Chapter 1 - Taking Risks and Making Profit within the Dynamic Business Environment

1.1 Business and Wealth Building

Business - Any activity that seeks to provide goods and services to others while operating a profit.

Goods - Tangible products such as computers, food, clothing, cars, etc.

Tangible - Things you can touch.

Services - Intangible products such as education, health care, travel, etc.

Intangible - Products that can’t be held in your hand

One result of successfully filling a market need is that you can make money for yourself by giving customers what they want.

Entrepreneur - A person who risks time and money to start and manage a business.

Revenues, Profits, and Losses

Revenue - The total amount of money a business makes during a given period by selling goods and services.

Profit - The amount of money a business earns above and beyond what it spends for salaries and other expenses needed to run the operation.

Loss - Occurs when a business’s expenses are more than its revenues.

About 80,000 businesses close each year in the US.

The business environment is constantly changing.

Matching Risk with Profit

Risk - The chance an entrepreneur takes of losing time and money on a business that may not be profitable.

Usuallym enterprises that take the most risk make the most money. Big risks can mean big profit.

Standard of Living and Quality of Life

A nation’s businesses are part of an economic system that contributes to the standard of living and quality for everyone in the country.

Standard of living - The amount of goods and services people can buy with the money they have.

United States has one of the highest standards of living.

Quality of life - The general well-being of a society in terms of its political freedom, natural environment, education, health care, safety, amount of leisure, and rewards that other goods and services provide.

There’s more to quality of life than simply making money.

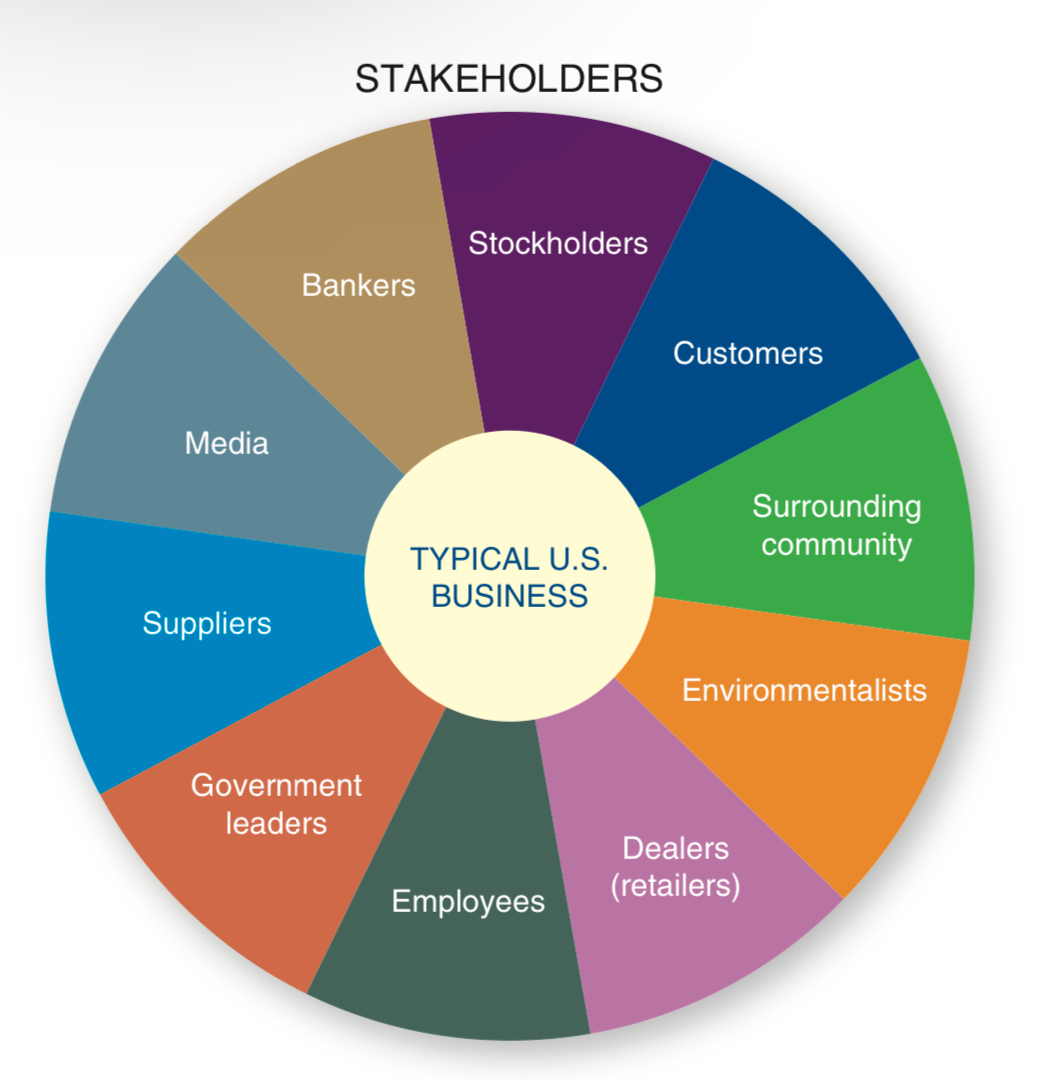

Responding to the Various Business Stakeholders

Stakeholders - All the people who stand to gain or lose by the policies and activities of a business and whose concerns the business needs to address.

In order to stay competitive, outsourcing may be used.

Primary challenge for organizations of the 21st century - Recognize and respond to the needs of their stakeholders.

Outsourcing - Contracting with other companies to do some or all of the functions of a firm. This might be a result of staying competitive.

Insourcing - The opposite of outsourcing.

Using Business Principles in Nonprofit Organizations

Nonprofit organization - An organization whose goals do not include making a personal profit for its owners or organizers.

They strive for financial goals, but they’re used to meet their social or educational goals instead of personal profit.

1.2 The Importance of Entrepreneurs to the Creation of Wealth

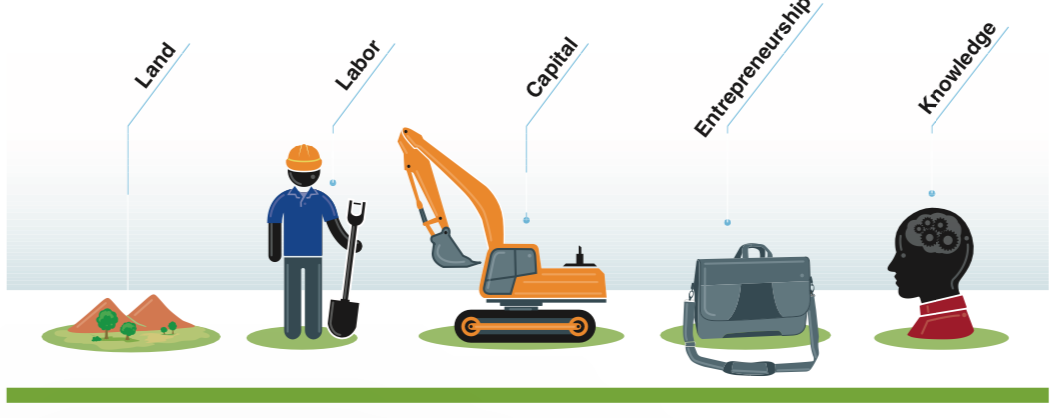

The Five Factors of Production

Land

Labor

Capital (Anything used in the production of goods)

Entrepreneurship

Knowledge (This is the most important factor of production in our economy).

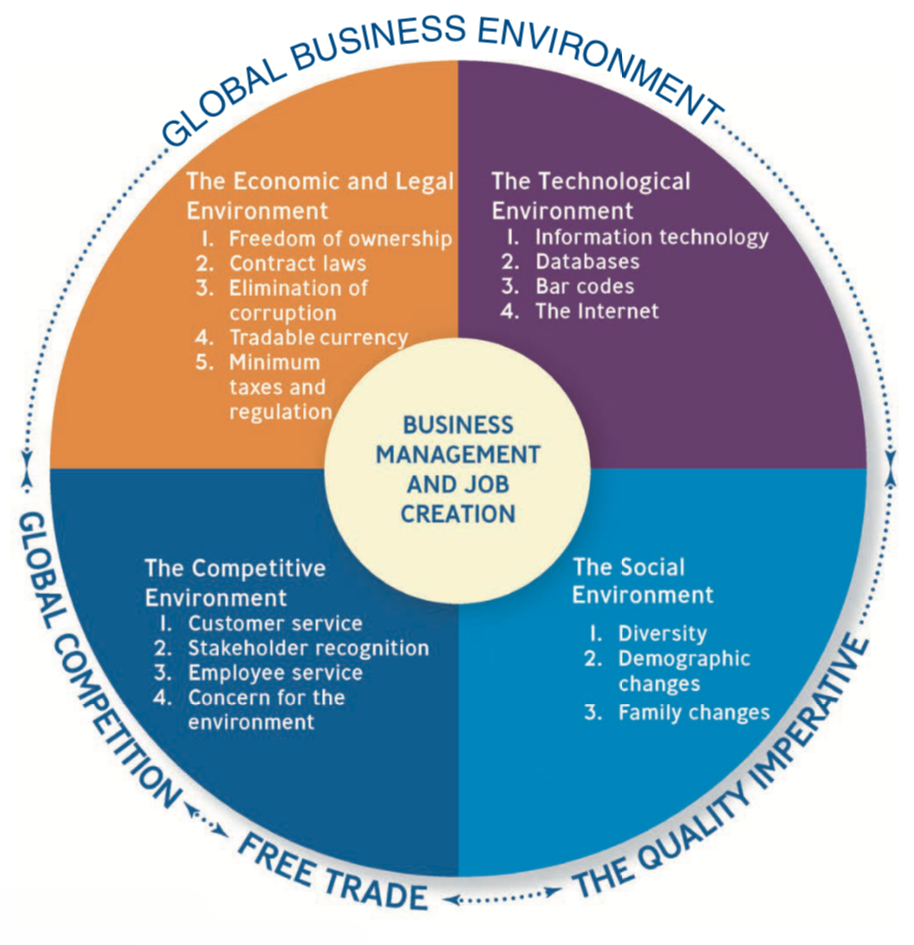

The Business Environment

Business environment - Consists of the surrounding factos that either help or hinder the development of businesses. These are the five elements in the business environment:

The economic and legal environment

The technological environment

The competitive environment

The social environment

The global business environment

Creating the right business environment is the foundation for all types of social benefits.

1.3 The Economic and Legal Environment

The economic system and government have a strong impact on the level of risk that starting a business has. People will only start a business if the risk levels are low.

A government can minimize spending and keep taxes and regulations to a minimum.

Government can promote entrepreneurship by allowing private ownership of businesses. In some countries, most businesses are owned by the government demotivating people to start their own. However, some countries are selling those businesses to private owners to create wealth. Governments of developing countries can minimize interference with the free exchange of goods and services.

Also, it can reduce risk by approving laws that enable businesspeople to write enforceable contracts. In the US, the Uniform Commercial Code regulates business agreements such as contracts and warranties so firms know they can rely on each other. Risk is higher in countries without these types of laws.

Government can also establish a currency that’s tradeable in world markets so it’s easily exchanged when buying or selling goods and services anywhere. Lastly, it can help reduce corruption in business and in its own ranks.

1.4 The Technological Environment

Effectiveness - Producing the desired result.

Efficiency - Producing goods and services using the least amount of resources.

Productivity - The amount of output you generate given the amount of input.

E-commerce - The buying and selling of goods online. There are two types of e-commerce:

Business to consumer (B2C)

Business to business (B2B)

Identity theft - The obtaining of an individual’s personal information.

1.5 The Competitive Environment

To stay competitive, businesses need to offer high-quality products and good value. They also need to exceed customer’s expectation and empower workers.

Empowerment - Giving frontline workers the responsibility, authority, freedom, training, and equipment they need to respond quickly to customer requests.

1.6 The Social Environment

Demography - The statistical study of the human population with regard to its size, density, and other characteristics such as age, race, gender, and income.

Managing diversity is creating a workplace that promotes inclusion and belonging.

1.7 The Global Environment

Global trade = Global competition

Uncertainty is considered by some ot be the biggest risk in business.

Two important issues in the global environment are the growth of global competition and the increase of free trade among nations.

The Ecological Environment

Climate change - One of the issues that has captures the most attention of the international business community.

Greening - Saving energy and producing products that cause less harm to the environment.

1.8 The Evolution of U.S. Business

Progress in the Agricultural and Manufacturing Industires

Technology has made modern farming efficient. The number of farmers dropped from 33% of the population to less than 1%, but the average farm size is now about 430 acres compared to 150 acres in the past.

The loss of farmworkers isn’t a negative sign. It indicates that the U.S. agricultural workers are the most productive worldwide.

The loss to society is minimized if the wealth created by increased productivity and efficiency creates new jobs elsewhere.

Progress in Service Industries

Before, the fastest-growing industrues in the U.S. produced goods. Now, the fastest growing ones provide services. Services employ about 85% of workers in the country. Also, there are more high-paying jobs in the service area.

Progress in the Information Age

In the Information Age, a significant portion of a company’s value is based on its intellectual capital.

Intellectual capital - Employee knowledge and skills that can be used to create new products, attract new customers, and increase profits.