The Basic Economic Problem

Economic Problem

- There are too few productive resources to make all the goods and services that consumers need and want.

- Unlimited wants and limited resources

- Scarcity of resources is the basic economic problem

Types of goods

- Economic goods: A good or service that has a degree of scarcity and therefore an opportunity cost.

- Free goods: A good or service that is not scarce and is available in abundance. For example, the air we breathe.

Factors of Production

- Consumers are people or firms who need and want goods and services

- Resources or factors of production are used to make goods and services

CELL

- Capital: the man-made resources that are used to produce goods/services (e.g. tractor)

Capital goods and semi-finished goods or components are used up in production

- Enterprise: the skills and willingness to take the risks required to organize productive activities

Entrepreneurs organize and combine resources in firms to produce goods and services

Durable consumer goods last long while (e.g. furniture) non-durable consumer goods (e.g. food) do not

- Land: natural resources used in production (e.g. land)

- Labour: human effort used in production of goods/services (e.g. workers)

Opportunity Cost

- Opportunity cost is the cost of choosing between alternative uses of resources

- Choosing one use will always mean giving up the opportunity to use resources in another way, & the loss of goods & services they might have produced instead

- Problem of resource allocation is choosing how best to use limited resources to satisfy as many needs and wants as possible and maximize economic welfare

- Economics aims to find most efficient resource allocation

- Example 1: A person invests $10,000 in a stock

- Could have earned interest by leaving $10,000 dollars in bank account instead

- Opportunity cost of decision to invest in stock is the value of the potential interest

- Example 2: A city decides to build a hospital on vacant land it owns

- Could have built school or sports centre

- Opportunity cost is the value of the benefits forgone of the next best thing which could have been done

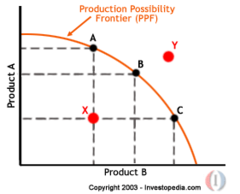

Production Possibility Curves & Choice

- Opportunity cost can be shown using a production possibility curve (PPC)

- It shows the maximum combinations of goods and services that can be produced by an economy in each period of time with its limited resources

- A PPC shows all the combinations of possibilities, involving two goods or options

- Each combination is a choice

- An economy can use all its scarce resources to produce this combination

- A point within the curve signifies like X, represents inefficiency

- A point outside the curve like Y, represents combinations that cannot be produced due to the lack of resources