The trial balance

Introduction

A trial balance is a list of the balances on the accounts in the ledger at a certain date. A trial balance is prepared to check the arithmetical accuracy of the double-entry bookkeeping. The name of each account is listed in the trial balance. The balance on each account is shown according to whether it is a debit balance or a credit balance. The trial balance will show if the total of the debit balances is equal to the total credit balances. It is important to remember that the trial balance is not a part of the double entry system of bookkeeping as it is simply a list of balances. If the ledger accounts are balanced monthly then a trial balance may also be drawn up at the end of each month. The trial balance should be headed with the term ‘trial balance’ along with the date on which it was prepared. The layout of a trial balance is as follows:

Trial balance — a list of balances on the accounts in the ledger at a certain date.

Trial balance — a list of balances on the accounts in the ledger at a certain date.

The purpose of a trial balance

1. The trial balance can help in locating arithmetical errors. However, the balancing of the trial balance is not proof that the entries in the ledger accounts are completely free from errors.

2. A trial balance is useful in preparing financial statements.

The preparation of a trial balance

All the ledger accounts which are ‘open’ (those which still have an amount of money showing in the account) are listed together with the balance on each account. If the debit side of the account is larger in money than the credit side then that account has a debit balance and the amount of the balance (or difference) is entered in the debit column of the trial balance. If the credit side of the account has more money than the debit side then that account has a credit balance and the amount of the balance (or difference) is entered in the credit column of the trial balance. The debit column and the credit column are totalled. If the totals agree, it indicates that the double entry bookkeeping is arithmetically correct.

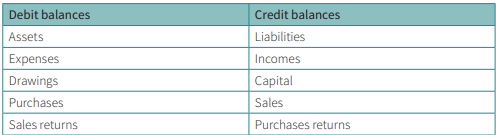

In practice, a trial balance is drawn up using the actual ledger accounts. It is necessary to know the type of accounts which have a debit balance and those which have a credit balance. These are shown in the following table:

The trial balance and errors

If the trial balance fails to balance When a trial balance fails to balance, it is obvious that an error has been made somewhere. This may be:

1. an error of addition within the trial balance

2. An error of addition within one of the ledger accounts

3. entering a different figure on the credit to that entered on the debit when making a double entry in the ledger

4. Make a single entry for a transaction rather than a double entry

5. entering a transaction twice on the same side of the ledger

Checklist for locating errors

■ Check the addition of the trial balance.

■ Check the addition of the balance of each ledger account.

■ Check that each ledger account balance has been entered in the correct column of the trial balance.

■ Check that every ledger account balance has been entered in the trial balance.

■ Look for a transaction equal to the difference in the trial balance and check that a double entry has been made for that transaction.

■ Look for a transaction equal to half the difference in the trial balance and check if it has been entered twice on the same side of the ledger rather than once on each side.

■ Check the double entry for every transaction entered in the books since the date of the last trial balance.

If the trial balance balances

When a trial balance balances, it simply means that the total of the debit balances is equal to the total of the credit balances. It does not imply that the double entry is error-free. The trial balance will still balance if any of the following errors are made:

Error of commission — This occurs when a transaction is entered using the correct amount and on the correct side, but in the wrong account of the same class

Example — Cash received from Malini credited to Mallika’s account.

Error of complete reversal — This occurs when the correct amount is entered in the correct accounts, but the entry has been made on the wrong side of each account.

Example — Cash drawings debited to the cash account and credited to the drawings account.

Error of omission — This occurs when a transaction has been completely omitted from the accounting records. Neither a debit entry nor a credit entry has been made.

Example — Payment of wages not entered in the books.

Error of original entry — This occurs when an incorrect figure is used when a transaction is first entered into the accounting records. The double entry will therefore use the incorrect figure.

Example — Goods, $100, bought on credit but recorded as $1 000

Error of principle — This occurs when a transaction is entered using the correct amount and on the correct side, but in the wrong class of account.

Example — Motor expenses debited to the motor vehicles account

Compensating errors — These occur when two or more errors cancel each other out.

Example — Purchases account underadded by $100 and sales returns account over-added by $100.

Summary

■ A trial balance is a list of the balances on the accounts in the ledger at a certain date.

■ A trial balance is prepared to check the arithmetical accuracy of the double entry book-keeping. ■ If a trial balance fails to balance, it indicates that an error has been made.

■ There are six types of error which are not revealed by a trial balance.