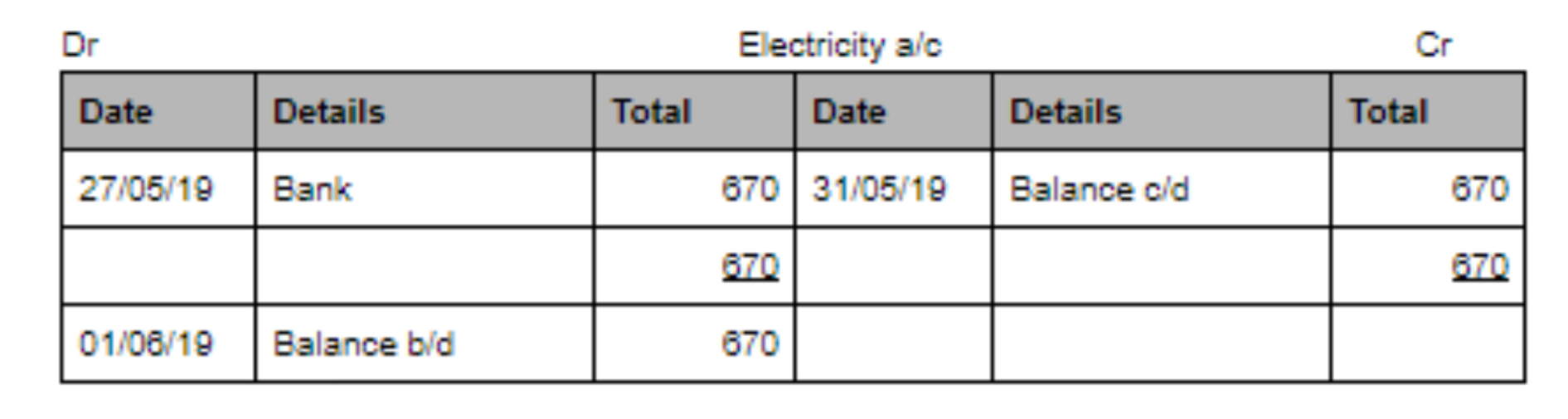

General Ledger

Ledgers are books that individual accounts are recorded in.

You balance the ledger the same way you balance an ACB

These accounts bring together:

- All transactions involving a particular person/business

- All transactions involving a particular type on income or expense.

Debit in ACB = Credit in Ledger

Credit in ACB = Debit in Ledger

Examples of general ledgers based on the ACB above.

Trial Balance