Chapter 15 - Sources of finance

Firms need finance to:

provide working capital

invest in non-current assets

Criteria for choosing a source of finance:

Cost: Debt is typically cheaper than equity.

Duration: Long-term finance is often more expensive but deemed safer than short-term finance.

Term Structure of Interest Rates: Usually, short-term finance has lower costs, but this isn't always the case.

Gearing: Reflection of current debt levels; Adding debt is usually cheaper than equity but high gearing is risky

Accessibility: Some sources may not be available to all firms.

Relationship Between Risk and Return

Risk: is the variability of potential returns.

Investment risk arises because returns are variable and uncertain.

An increase in the risk taken on by an investor generally requires an increase in returns provided by the investment.

Each time an investor demands a higher return on the finance they have provided, this is reflected in a higher cost of that finance to the company:

Shareholders: provide equity funding to the business. They buy shares that allow them to participate in the fortunes of the business. This means that if the business does well, so do they. If the business does badly, so do they.

Some industries are riskier to invest in than others. Food companies such as Heinz are long-established and may provide stable returns, while new tech start-up companies will be inherently more risky, with unpredictable levels of success and therefore of returns to investors.

Dividends are only paid at the discretion of the directors and share prices will rise and fall in line with company fortunes.

Shareholders therefore take on high levels of risk in their investment.

eg: Supermarkets and discount retailers tend to have stable returns and are not affected significantly by changes in the economy. These stable returns are lower risk and more predictable for the investor and hence they would see a lower return on their investment.

The airline and the yacht manufacturer will see their profits fluctuate from year to year, as the companies rely on a strong economy. As these profits are less stable and predictable, they are at higher risk and so their investors will demand a higher return.

Lenders: provide debt finance to the business.

They lend money in return for interest receipts and capital repayment.

Their returns are legally guaranteed via debt agreements.

Therefore, even when it comes to lending to companies in risky industries, debt providers will be more protected than equity providers.

Debt providers therefore take on less risk on their investment than shareholders do.

As shareholders take on more risk than debt providers, they will demand a higher return on their investment than lenders do.

This means that from the company point of view, equity funding will be more expensive to raise than debt funding.

Short-term Sources of Finance

Bank Overdrafts: Flexible, used as needed.

Bank Loans: Secure but require assets for collateral.

Better Management of Working Capital: Focus on profitability vs. liquidity decisions (collect receipts faster, delay payments to suppliers, have a more efficient inventory system in place)

Leasing: Allows spreading the cost of an asset over time. This could work out more expensive overall but allows cash flow to improve.

Sale and Leaseback: Generates immediate cash for other purposes (sell existing asset within the company and then lease it back over time).

Long-term Finance - Equity

Equity shareholders (ordinary shareholders) are the owners of the business and exercise ultimate control through their voting rights.

Equity finance is the investment in a company by the ordinary shareholder, represented by the issued ordinary share capital plus reserves.

While strictly preference shares are an equity source of finance, their characteristics bear more resemblance to debt finance and so for the purposes of such calculations as gearing they are considered to be part of debt rather than equity (don’t own the company - only buying the right to preference - paid first - dividend).

If a company is unsure of the price to set for new shares, they can invite new shareholders to tender for a price. The company will then issue new shares at the highest price that will generate the funds that they need.

Free shares given to existing shareholders is known as a bonus issue.

Offering existing shareholders the right to buy a new share is a rights issue.

Selling shares to the public at a price agreed by the company is a fixed price issue to the public.

Raising equity

Internally generated funds (retained earnings not already paid out as dividends or used for prior investment. Quick and cheap source of finance if available)

Rights issues (the issue of new shares to existing shareholders in proportion to their existing shareholdings at a discount to the current market value)

New external share issues (placings, offers for sale, etc.)

Rights issues

More expensive than internally generated funds but cheaper than a new issue.

Shareholders can sell their rights instead of taking them up.

Issuing new shares at a discount will cause the share price to fall.

Theoretical ex-rights price (TERP) = (Market value of shares already in issue + proceeds from new share issue) /nb of shares in issue after the rights issue

ex-rights price is our best estimate of the share price immediately after the rights issue has taken place

Market value of shares already in issue = nb of shares currently in issue x market price per share

proceeds from new share issue is the amount of money generated from the rights issue process

nb of shares in issue after the rights issue (ex-right) = original number of shares + new ones generated from rights issue

Value of a right

When a rights issue is made by a company, shareholders have a choice as to whether to take up the rights or not. If they do not wish to purchase more shares, they may sell the rights. The right means that an investor can purchase a share in the company at a discounted price.

Value of a right = TERP – issue (subscription) price

Value of a right per existing share = (TERP – issue price)/no. of shares needed to obtain a right

Shareholder Options in Rights Issues

take up the rights by buying the specified proportion of shares at the price offered

renounce the rights and sell them in the market.

Renounce part of the rights and take up the remainder

Do nothing (will lose wealth as shares held will fall in value to the TERP)

Example: Mira shareholder offered 1 for 3 rights issye at 1.50, with current market value of the share of 1.90 and a TERP of 1.80. The value of each right is worth 0.30. Mira currenctly has 900 shares which, before the rights issue are worth 900 × 1.90 = 1,710.

If she takes up her rights, The new value of shares would be (900+900/3×1)*1.80=2,160

But this has cost 1.50 per share = 1.50 × 300 = 450

So overall Mira’s wealth is 2,160-450 = 1,710

Result: Wealth maintained

Second option is to sell the offered rights this would means that after the issue, her shares would only be worth 900×1.80=1,620 But she would make some money from the sale of the rights. Assuming that they are sold at maximum 0.30 each = 300×0.30 = 90 + 1,620 =1,710

Result: wealth maintain

Option 3: Do nothing: Then will only own 900 shares which are worth 1,620 and will not make any spare cash

Result: wealth would fall

If shareholder wants to maintain wealth and control then should buy the shares offered.

New External Share Issues

This is where brand new shares are offered to all investors.

expensive

may fail

may require business to become quoted – stringent criteria to adhere to

via placing, enterprise investment scheme, public offer, fixed price offer, offer for sale by tender

dilution of control for existing shareholders.

Rule of law. When raising finance, companies should be aware of and comply with the relevant legislation and regulations that apply.

Democracy. To issue new shares, directors may need approval from a majority of existing shareholders.

Such issues are expensive and may fail if enough investors cannot be found to purchase enough shares to raise the required total cash needed by the company. Some companies will choose to have the issue insured, known as underwriting, to make sure enough cash is raised.

In some cases, to raise enough cash, a company may need to list on a stock market, becoming a quoted company, in order to access a wider potential pool of investors.

In order to undertake a new issue, because it will be likely to lead to a dilution of control for existing shareholders, it may be that approval needs to be gained from them beforehand.

There are a number of methods of issuing new shares. For instance, they may be offered directly to the general public, or placed with specific institutional investors, such as pension or trust funds.

The issue may be at a fixed price, where every new investor pays the same price, or by tender, where investors bid for shares at a price of their choosing and shares generally end up being allocated at the highest price that would allow all shares to be sold.

Long-term finance – debt

Long-term debt (bonds), usually in the form of debentures or loan notes, is frequently used as a source of long-term finance as an alternative to equity.

A bond is a written acknowledgement of a debt by a company, normally containing provisions as to payment of interest and the terms of repayment of the principal.

Long-term loans are long-term versions of short-term loans. They would normally be provided by banks, which would ask for security in the form of company assets.

Long-term corporate debt (loan notes, also known as bonds or debentures – these terms are interchangeable for the exam) is frequently used as a source of long-term finance as an alternative to equity.

A loan note is a written acknowledgement of a debt by a company, normally containing provisions on payment of interest and terms of repayment of the principal (loan amount). They are traded on a market.

Individual lenders can purchase loan notes, which effectively means that they are lending money to the company for the duration of the bond.

Loan note terminology

As an example, a loan note may be stated as being:

5% loan note with a price of $120 and a nominal value of $100, redeemable in 3 years at nominal value.

5%: This refers to the coupon rate. This is the annual interest rate paid out to lenders (loan note holders) and is calculated as a percentage of the nominal value of debt.

The nominal value is usually $100 unless the exam question states otherwise.

So, in this example, the loan note holder will receive interest of 5% × $100 = $5 for each year of the loan.

Loan note: There are many types of loan notes, and the terms loan notes and bonds may be used interchangeably.

Loan notes may be redeemable or irredeemable. If redeemable, the repayment date will be specified in the terms of the loan note. If irredeemable, interest will be paid to the loan note holder into perpetuity.

They may also be secured or unsecured (security may come in the form of a fixed charge over specific assets or a floating charge over all assets or a category of assets).

Price of 120: This is the market value of debt and will fluctuate just like share prices do, although usually for different reasons. In this example a loan note holder will pay $120 for a debenture with a nominal value of only $100.

A reason for this is that the base rate in the economy is low making it unlikely investors can generate much return on their funds without investing it somewhere.

A loan note is a low risk investment and so will be a very attractive source of investment when base rates are low. The more attractive they are, the more a company can charge for it.

Redeemable in 3yaers: If debt is redeemable, then it will be repaid by the company at the end of the loan, as defined in the loan note agreement. In this example it will be repaid in 3 years’ time.

At nominal value: As with shares, a loan note will have a nominal value that does not change over its life. When traded, it will also have a market value that fluctuates. When a loan note is issued, it is recorded at nominal value in the books of account. If more than $100 is paid for the loan notes at issue, the extra money received will also be recorded, but the nominal value itself is not adjusted. In the exam, assume that each loan note has a nominal value of $100 unless the question states otherwise. Redemption at nominal value simply means that the company will pay back the loan note holder $100 at the end of the loan note duration.

Features:

traded on stock markets

usually denominated in blocks of $100 nominal value

interest (coupon) paid as a percentage of nominal value

may be secured or unsecured (security may come in the form of a fixed charge over specific assets or a floating charge over all assets or a category of assets)

may be redeemable or irredeemable (if redeemable the repayment date will be specified in the terms of the bond)

Note: for the purposes of the FM exam, consider the terms bonds and loan notes to represent the same thing.

Debt in comparison to equity

For Investor

Advantages: Low risk, low return - Investors are assumed to be rational – they will only take on extra risk if higher returns are to be earned. Certain investors want predictable, low risk investments. They don’t want to run the risk of losing their money! Pension funds are typical low risk investors. They need to protect their funds to have money to pay out to pensioners.

Disadvantages: No voting rights (no control)

As debt investors do not have equity shares, they can’t influence the direction of the company. If management are following a path that the debt investor does not like, the investor cannot force a change in direction.

For Company

Advantages: Cheap, predictable, doesn’t dilute control

Debt investors expect low returns given that they are taking less risk. This saves the company money.

Returns are predictable – the company knows how much it is going to have to pay out, so can budget accordingly.

There is no change in share ownership, so the owners of the company will be able to continue to run the business as they see fit.

Disadvantages: Inflexible, increases risk at high levels of gearing, must be repaid

Inflexibility means that in a bad year, the company still has to pay returns to debt investors – even if it can’t really afford them.

Contrast this with dividends on ordinary shares, which can be cut if the company is facing tough times.

Increased risk at high levels of gearing occurs because the company has more fixed outgoings to investors. These have to be paid regardless of performance – so a small drop in profits could leave the company in trouble.

Other Types of Debt Instruments

Deep discount loan notes – issued at a discount to nominal value and redeemable at nominal value and above. Ex: A loan note has an issue price of $80, a redemption value of $120 and pays 2% interest over its life

Zero coupon loan notes – like deep discount but zero interest is paid whilst in issue. The investors’ entire return (unless traded at a high price in a market) is in the form of a capital gain from the difference between the issue and redemption prices. Ex: A loan note has an issue price of $70, a redemption price of $130 and pays no interest over its life

Hybrid loan notes – convertibles – these give the loan note holder the right to convert (if they choose at the time) the debt into other securities, normally ordinary shares, at a future date. Ex: A loan note can be exchanged for 20 shares in 5 years’ time

Hybrid loan notes – with warrants – these give the loan note holder the right to subscribe at a fixed future date for a certain number of ordinary shares at a predetermined price. Ex: A loan note holder can buy 20 shares at a discount in 2 years’ time

Leasing Finance

Long-term lease arrangements would be used as debt finance for assets that have a useful life over the medium to long-term period.

Lease generally covers the whole useful life of the asset

Lessor does not usually deal directly in this type of asset

Risks and rewards of ownership generally passed to the lessee

Lease agreement cannot be cancelled.

Leasing is a type of debt finance that allows the payments to be spread over the life of the asset, rather than being paid up front.

Lease agreements are usually difficult to cancel and the risks and rewards are likely to be passed to the lessee, as they will use the asset for the majority of its useful life.

In most cases because the risks and rewards have been transferred, it means that the lessee would need to maintain the asset, but they do not legally own the asset and so cannot claim writing down allowances.

Venture Capital

Venture capital is the provision of risk-bearing capital, usually in the form of a participation in equity, to companies with high growth potential.

Venture capitalists provide start-up and late stage growth finance, usually for smaller firms and will often look for an exit route in the form of flotation of the company enabling them to sell their investment.

Venture capital investors take up shares in small, fast growing companies that have significant growth potential.

They provide the funds to help the business grow, and often take an active role in advising the company too.

Venture capitalists usually aim to grow the company to the point at which it can be floated on the stock market (called a listing). This allows them to sell their shares, all being well at a huge profit on their original stake.

Bank loans

Bank loans are flexible in terms of length and can be offered either short- or long-term.

The terms of the loan are set by the bank. This means that this type of finance may be more restrictive than finance from the issue of loan notes.

Can be short- or long-term.

Terms set by the bank, meaning that loan finance may be more restrictive than loan note finance.

Loans secured against property are called mortgages

Sources of finance for small and medium enterprises (SMEs)

SMEs tend to be unquoted and can have difficulty raising finance because:

Small number of owners with limited capital available between them

Lack of business history or proven track record

lower level of public scrutiny over accounts and records

lack of internal controls and governance over owner-manager decisions

lack of tangible assets to use as security for lending.

The funding gap

Because of the above issues, there can be a gap between the finance that SMEs could productively use and the finance that is available to them. This is known as the funding gap. This may be bridged by using:

business angels (usually under 100k) or venture capitalists (usually above 250k)

government grant

High street bank (loan and overdraft)

Seed capital (owners and family funds)

supply chain financing, crowdfunding, peer-to-peer funding.

personal guarantees made by wealthy shareholders to lenders (sacrifice of limited liability)

The maturity gap

SMEs may find it easier to obtain long-term finance secured against their assets than short or medium-term finance.

But for short to medium-term assets it would prefer to raise short to medium-term finance to match the term of its assets against its liabilities and keep funding costs down.

The inability to do this is known as the maturity gap.

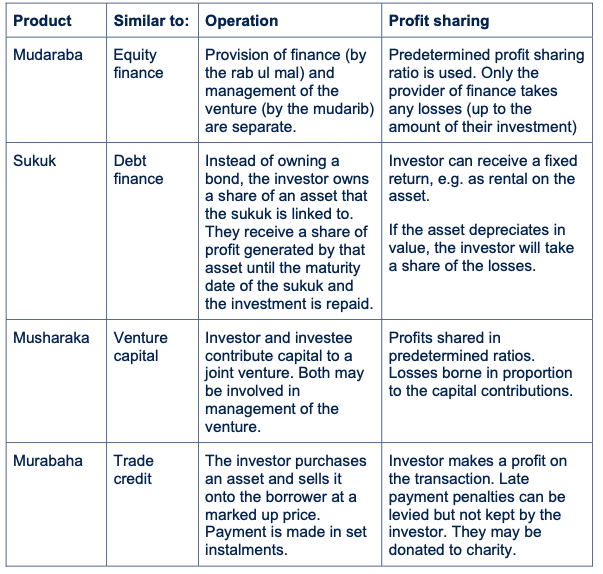

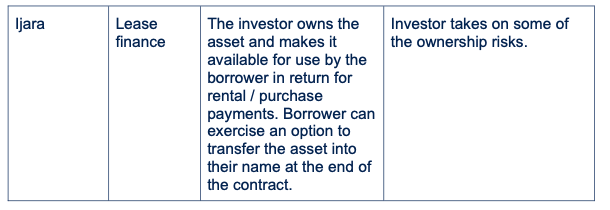

Islamic Finance

Not all finance providers operate on the same principles. A traditional UK bank such as Barclays may offer loans in return for interest and capital repayments. However, such a loan would not be acceptable under Sharia law, followed by those of the Muslim faith, as it is considered unethical to earn money simply from the provision of money.

Learning about Islamic finance will aid your understanding of the differences between those of different faiths and help those of you who are undertaking apprenticeships grasp the concept of the British value of tolerance and mutual respect.

Islamic finance operates in accordance with the principles of Sharia law:

Sharing of profits and losses

no interest (riba) allowed

Restricted to Islamically accepted transactions, i.e. no investment in alcohol, gambling, etc.

Main sources of Islamic finance are:

Tolerance and mutual respect. Those dealing with potential finance providers of different faiths should understand and respect that the criteria used by the finance providers to determine the acceptability of a project may be different to their own.