1.3.3 Pricing Strategies

Price is fundamental to most consumers buying decisions. It is a key communication between producer and consumer. It can also give the customer a message about the products quality.

The correct price is important due to the companies profit margins (the different between price and cost).

Pricing Strategies

a pricing strategy is a medium to long term plan for setting prices.

Price Skimming

product is priced high to begin with then prices can be lowered later on.

this is usually done with technology as it has a short lifecycle due to newer models and the product can attract a new market at its lower price.

normally done when the product is innovative as there is less likely to be competition so customers will pay the high price.

- usually done to recover research and development costs

- high prices may make the product seem like a must have item when new

- if competitors enter the market prices can be lowered

problems with it are:

- some customers may be put off by the expensive prices at the start

- it may affect the image of the brand to drop prices later on

- people who buy at the high price may be annoyed when they fall

Price Penetration

Price penetration is the opposite to price skimming.

The price is set low and once the product is established it can be increased.

This is useful for products starting in a competitive market as it helps them gain market share quickly.

One example is Walmart. When they open a store in a new are they will start their prices very low for essential products such as milk and locals will start buying from Walmart as it is a much better deal than local stores. Sadly, this will then put the local stores out of business and the Walmart will bring their prices up, hoping to recover their cost of the sales.

Cost-Plus Pricing

cost plus pricing is adding a percentage on top of the production costs to make a profit.

The cost of production is the total cost of making a product, including the cost of materials, labor, and overhead. The markup percentage is the amount of profit that the seller wants to make on each sale.

Cost plus pricing is a simple and pricing strategy. It is also an accurate way to set prices, as it takes into account the costs of production. However, cost plus pricing can be a less competitive pricing strategy, as it does not take into account the prices of other sellers in the market.

Competitive Pricing

competitive pricing is setting prices related to other products on the market. setting prices the same or lower than competitors will attract customers. Can also be used to try and steal customers from established brands by undercutting with a lower price. (most important in physical shops where there are many similar items on a shelf)

the problem with competitive pricing is that you do not have much control and are forced to change according to competitors.

Predatory Pricing

predatory pricing is when you price your products low enough to drive a rival out of business 😱. Sometimes the business will even take a loss to do this. (they will then raise the prices when they have succeeded!) Once they have done this there will be no competition left and the consumers will have no other options so they can charger what ever they want!

however for this to work the predator must be strong financially to lose money for a bit and the prey must be weak already!

Psychological Pricing

more of a tactic than a strategy, psychological pricing is usually a short term method.

It is setting prices in a way that entices customers without changing the price very much.

For example setting all fuel prices to £4.99 means they look like they are under £5 when actually they are only 1p under.

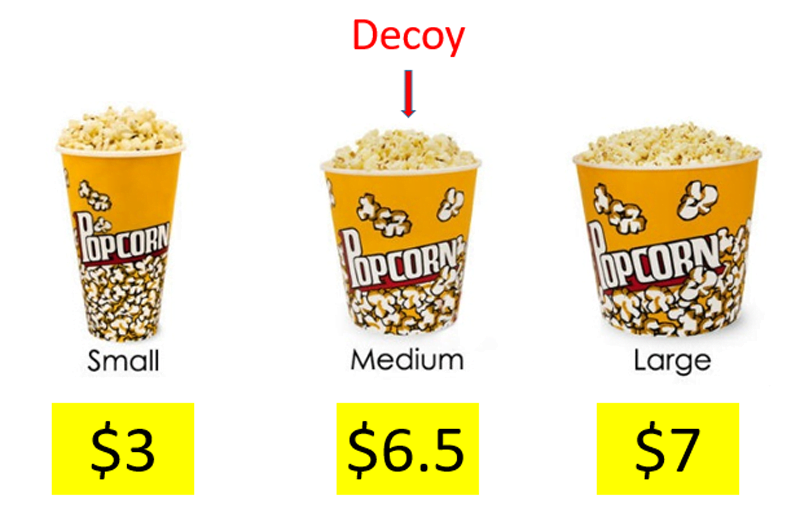

Also, psychological pricing can include tactics such as offering a medium option which makes the more expensive one look like better value:

this is known as decoy pricing.

this is known as decoy pricing.

Factors that effect which strategy to use

- Number of unique selling points (USPs) or amount of differentiation

A product with more USPs or that is more differentiated from its competitors is less price-sensitive, meaning that customers are less likely to switch to a competitor if the price is higher. This gives businesses more flexibility in setting prices.

- Level of competition in the business environment

In a competitive market, businesses need to set prices that are competitive with their competitors in order to attract customers. This can lead to lower prices and lower profits.

- Strength of brand

A strong brand can command a higher price than a weaker brand. This is because customers are more likely to be loyal to a strong brand and are less likely to switch to a competitor even if the price is higher.

- Price elasticity of demand

Price elasticity of demand measures how sensitive customers are to changes in price. A product with low price elasticity of demand means that customers are not very sensitive to changes in price, meaning that businesses can charge higher prices without losing too many customers.

- Stage in the product’s life cycle

The stage in the product’s life cycle can also affect pricing strategy. For example, new products are often priced high to recoup the costs of development and marketing. As the product matures, prices can be lowered to attract more customers.

- Costs and the need to make a profit

Businesses need to charge more for their products than it costs to make them in order to make a profit. However, businesses may also choose to lower prices in order to gain market share or to attract customers who are price-sensitive.

Ultimately, the best pricing strategy for a particular business will depend on a number of factors, including the type of product or service, the target market, and the competitive landscape.

Changes in pricing to reflect social trends

Online sales

Online sales have had a significant impact on pricing in a number of ways. First, they have increased competition among retailers. This is because online retailers can reach a much wider audience than traditional brick-and-mortar stores. As a result, retailers are under pressure to keep their prices low in order to compete.

Second, online sales have made it easier for consumers to compare prices. This is because price comparison websites allow consumers to compare prices from different retailers for the same product. This has made it easier for consumers to find the best deal, which has put pressure on retailers to keep their prices competitive.

Price comparison sites

Price comparison sites have also had a significant impact on pricing. These sites allow consumers to compare prices from different retailers for the same product. This has made it easier for consumers to find the best deal, which has put pressure on retailers to keep their prices competitive.

In addition, price comparison sites can also help consumers to find new and innovative products that they may not have otherwise known about. This can lead to increased demand for these products, which can put further pressure on prices.

Key Definitions

Price elasticity - The measure of how responsive demand is to a change in price.

Price sensitive - When demand responds more than proportionately to a change in price, indicating high price elasticity.

Pricing tactics - Short-term pricing responses implemented to leverage opportunities or address threats in the market.

Pricing strategy - The establishment of the initial price of a product and the formulation of a company's plan for setting prices over the medium-to-long term.

Cost-plus pricing - A pricing approach where the price of a product or service is determined by calculating its cost and adding a predetermined amount or percentage to it.

Competitive pricing - A pricing strategy that involves charging a similar amount for goods or services as compared to competitors.

Penetration pricing - A strategy in which a company initially sets a low price for its product to capture a significant portion of the target market.

Price skimming - The practice of initially setting a high introductory price for a product, often coupled with extensive promotion, and gradually reducing the price over time. This approach is commonly used to recover the initial heavy investment in the product.

Markup - The amount added above the cost of a product or service before it is offered for sale.

Loss leader - A product that is deliberately priced below cost with the intention of attracting customers and generating additional profitable business.