Microeconomics Chapter 16: The Demand for Resources

Microeconomics Chapter 16: The Demand for Resources

Significance of Resource Pricing

Resource pricing plays a crucial role in economic theory and practice.

Its significance includes money-income determination, cost minimization, resource allocation, and addressing policy issues.

Money-Income Determination

Prices of resources impact the incomes of individuals and firms, thereby influencing overall economic activity and demand for goods/services.

Cost Minimization

Firms aim to minimize costs by employing the optimal combination of resources, influenced by resource pricing.

Resource Allocation

Resource pricing drives efficient allocation of resources towards their most valued uses.

Policy Issues

Understanding resource pricing informs policy decisions regarding taxation, subsidies, and regulation.

Marginal Productivity Theory of Resource Demand

Derived Demand: The demand for resources arises from the demand for the products they help produce. - That is, demand for resources is contingent on product demand.

Determinants of Resource Demand

Changes in Product Demand: Shifts in consumer preferences or needs change the demand for resources.

Changes in Productivity: Enhancements in technology, quality of resources, or quantities of complementary resources affect resource demand.

Changes in Price of Substitute Resources: The substitution effect and output effect dictate changes in resource demand.

Changes in Price of Complementary Resources: Fluctuations in the prices of resources usually used together will impact overall demand.

Marginal Productivity Theory

Assumptions

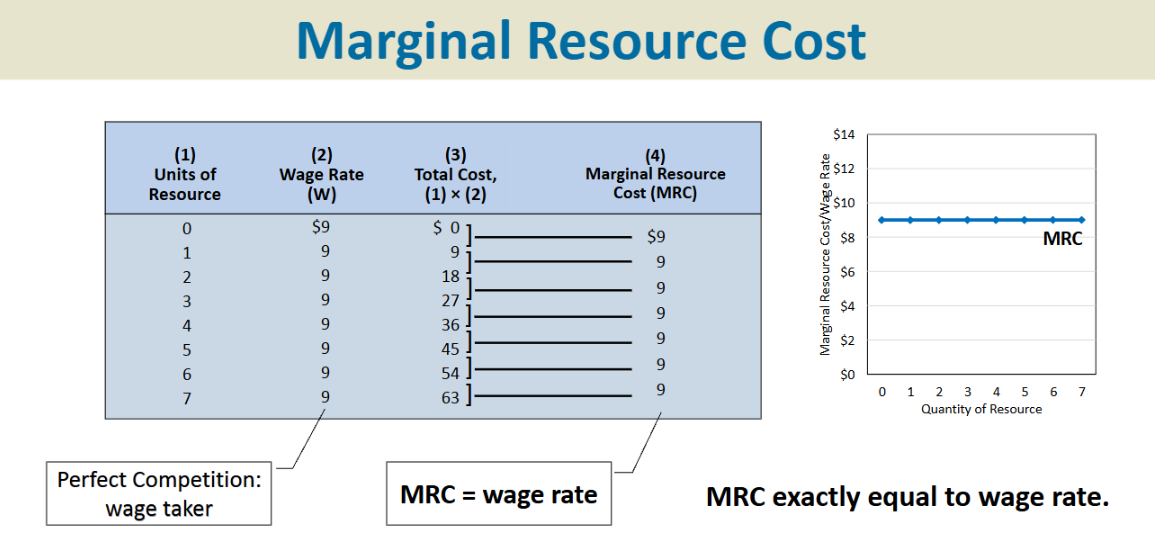

Perfect Competition in product and resource markets, wherein: - Firms are price takers in competitive product markets. - Firms are wage takers in competitive resource markets.

Key Relationships

Marginal Product of Resource (MP): The additional output gained by employing one more unit of the resource.

Price of Product (P): The market price at which the product is sold.

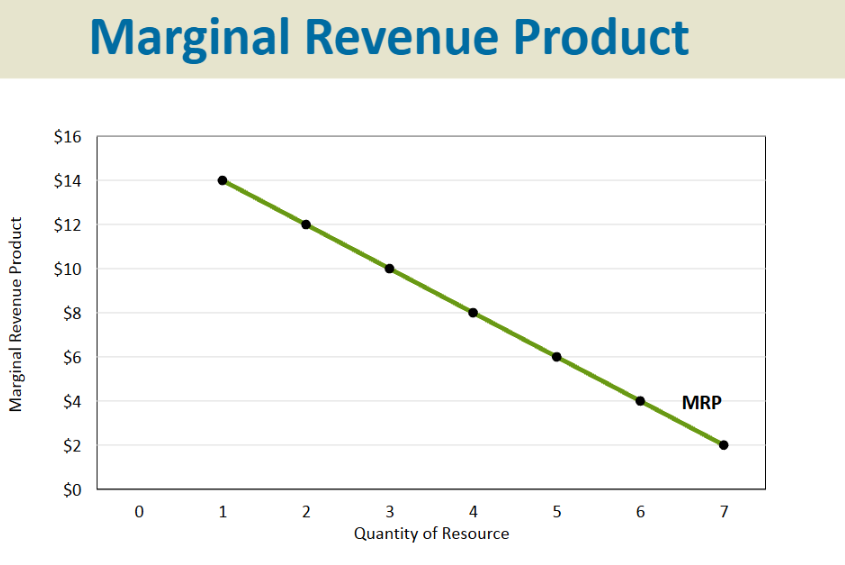

Marginal Revenue Product (MRP)

Definition: Change in total revenue resulting from a change in resource input (labor). - Formula:

Marginal Resource Cost (MRC)

Definition: Change in total resource cost resulting from a change in resource input (labor). -

Profit Maximization Rule

Firms maximize profit by hiring additional resources until the added revenue (MRP) equals the added cost (MRC). - If MRP > MRC, profit increases. - If MRP < MRC, profit decreases. - If , profit is maximized.

Labor Demand in Perfect Competition

In a perfect competition setting, labor demand reflects the relationship between the wage rate and the quantity of labor hired.

MRP function represents the firm’s demand schedule.

Labor Demand in Imperfect Competition

Firms with higher market power may influence prices, leading to a downward-sloping MRP curve.

Two primary reasons for downward-sloping MRP in imperfect competition: 1. Law of Diminishing Returns: Marginal product decreases as more labor is added. 2. Downward Sloping Demand for Product: As firms increase quantity produced, the price at which they can sell their output decreases.

Determinants of Resource Demand: Shifts in Demand Curve

Change in Product Demand: Examples include increased demand in sectors like gambling (for casino workers) or decreased demand for leather goods (decreasing demand for tanners).

Change in Productivity: Higher skill levels among workers or improved technology can raise demand for respective services.

Resource Price Changes: Fluctuations in the price of electricity can impact aluminum production and thus the demand for aluminum workers. Substitutions like part-time workers may also arise due to insurance costs.

Occupational Employment Trends

Notable trends include rising employment in health services with roles like personal care aides and declining employment in sectors such as telephone operating.

Income Distribution

Overview of the Marginal Productivity Theory of Income Distribution:

- Workers and resource owners are compensated based on the value of their contributions. - Explains income inequality: productive resources are inequitably distributed, and market imperfections play a role.

Closing Thoughts: Labor and Capital

The interaction between banks, labor, and capital (e.g., ATMs as capital) highlights how resources can shift from being substitutes to complements over time as technology evolves. Initially, ATMs displaced tellers, but they evolved to work alongside them, leading to increased demand for both capital and labor.

Conclusion

Understanding resource demand, pricing, and productivity implications is essential for efficient economic functioning and policy-making.