IB Business Management: Unit 3

3.1 Introduction to finance

Capital expenditure is the money spent to acquire fixed assets in a business. Due to their high initial cost, most fixed assets can be used as collateral (financial security pledged for repayment of a particular source of finance, such as bank loans). Capital expenditures are therefore long-term investments intended to assist businesses to succeed and grow.

Revenue expenditure is the money used in the day-to-day running of a business

3.2 Sources of Finance

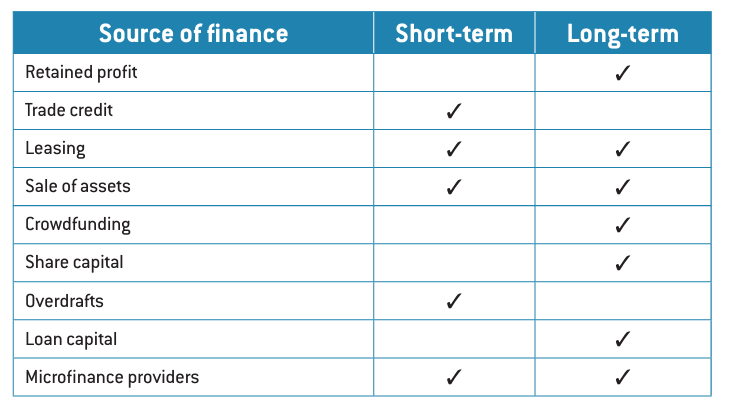

Internal sources of finance

Personal funds is a source of finance for sole traders that comes mostly from their own personal savings.

Advantages

The sole trader knows exactly how much money is available to run the business.

It provides the sole trader with much more control over the nances than other nance options. It also means that the sole trader does not need to pay the funds back or rely on outside investors or lenders, who could decide to withdraw their support at any time.

Disadvantages

It poses a large risk to the owners or sole traders because they could be investing their life’s savings, hence putting a strain on family or personal life.

If the savings are not sufficient it may prove difficult to start or maintain a business, especially if this is the only source of funding.

Retained profit is the profit that remains after a business (a profit-making entity) has paid out dividends to its shareholders. It is also known as ploughed-back profit. It is considered to be one of the most important long-term sources of finance for a business.

Advantages

It is cheap because it does not incur interest charges (like bank loans do).

It is a permanent source of finance as it does not have to be repaid.

It is flexible as it can be used in a way the business deems fit.

The owners have control over their retained profits without interference from other financial institutions such as banks.

Disadvantages

Start-up businesses will not have any retained profit as they are new ventures.

If retained profit is too low, it may not be sufficient for business growth or expansion.

A high retained profit may mean that either very little or nothing was paid out to shareholders as dividends. This could be less attractive to stock buyers than a similar profitable business that distributes dividends generously to its shareholders.

For non-profit businesses or entities, the money remaining at the end of a financial year is referred to as “retained surplus”.

Sale of assets is when a business sells off its unwanted or unused assets to raise funds.

Advantages

This is a good way of raising cash from capital that is tied up in assets which are not being used.

No interest or borrowing costs are incurred.

Disadvantages

This option is only available to established businesses as new businesses may lack excess assets to sell.

It can be time-consuming to find a buyer for the assets, especially for obsolete machinery.

In some cases, businesses adopt a sale and leaseback approach, which involves selling an asset that the business still needs to use. For example, the business can sell an asset to a specialist rm and then lease it back.

External sources of finance

Share capital is the money raised from the sale of shares of a limited company. It is also known as equity capital. The term authorized share capital is the maximum amount the shareholders of a company intend to raise.

Advantages

It is a permanent source of capital as it will not need to be redeemed (repaid by the business). If shareholders want to get their money back they have to find a buyer for their shares.

There are no interest payments and this relieves the business from additional expenses.

Disadvantages

Shareholders will expect to be paid dividends when the business makes a profit.

For public limited companies, the ownership of the company may be diluted or change hands from the original shareholders to new ones via the stock exchange.

Loan capital is the money sourced from financial institutions such as banks with interest charged on the loan to be repaid. It is also known as debt capital. A fixed interest rate is one that does not fluctuate and remains fixed for the entire term of the loan repayment. A variable interest rate changes periodically based on the prevailing market conditions.

Advantages

Loan capital is accessible and can be arranged quickly for a firm’s specific purpose.

Its repayment is spread out over a predetermined period of time, reducing the burden to the business of having to pay it in a lump sum.

Large organizations can negotiate for lower interest charges depending on the amount they want to borrow.

The owners still have full control of the business if no shares are issued to dilute their ownership.

Disadvantages

The capital will have to be redeemed even if the business is making a loss.

In some cases, collateral (security) will be required before any funds are lent.

Failure to repay the loan may lead to the seizure of a firm's assets.

If variable interest rates increase, a firm that has a variable rate loan may be faced with a high debt repayment burden.

Overdraft is when a lending institution allows a firm to withdraw more money than it currently has in its account. In most cases, the overdrawn amount is an agreed amount that has a limit placed on it. Interest is charged only on the amount overdrawn. It is also called overdrawing from the account.

Advantages

It provides an opportunity for rms to spend more money than they have in their account (even in situations where there is no money in the account), which greatly helps in settling short-term debts such as paying suppliers or wages for their staff.

It is a flexible form of nance as its demand will depend on the needs of the business at a particular point in time.

Charging interest only on the amount overdrawn can make it a cheaper option than loan capital.

Disadvantages

Banks can request for the overdraft to be paid back at very short notice.

Due to the variable nature of an overdraft, the bank can at times charge high interest rates.

Trade credit is an agreement between businesses that allow the buyer of the goods or services to pay the seller at a later date. The credit period offered by most creditors or suppliers (trade credit providers) usually lasts from 30 to 90 days; jewelry businesses are known to extend it to at least 180 days.

Advantages

By delaying payments to suppliers, businesses are left in a better cash flow position than if they paid cash immediately.

It is an interest-free means of raising funds for the length of the credit period.

Disadvantages

Debtors (trade credit receivers) lose out on the possibility of getting discounts had they purchased by paying cash.

Delaying payment to creditors or suppliers after the agreed period may lead to poor relations between the debtors and suppliers, with the latter refusing to engage in future transactions with the former.

Crowdfunding is when a business venture or project is funded by a large number of people each contributing a small amount of money.

Advantages

Crowdfunding provides access to thousands of investors who can see, interact with and share a project’s fundraising campaign.

It is a valuable form of marketing because pitching a project or business through the online platform can result in media attention that publicizes the business.

It provides an opportunity for feedback and expert guidance. By sharing the business idea, suggestions about how to improve it can be provided by a team of experts.

The business still maintains full control and won’t have to forfeit control when raising funds. It can decide how to structure the campaign, including how much to ask for, and then choose how to operate once it gets the funding.

It is a good alternative finance option as it provides another pathway for businesses that have struggled to get bank loans or traditional funding.

Disadvantages

Businesses seeking crowdfunding have strong competition. As crowdfunding is quite popular because of its advantages and accessibility, there are numerous projects on the major platforms at any given time. So businesses need a detailed plan of attack, and a clever way to differentiate themselves from their competitors.

The business is subject to thorough scrutiny and rejection. Having a solid idea does not mean it is going to be accepted by the crowdfunding platform of choice. Some popular platforms (like Kickstarter) have very detailed rules about what is allowed and what is not, and if all requirements are not met then the campaign might never be seen.

Fees need to be paid. Many crowdfunding platforms take a percentage of the contributions raised. The fees are usually minimal, but they still reduce the amount of money a project may otherwise get.

There is a potential risk of failure. If the crowdfunding campaign fails, it can be hard to recover. A failed crowdfunding campaign is a sign that the business plan is not good enough to the majority of investors. In addition, most crowdfunding platforms will not allow you to list the same project twice. Hence, the consequences of failure are severe.

Leasing is a source of finance that allows a firm to use an asset without having to purchase it with cash. Periodic or monthly leasing payments are made by agreement between the lessor and lessee. In some cases, businesses may get into a nance lease agreement, where at the end of the leasing period (which usually lasts for more than three years) they are given the option of purchasing the asset.

Advantages

A firm does not need to have a high initial capital outlay to purchase the asset.

The lessor takes on the responsibility of repair and maintenance of the asset.

Leasing is useful when particular assets are required only occasionally or for short periods of time.

Disadvantages

Leasing can turn out to be more expensive than the outright purchase of an asset due to the accumulated total costs of the leasing charges.

A leased asset cannot act as collateral for a business seeking a loan as an additional source of finance.

Microfinance providers are institutions that provide banking services to low income or unemployed individuals or groups who would otherwise have no other access to financial services. Microfinance services include microcredit, which is the provision of small loans to poor clients; microinsurance; and savings and current accounts (also known as checking accounts), among other services.

Advantages

Most microfinance institutions do not seek any collateral for providing financial credit.

They provide or disburse loans quickly and with less formalities to individuals, groups or small businesses, so they can meet any financial emergency.

They have an extensive portfolio of loans, including working capital loans, housing loans, etc.

They promote self-sufficiency and entrepreneurship. They do this by providing funds to individuals to set up a business that may need minimal investment but will provide a sustainable profit.

Disadvantages

Microfinance institutions can adopt harsh recovery methods in the event of a default if the customer does not have legal representation.

They offer smaller loan amounts or financial capital than other financial institutions that provide much larger amounts.

The interest rates on their loans are high and they find it difficult to offer lower rates. This is partly because they do not operate in the same way as traditional banks that nd it easy to accumulate funds. In addition, they borrow money from these banks in order to execute their functions. Hence, their operating cost per transaction is quite high despite the large volume of transactions every day.

Business angels are highly affluent individuals who provide financial capital to small start-ups or entrepreneurs in return for ownership equity in their businesses. They are also known as angel investors.

Advantages

Business angels are more open to negotiation than other institutions or lenders to small or start-up businesses. This is because they are usually successful entrepreneurs who understand the amount of risk involved with establishing a business. Their flexibility and risk-taking attitude make them one of the best sources of nance in this situation.

No repayment or interest is required. Angel investors fund the business and in exchange get an ownership stake in the business. If the business succeeds, both the business and angel investor benet; if not, the angel does not get paid back.

They offer valuable knowledge and they focus on helping a business succeed by using their extensive business experience coupled with good financial capital.

Disadvantages

Business angels may assume a large degree of control or ownership in the businesses they invest in, therefore diluting the ownership of the entrepreneur.

They may expect a substantial return on their investment within the first few years, sometimes equal to 10 times their original investment. This can create additional pressure on the business.

Short-term and Long-term finance

Short-term finance

This is money needed for the day-to-day running of a business and therefore provides the required working capital. External short-term financing is usually expected to be paid back within 12 months or less. Examples of short-term finance include bank overdrafts, short-term loans and trade credit.

Long-term finance

This is funding obtained for the purpose of purchasing long-term fixed assets or other expansion requirements of a business. It is normally used for the overall improvement of the business. Businesses that take up external long-term financing usually have a time span of more than one financial year to pay it back. Long-term finance sources include long-term bank loans and share capital.

Factors influencing the choice of a source of finance

Purpose or use of funds: Long-term loan capital may be appropriate when purchasing a fixed asset, while trade credit may be suitable if raw materials are needed urgently for the business.

Cost: The opportunity cost (the lost benet that would have been derived from an alternative) is an important consideration when deciding on the most appropriate source of finance.

Status and size

Amount required

Flexibility

Status of the external environment

Gearing: This refers to the relationship between share capital and loan capital. If a company has a large proportion of loan capital to share capital it is said to be high geared, while a company that is low geared has a smaller proportion of loan capital to share capital. High-geared businesses are viewed as risky by financial institutions, and they will be reluctant to lend money to such rms. These businesses will therefore need to seek alternative sources of finance. One way of measuring gearing is by calculating the gearing ratio.

3.3 Costs and Revenues

Cost is an expenditure or amount paid to produce or sell a good or service, including the acquisition of business resources.

Revenue is income earned or money generated from the sale of goods or services.

Profit is calculated by subtracting costs from revenue. A high positive difference (where revenue is higher than costs) is a good indicator of business success.

Types of costs

Fixed costs are costs that do not change with the amount of goods or services produced. They remain fixed in the short run. The short run is defined as a period of time when at least one factor of production (resource needed to produce goods or services) does not change.

Variable costs are costs that change with the number of goods or services produced.

Direct costs are costs that can be identified with the production of specific goods or services.

Indirect costs are costs that are not clearly identified with the production of specific goods or services. They are also known as overheads or overhead costs.

In most cases, indirect costs are fixed costs while direct costs are variable costs. However, both indirect and direct costs can be either fixed or variable depending on the specific nature of the business activity.

total revenue = price per unit × quantity sold

Revenue is a measure of the money generated from the sale of goods and services.

Total revenue is the total amount of money a firm receives from the sale of goods or services, found by multiplying the price per unit by the number of units sold. It is also known as sales revenue or sales turnover.

A firm's revenue is obtained not only from its trading activities. Other revenue streams include the following:

Rental income

Sale of fixed assets

Dividends

Interest on deposits

Donations

As a contribution tool, absorption costing aids in business decision-making by providing a platform where various cost situations are analyzed and evaluated. Absorption costing (also called full costing) is a managerial accounting method that captures all costs associated with producing a given product.The direct and indirect costs, including direct materials, direct labor, rent, and insurance, are accounted for using this method.

Descriptive statistics involve the use of statistical data and help to present large amounts of data in simplified and manageable forms.

3.4 Final Accounts

Final accounts are financial statements compiled by businesses at the end of a particular accounting period, such as at the end of a fiscal or trading year. These records of accounts – including transactions, revenues, and expenses – help to inform internal and external stakeholders about the financial position and performance of an organization. The purpose of accounts to each of these stakeholders is explored below.

Shareholders

Shareholders are interested in knowing how valuable the business has become throughout its financial year. They are keen to establish how profitable the business is in order to assess the safety of their investment. They check on how efficiently the business is investing capital in an attempt to make a worthwhile return on their investment. The performance of the directors is also of interest to them: shareholders want to see whether the directors need to be motivated further or replaced.

Managers

Final accounts are used by managers to set targets, which they can use to judge and compare their performance within a particular financial year or number of years. These will help them in setting budgets, which will then help in monitoring and controlling expenditure patterns in various departments. Knowing the financial records will therefore greatly assist managers in strategic planning for more effective decision-making in the businesses.

Employees

A profitable business could signal to employees that their jobs are secure. This may also indicate that they could get pay rises. The potential for business growth could help to strengthen these two aspects of job security and salary increases. However, an increase in profitability does not necessarily lead to pay increases for employees, leading them to involve trade unions to negotiate further on their behalf.

Customers

Customers are interested in knowing whether there will be a constant supply of a firm's products in the future. This will determine how dependent they should be on the business. If a rm lacks security, perhaps due to low profitability, customers will go elsewhere where supply is reliable and guaranteed.

Suppliers

Suppliers can use final accounts to negotiate better cash or credit terms with rms. They can either extend the trade credit period or demand immediate cash payments. The security of the business and thus its ability to pay off its debts will be a key concern for suppliers.

The government

The government and tax authorities will check on whether the business is abiding by the law regarding accounting regulations. They will be interested in the profitability of the business to see how much tax it pays. A loss making business will be of grave concern to the government because it could mean an increase in unemployment, which could be detrimental to a country’s economy.

Competitors

Businesses will want to compare their financial statements with those of other firms to see how well they are performing financially. They will look for the answers to key questions such as:

Are their competitors’ profitability levels higher than theirs or are the competitors struggling financially?

How do the competitors’ sales revenues compare with theirs?

Financiers

These include banks who check on the creditworthiness of the business to establish how much money they can lend it. This will also depend on the gearing of the business, because a high-geared business will have problems soliciting funding from financial institutions. Banks will thoroughly assess the accounts of a business in order to be confident that it will be able to pay back its loan with interest.

The local community

Residents living around a particular business will want to know its profitability and expansion potential. This is because it may create job opportunities for them and lead to growth in the community. However, the residents will also be concerned about whether the business will be environmentally friendly and whether its accounts consider costs for minimizing air or noise pollution.

The main finals accounts

The profit and loss account

This is also known as the income statement and shows the records of income and expenditure flows of a business over a given time period. It therefore establishes whether a business has made a profit or a loss and how this was distributed at the end of that period. It is divided into three parts: the trading account, the profit and loss account, and the appropriation account

The trading account

The trading account shows the difference between the sales revenue and the cost to the business of those sales. It is shown as the top part of the income statement that establishes the gross profit of the business. In calculating gross profit, the following formula is used: gross profit = sales revenue − cost of sales

Sales revenue is the income earned from selling goods or services over a given period. Cost of sales or cost of goods sold (COGS) is the direct cost of producing or purchasing the goods that were sold during that period. The formula for cost of sales is as follows: cost of sales = opening stock + purchases − closing stock

Profit and loss account is also known as the income statement, this is the record of income and expenditure flows of a business over a given time period

Cost of sales is the direct cost of producing or purchasing the goods that were sold during that period

The profit and loss account

This is the second part of the income statement that shows the profit before interest and tax, profit before tax, and profit for period. To find out profit before interest and tax, expenses are subtracted from the gross profit shown in the trading account. These expenses comprise indirect costs or overheads which are not directly linked to the units sold. Examples include advertising costs, administration charges, rent, and insurance costs. Therefore: profit before interest and tax = gross profit expenses

Profit before tax is calculated by subtracting interest payable on loans from the profit before interest and tax: profit before tax = profit before interest and tax interest

Then, the profit for period is found by deducting corporation tax (tax on company profits) from profit before tax: profit for period = profit before tax corporation tax The appropriation account This is the final part of the profit and loss account that shows how the company’s profit for period is distributed. This distribution is in two forms: either as dividends to shareholders or as retained profit (ploughed-back profit).

Retained profit is calculated using the following formula: retained profit = profit for period dividends.

Balance sheet is a financial statement that outlines the assets, liabilities and equity of a firm at a specific point in time

Assets are resources of value that a business owns or that are owed to it

Liabilities are a firm’s legal debts or what it owes to other rms, institutions or individuals

The balance sheet

Also known as the statement of financial position, this outlines the assets, liabilities, and equity of a firm at a specific point in time. It is a snapshot of the financial position of a firm and is used to calculate a firm's net worth. It gives the firm an idea of what it owns and owes, including how much shareholders have invested in it. The basic requirement of a balance sheet is that what a business owns (total assets) must equal what it owes (total liabilities) plus how the assets are financed (equity). This is what makes the balance sheet balance.

Assets

These are resources of value that a business owns or that are owed to it. They include fixed assets and current assets. Non-current assets, also called fixed assets, are long-term assets that last in a business for more than 12 months. Tangible examples that are physical in nature include buildings, equipment, vehicles, and machinery. Some of these assets, such as machinery, usually depreciate (lose value) over time. In this case, the accumulated depreciation is deducted from the non-current asset. Intangible assets that are non-physical in nature tend to be difficult to value. Current assets are short-term assets that last in a business for up to 12 months. They include cash, debtors, and stock.

Cash is money received from the sale of goods and services, which could be held either at the bank or by the business.

Debtors are individuals or other firms that have bought goods on credit and owe the business money.

Stock, also known as inventory, includes raw materials, semi-finished goods, and finished goods. total assets = non-current assets + current assets

Liabilities

These are a firm's legal debts or what it owes to other firms, institutions, or individuals. They arise during the course of business operation and are usually a source of funding for the firm. They are classified into noncurrent liabilities and current liabilities. Non-current liabilities, also known as long-term liabilities, are long-term debts or borrowings payable after 12 months by the business. They include long-term bank loans and mortgages. Current liabilities are short-term debts that are payable by the business within 12 months. These include creditors (unpaid suppliers who sold goods on credit to the firm), a bank overdraft and tax (money owed to the government, such as corporation tax).

total liabilities = current liabilities + non-current liabilities

To work out net assets, total liabilities is subtracted from total assets: net assets = total assets − total liabilities

Equity

This refers to the amount of money that would be returned to a business if all of the assets were liquidated. Liquidation is a situation where all of a firm's assets are sold off to pay any funds owing. For profit-making entities there are two aspects to equity: share capital and retained earnings. However, for non-profit entities there is only one aspect of equity (retained earnings).

Share capital

This refers to the original capital invested into the business through shares bought by shareholders. It is a permanent source of capital and does not include the daily buying and selling of shares in a stock exchange market or the current market value of shares.

Retained earnings

This includes all current and prior period retained profits (prot-making entities) or retained surpluses (non-profit entities). Hence, for profit-making businesses, equity is the combination of share capital and retained earnings: equity = share capital + retained earnings

For non-profit-making businesses, equity is equal to retained earnings: equity = retained earnings In both profit-making and nonprofit entities, equity helps to finance the net assets of the business and enables the balance sheet to balance: net assets = equity

Intangible assets are assets that are non-physical in nature.

Patents provide inventors with the exclusive rights to manufacture, use, sell or control the product or process they invented.

Goodwill the value of positive or favorable attributes that relate to a business. Goodwill usually arises when one rm is purchased by another. During an acquisition, goodwill is valued as the amount paid by the purchasing rm over and above the book value of the rm being bought.

Copyright laws legislation that provides creators with the exclusive right to protect the production and sale of their artistic or literary work.

Trademark a recognizable symbol,word, phrase or design that is officially registered and that identifies a product or business.

Intangible assets are difficult to value due to their subjective nature, and in many cases they will not be shown in the balance sheet. Their value can fluctuate over time and simple changes in the reputation of an organization can either inflate or deflate a firm's value. As a result, intangible assets can be used to “window dress” or artificially increase the value of a firm just before a purchase. The setting of specific parameters to be used to quantify an intangible asset just serves to increase the complexity and inaccuracy of including it in the balance sheet.

Depreciation

This is the decrease in the value of a non-current asset over time. It is a non-cash expense that is recorded in the profit and loss account in order to determine the profit before interest and tax. Two reasons why assets depreciate are:

Wear and tear – the repeated use of non-current assets such as cars or machinery causes them to fall in value and more money is needed to maintain them.

Obsolescence – existing non-current assets fall in value when new or improved versions are introduced in the market. With time these “old” assets become obsolete or out of date and are eventually withdrawn.

Straight-line method

This is a commonly used method that spreads out the cost of an asset equally over its lifetime by deducting a given constant amount of depreciation of the asset’s value each year. It requires the following elements in its calculation:

The expected useful life of the asset, which is the length of time it intends to be used before replacement.

The original cost of the asset, which is its purchase or historical cost.

The residual, scrap or salvage value of the asset, which is an estimation of its worth or value over its useful life.

annual depreciation = original cost − residual value / expected useful life of asset

Residual value is an estimation of an asset’s worth or value over its useful life, also known as scrap or salvage value.

Advantages of using straight-line depreciation

It is simple to calculate as it is a predictable expense that is spread over a number of years.

It is most suitable for less expensive items, such as furniture, that can be written off within the asset’s estimated useful life.

Disadvantages of using straight-line depreciation

It is not suitable for expensive assets such as plants and machinery, as it does not cater for the loss in efficiency or increase in repair expenses over the useful life of the asset.

It can inflate the value of some assets which may have lost the greatest amount of value in their first or second years (e.g. motor vehicles).

It does not take into account the fast-changing technological environment that may render certain fixed assets obsolete very quickly.

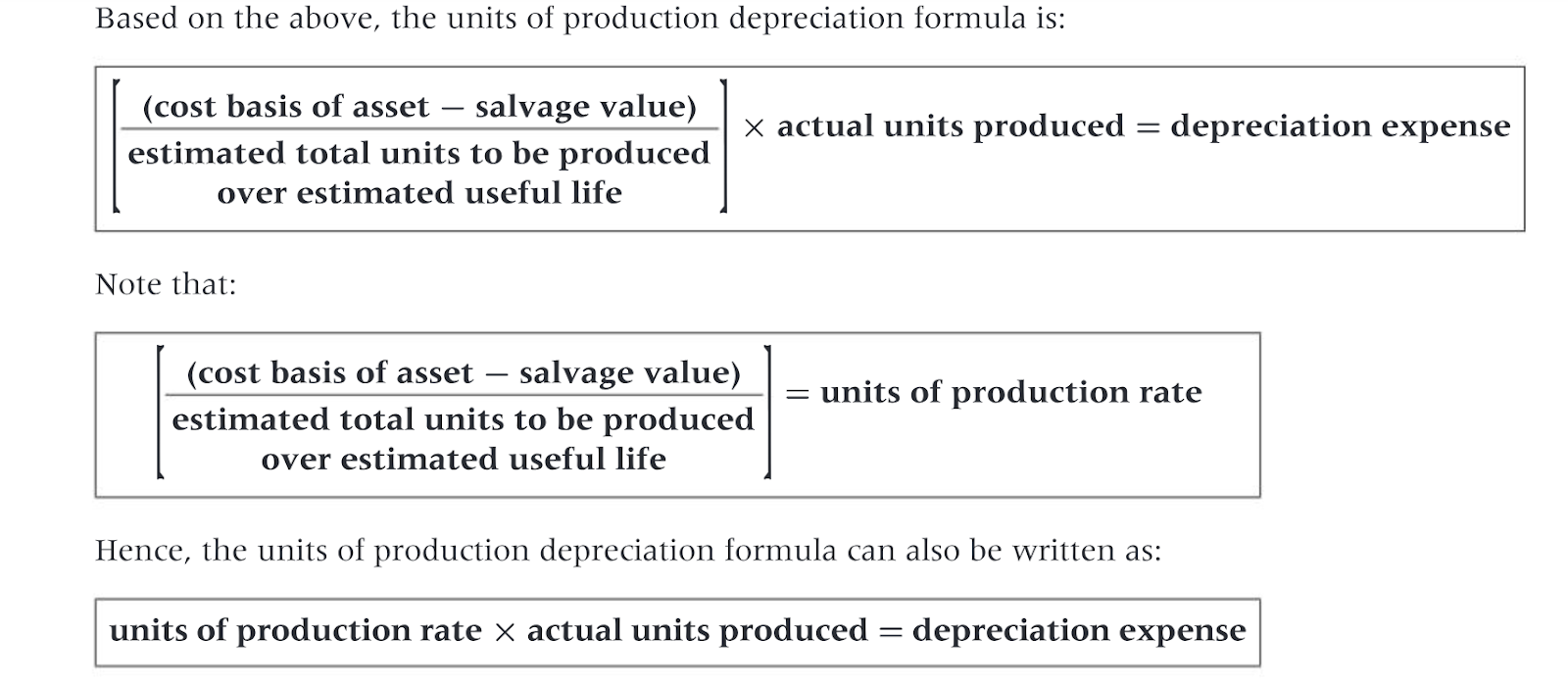

Units of production method

Also called the units of activity method, this depreciation method calculates the depreciation of the value of an asset based on usage. It assumes that an asset’s useful life is more closely related to its usage than just the passage of time. In this method, depreciation will be higher when there is a greater volume of activity during the year when an asset is used a lot, and lower during times when an asset is used less. The following information is required to calculate depreciation using the units of production method:

The cost basis of the asset. The cost basis of a non-current asset is the total amount paid to acquire the asset for use in the business. This is the original value of the asset.

The salvage value of the asset. This is the estimated value of the asset if it were to be sold at the end of its useful life.

The estimated total number of units to be produced. The wear and tear on the machinery is the result of the number of units it is expected to produce over its useful life. This figure is usually based on production estimates and historical information.

Estimated useful life. This is the length of time an asset is expected to be used before it wears out and needs to be replaced.

Actual units produced. The number of units the asset produced during the current year. Based on the above, the units of production depreciation formula is:

Advantages of using units of production depreciation

As the depreciation expense is directly tied to the wear and tear on the asset, this method writes down an asset based on its usage as opposed to time. This is a more accurate reflection of the declining physical value of the asset.

It accurately matches revenues and expenses. As this method is based on asset usage, it is important to note that the expenses fluctuate with customer demand. This allows revenues generated to be matched to expenses when producing financial statements, hence providing a more realistic view of what is taking place in the business.

Disadvantages of using units of production depreciation

It is only useful to manufacturers or producers. It makes little sense to tie depreciation to asset usage if a business does not manufacture or produce a product.

This method is not allowed for tax purposes. It cannot be used when a business computes its tax returns at the end of the year.

It can be complicated to compute the units of depreciation. Also, measuring output can be tricky and depreciation expense must be recalculated each period.

3.6 Debt/equity ratio analysis

Efficiency Ratios

These ratios assess how well a rm internally utilizes its assets and liabilities. They also help to analyze the performance of a firm.

Stock turnover ratio

This ratio measures how quickly a firm's stock is sold and replaced over a given period. It considers the number of times stock is sold and replenished. It can be calculated using two approaches. One approach looks at how many times in a given period (usually a year) a firm sells its stock. The formula is:

stock turnover ratio (number of times) = cost of sales / average stock

average stock = (opening stock + closing stock) / 2

Another approach in calculating stock turnover is to consider the number of days it takes to sell the stock. The following formula can be used:

stock turnover ratio (number of days) = (average stock / cost of goods sold) × 365

A higher stock turnover in terms of number of times is preferred by a business – or a lower stock turnover ratio (in number of days). In considering the first approach to stock turnover (number of times), a high stock turnover ratio means that the firm sells stock quickly, thereby earning more profit from its sales. This also means that goods do not become obsolete quickly and perishable goods do not expire, showing that the firm has good control over its purchasing decisions. Stock turnover ratio is a good instrument for assessing the effectiveness of working capital management. Working capital management is an assessment of the way the current assets and current liabilities are being administered. Generally, the faster a business turns over its stock, the better. However, it is important that this is done profitably, rather than selling stock at low gross profit margins or, worse still, at a loss.

Possible strategies to improve stock turnover ratio

Slow-moving or obsolete goods should be disposed of. This will help reduce the firm's level of stock. The downside is that it could lead to losses due to the lost sales revenue that these goods could have generated.

Firms with a wide range of products may need to offer a narrower, better-selling range of products. The disadvantage is that this may minimize the variety of products offered to consumers.

Keeping low levels of stock has the added benefit of reducing the costs of holding stock. However, during sudden increases in demand for goods by customers, businesses with low levels of stock may not have sufficient amounts to sustain the market.

Some firms are able to adopt the just-in-time (JIT) production method, where stocks of raw materials are ordered only when they are needed. The major drawback is that if there are any delays in the delivery of the raw materials to producers then it could negatively affect production and eventually sales.

Debtor days

This ratio measures the number of days it takes on average for a firm to collect its debts from customers it has sold goods to on credit. These customers who owe the business money are known as debtors, and the ratio is also referred to as the debt collection period. It assesses how efficient a business is in its credit control systems. It is calculated using the following formula:

debtor days ratio (number of days) = (debtors total / sales revenue) × 365

Possible strategies to improve debtor days ratio

A firm can provide discounts or other incentives to encourage debtors to pay their debts earlier. The drawback here is that the business receives less income from these customers than was originally agreed.

A firm could impose stiff penalties, such as nes for late payers. However, the firm might lose long-time loyal customers.

A firm could stop any further transactions with overdue debtors until payment is finalized. This still does not guarantee payment though, and some debtors may opt to seek alternative suppliers for their goods.

A business can resort to legal means, such as court action for consistently late payers. This may harm the reputation that a business has with its customers.

Creditor days

This ratio measures the average number of days a rm takes to pay its creditors. It assesses how quickly a firm is able to pay its suppliers. The ratio is calculated using the following formula: creditor days ratio (number of days) = creditors / cost of sales × 365

Possible strategies to improve creditor days ratio

Having good relationships with creditors such as suppliers may enable a firm to negotiate for an extended credit period. However, some suppliers could object to the extension and refuse to support the business in the future (when it might be in dire need of assistance).

Effective credit control will improve the creditor days ratio. Managers will need to assess the risks of paying creditors early versus how long they should delay in making their payment. This may not be an easy task and will depend on the cash flow position and needs of the business at that time.

Gearing ratio

This measures the extent to which the capital employed by a firm is financed from loan capital. Loan capital is a non-current liability in the business, while capital employed includes loan capital, share capital and retained profits. The commonly used gearing ratio formula is: gearing ratio = loan capital / capital employed × 100

Possible strategies to improve the gearing ratio

Businesses that are very highly geared can find themselves in a difficult financial position. This ratio could be reduced using the following measures:

A business can seek alternative sources of funding that are not “loan related”, for example issuing more shares. The drawbacks are that it may take a long time to issue shares and it may go against the objective of any existing shareholders who do not want to lose ownership of the business.

A firm could decide not to issue dividends to shareholders so as to increase the amount of retained profit. But this may lead to resentment among shareholders, especially if the reasons for doing so are not well explained.

Insolvency and bankruptcy (HL)

Insolvency is a financial state where a person or rm cannot meet their debt payments on time. The person or rm no longer has the money to pay off their debt obligations, and their debts exceed their assets. Naturally, people or firms that become insolvent will take certain steps towards a resolution. One of the most common solutions for insolvency is declaring bankruptcy. Bankruptcy is a legal process that happens when a person or rm declares that they can no longer pay back their debts to creditors. It is a legal process for liquidating the property and assets a debtor owns in order to pay off their debts. This process can provide protection and relief for people or rms that are unable to pay off their debts.

3.7 Cash Flow

Cash is money that a business obtains through either the sale of its goods or services, borrowing from financial institutions, or investment by shareholders. It is the most liquid asset in a business and is placed under current assets in the balance sheet. This cash is essential to the smooth running of any business and a lack of it could result in business failure or bankruptcy. Cash flow is the money that flows in and out of a business over a given period of time. Cash inflows are the monies received by a business over a period of time, while cash outflows are the monies paid out by a business over a period of time. Cash flow is a key indicator of a firm’s ability to meet its financial obligations. A positive cash flow (where cash inflows exceed cash outflows) will enable businesses to meet their day-to-day running costs.

Cash flow forecasts

These are future predictions of a firm's cash inflows and cash outflows over a given period of time. The forecast is a financial document that shows the expected month-by-month receipts and payments of a business that have not yet occurred. Examples of likely cash inflows include cash sales from selling goods or business assets, payments from debtors, cash investments from shareholders, and borrowing from banks. Cash outflows include purchasing materials or fixed assets for cash; cash expenses such as rent, wages and salaries; paying creditors; repaying loan; and making dividend payments to shareholders.

Constructing cash flow forecasts

In constructing a cash ow forecast, it is important to know the following terms:

Opening cash balance – this is the cash that a business starts with every month. It is also the cash held by a business at the start of a trading year.

Total cash inflows – this is a summation of all cash inflows during a particular month.

Total cash outflows – this is a summation of all cash outflows during a particular month.

Net cash flow – this is the difference between the total cash inflows and the total cash outflows.

Closing cash balance – this is the estimated cash available at the end of the month. It is found by adding the net cash flow of one month to the opening balance of the same month.

Benefits of cash flow forecasts

A cash flow forecast is a useful planning document for anyone wishing to start a business. This is because it helps to clarify the purpose of the business and provides estimated projections for future performance.

Cash flow forecasts provide a good support base for businesses intending to apply for funding from financial institutions. This is because they enable the banks to check on the businesses’ solvency and creditworthiness.

Predicting cash flow can help managers identify in advance periods when the business may need cash, and therefore plan accordingly to source it.

A cash flow forecast can help with monitoring and managing cash flow. By making comparisons between the estimated cash flow figures and its actual figures, a business should be able to assess where the problem lies and seek the respective solutions to solve it.

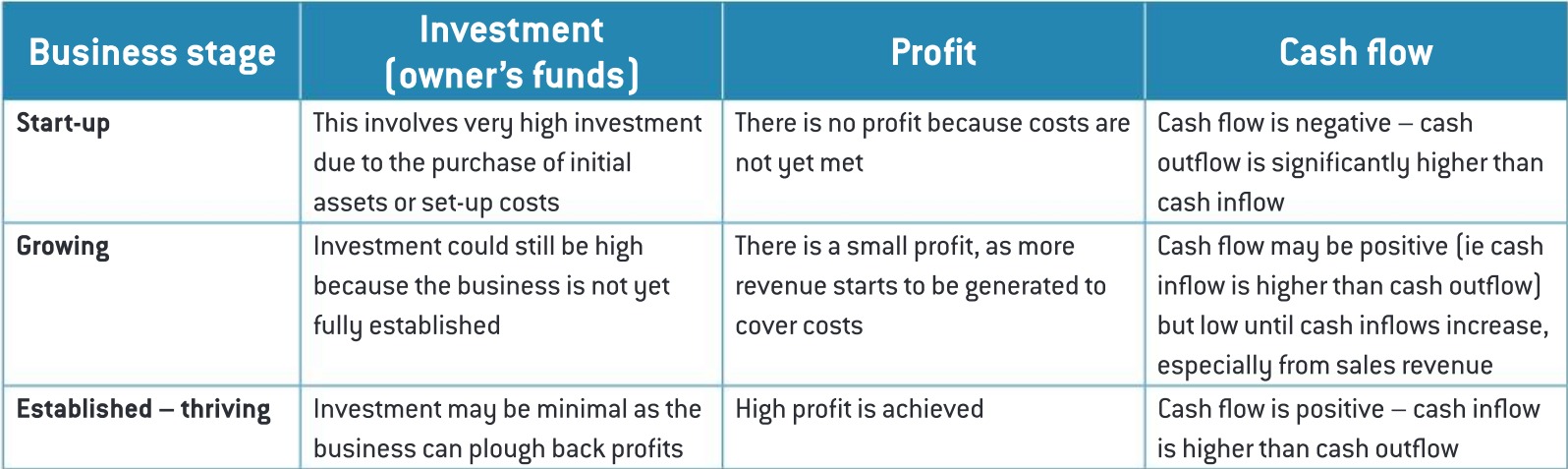

The relationship between investment, profit, and cash flow

Investment generally refers to the act or state of investing. In finance or business, investing is spending money on purchasing an asset with the expectation of future earnings. Investing involves wealth creation, including hoping that the bought asset appreciates in value over time. Examples of financial investments include buying bonds, stocks, or property. All forms of investment come with risks, especially risks brought about by unexpected changes in the market conditions in an economy.

Reducing cash outflows

The following methods aim to decrease the amount of cash leaving a business:

A business can negotiate with suppliers or creditors to delay payment. This helps it to have working capital for its short-term needs. The drawbacks with this are that negotiations may be time-consuming, and delaying payment to suppliers could affect future relationships – suppliers may refuse to supply in the future.

Purchases of fixed assets can be delayed. Assets such as machinery and equipment may take up a lot of the business’s cash, and delaying purchases of them helps to avail cash in the business. However, if the machines or equipment are becoming obsolete or outdated, delaying the purchase of replacements may lead to decreased efficiency and higher costs in the long term.

A business can decrease specific expenses that will not affect production capacity, such as advertising costs. If not well checked, though, this may reduce future demand for a business’s products.

A business could look into sourcing cheaper suppliers. This will help to reduce costs for materials or essential stock, decreasing the outflow of funds. A possible danger of this is that the quality of the finished product may be compromised, affecting future customer relationships.

Improving cash inflows

A business can insist that customers pay with cash only when buying goods. This avoids the problem of delayed payments from debtors, which ties up cash. The disadvantage is that the business may lose customers who prefer to buy goods on credit.

Offering discounts or incentives can encourage debtors to pay early. This will reduce the debt burden on debtors as they will pay less than earlier agreed. The limitation here is that, after the discount, businesses will receive less cash than previously expected.

A firm may diversify its product offering. This will help to increase the variety of goods on offer to customers, potentially increasing sales. It is worth remembering that diversification comes with higher costs and with no clear guarantee of sales.

Looking for additional finance sources

Sale of assets

Arranging a bank overdraft

Sale and leaseback

Limitations of cash flow predictions

Unexpected changes in the economy

Poor market research

Difficulty in predicting competitors’ behavior

Unforeseen machine or equipment failure

Demotivated employees

3.8 Investment Appraisal

Investment appraisal refers to the quantitative techniques used in evaluating the viability or attractiveness of an investment proposal.

Payback period is the length of time required for an investment project to pay back its initial cost outlay.

payback period = initial investment cost / annual cash flow from investment

(extra cash inflow / required annual cash flow in year #) × 12 months

Advantages of payback period

It is simple and fast to calculate.

It is a useful method in rapidly changing industries such as technology. It helps to estimate how fast the initial investment will be recovered before another machine, for example, can be purchased.

It helps firms with cash flow problems because they can choose the investment projects that can pay back more quickly than others.

Since it is a short-term measure of quick returns on investment, it is less prone to the inaccuracies of long-term forecasting.

Business managers can easily understand and use the results obtained.

Disadvantages of payback period

It does not consider the cash earned after the payback period, which could influence major investment decisions.

It ignores the overall profitability of an investment project by focusing only on how fast it will pay back.

The annual cash flows could be affected by unexpected external changes in demand, which could negatively affect the payback period.

Average rate of return

This method measures the annual net return on an investment as a percentage of its capital cost. It assesses the profitability per annum generated by a project over a period of time.

Advantages of average rate of return

It shows the profitability of an investment project over a given period of time.

Unlike the payback period, it makes use of all the cash flows in a business.

It allows for easy comparisons with other competing projects for better allocation of investment funds.

A business can use its own criterion rate and check this with the ARR for a project to assess the viability of the venture.

Disadvantages of average rate of return

Since it considers a longer time period or useful life of the project, there are likely to be forecasting errors. Long-term forecasts reduce the accuracy of results.

It does not consider the timing of cash inflows. Two projects might have the same ARR but one could pay back more quickly compared to the other due to faster cash inflows.

The effects on the time value of money are not considered.

Net Present Value (HL)

This is defined as the difference in the summation of present values of future cash inflows or returns and the original cost of investment. Present value is today’s value of an amount of money available in the future. The discounted cash flow method is a technique that considers how interest rates affect the present value of future cash flows. It uses a discount factor that converts these future cash flows to their present value today. This discount factor is usually calculated using interest rates and time.

NPV = total present values – original cost

Advantages of net present value

The opportunity cost and time value of money is put into consideration in its calculation.

All cash flows, including their timing, are included in its computation.

The discount rate can be changed to suit any expected changes in economic variables, such as interest rate variations.

Disadvantages of net present value

It is more complicated to calculate than the payback period or ARR.

It can only be used to compare investment projects with the same initial cost outlay.

The discount rate greatly influences the final NPV result obtained, which may be affected by inaccurate interest rate predictions.

The BCG Matrix

The BCG matrix is a planning and decision-making tool that uses graphical representations of a firm's goods or services in order to help the firm to decide what to keep, sell or invest more in. The BCG matrix works on the premise that every business should have a portfolio containing both high growth products requiring cash investment and low-growth products that provide extra cash. Having both types of products can ensure long-term business success. The BCG is important in financial decision-making because:

It provides a high-level overview for the finance department to see the opportunities that each product in the organization’s product portfolio presents.

It enables the finance department to think of ways to allocate its financial resources to the organization’s product portfolio so that profits are maximized over the long term.

The finance department can see the extent to which the organization’s product portfolio is balanced. For example, an organization with very few products in its portfolio could be in a risky position if competition increases for similar products. This will have financial implications for the business.

It is very simple to use and can be used across the other business departments, providing a chance to collaborate and compare department outcomes.

3.9 BudgetsA budget is a quantitative financial plan that estimates revenue and expenditure over a specified future time period. Budgets can be prepared for individuals, for governments, or for any type of organization. Budgets help in setting targets and are aligned with the main objectives of the organization. They enable the efficient allocation of resources within the specified time period. The person involved in the formulation and achievement of a budget is known as the budget holder. The budget holder is responsible for ensuring that the specified budget allocations are being met. Commonly used budgets are sales revenue budgets and cost budgets. Budgetary Control = modalities taken that ensure the budgeted performance is in like with the actual performance. To be able to account for the revenues generated and costs incurred, different parts of a business are divided into cost centers or profit centers

Cost centers

Cost centers can help managers to collect and use cost data effectively. Examples of costs collected and recorded in these sections include electricity, wages, advertising, and insurance, among other costs. Businesses can be divided into cost centers in some of the following ways:

By department

By product

By geographical location

Profit centers

This is a part or section of a business where both costs and revenues are identified and recorded. These sections allow businesses to calculate how much profit each center makes. Prot centers enable comparisons to be made so as to judge the performance in the various sections of the business. Just like cost centers, profit centers can be divided according to product, department or geographical location, as long as in addition to cost, revenue is also generated.

The role of cost and profit centers

Aiding decision-making

Better accountability

Tracking problem areas

Increasing motivation

Benchmarking

Problems of cost and profit centers

Indirect cost allocation

External factors

Inter-center conflicts

Staff stress

Constructing a budget (HL)

The following terms are important when constructing a budget:

Total income – this is a summation of all income or money received by a business. Common income sources include sales revenue and interest earned.

Total expenses – this is a summation of all expenses or cost of operations incurred by a business. Common expenses include material costs, salaries and wages, rent, and advertising costs.

Net income – this is the difference between the total income and total expenses.

Budgeted figure – this is the estimated amount of money to be received or spent as set out in the budget.

Actual figure – this is the amount of money that is definitely received or spent as a result of business activity.

Variance – this is the difference between the budgeted figure and the actual figure.

Variance analysis (HL)

In budgeting, a variance is the difference between the budgeted figure and the actual figure. This variance is usually calculated at the end of a budget period once the actual amounts are determined. Variance analysis is a budgetary control process of assessing the differences between the budgeted amount and the actual amount. This analysis can be done for both cost and sales revenue budgets. Variances can either be favorable or adverse. A favorable variance is when the difference between the budgeted and actual figure is financially beneficial to the firm. An adverse variance occurs when the difference between the budgeted and actual amount is financially costly to the firm.

The importance of budgets and variances in decision-making (HL)

Decision-making is a process that involves selecting a course of action from various possible alternatives with the aim of providing a solution to a given problem. Choices are made by identifying the problem, gathering relevant data or information, and assessing alternative resolutions.

Benefits of using budgets and variances in decision-making

Planning

Motivation

Resource Allocation

Coordination

Control

SMART goals

Comparison

Detecting deviation

Objective appraisal

Limitations of budgets in decision-making

Inflexible budgets that do not consider any unforeseen changes in the external environment, such as increases in raw material costs, may be too difficult to stay within and therefore be unrealistic.

Significant differences between the budgeted and actual results could make the budget lose its importance as a decision-making tool.

Since most budgets are based on the short term, long-term future gains (such as increased sales potential due to unexpected increases in demand) could be lost by looking only at the current budgeted amount.

Highly underspent budgets towards the end of the year could result in unjustified wasteful expenditure by managers.

Setting budgets without involving some people could make them feel resentful and affect their motivation levels.