Chapter 19: Factor Markets

Introduction

Factors of production: are the inputs that are used to produce a good or service. Land, labour, capital.

- when a bakery sells cookies it used land (where the bakery is), labour (bakers), and capital (the building and equipment).

- the market for factors of production is similar to the market of goods and services, but with one crucial difference: demand for a factor of production is a derived demand. Meaning that the demand for waiters is dependent on the demand for restaurant food.

The Demand for Labour

- supply and demand run the factor market like the goods and services market. The demand for doughnut shop workers determines the wage.

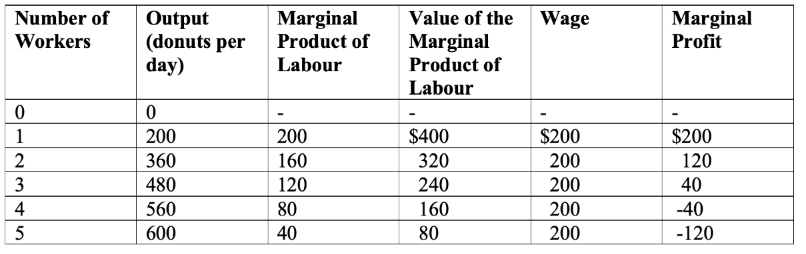

Example: Morgan’s doughnut shop

make two assumptions

- that assume that businesses are in a competitive market.

- the business is profit-maximizing. So Morgan’s shop doesn’t care how much production it produces or the workers it hires. They only focus on profits.

- to figure out how many workers to hire, a business must think about how the number of workers influences the amount it produces.

Production function: the relationship between the number of inputs a business uses, and the quantity of output it produces and sells.

- input in this example = the bakers, ingredients, capital.

- output = donuts

marginal product of labour: the increase in output that results from hiring one more worker. - the marginal product of the second worker is 160 doughnuts.

Diminishing marginal product: the more workers you hire the less each new worker makes as there are limited resources and space to work in.

The Demand for Labour and the value of the Marginal Product of Labour

- When Morgan is thinking to hire another worker they are only looking at how much profit will increase, not how much more quantity will be produced.

- to find how much revenue will increase from hiring another worker we have to convert the marginal product of labour into the value of the marginal product. If a doughnut sells for $2 and a new hire can produce 160 doughnuts then that worker produces an additional $320 of revenue.

Value of the marginal product: the value of the additional output created by adding one more unit of input. Sometimes called the marginal revenue product.

}}Value of the Marginal Product of Labour (V M P L) = P x M P L}}

How many workers should Morgan hire?

- assume the wage is $200 per day. The first worker would create $200 of profit in a day. The second worker was $320, and the third was $40. Hiring more than three workers is unprofitable.

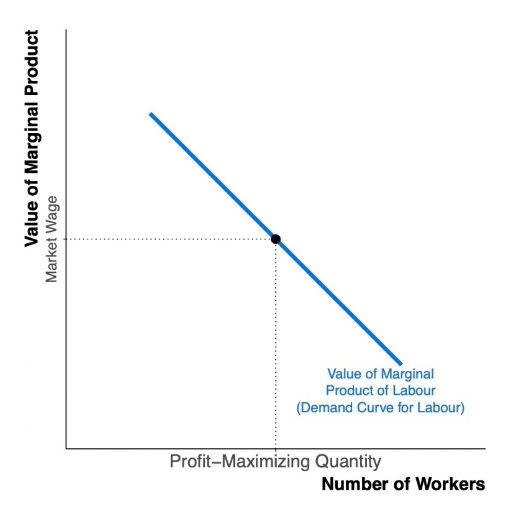

- A competitive business hires workers up to the point where the value of the marginal product = the wage.

- The value of the marginal product of labour is the labour demand curve for a competitive business.

Shifts in Labour Demand

- changes in wages (the price of labour/input) will cause a movement along the curve.

- When the output price changes, the value of the marginal product changes.

- technology

Labour-augmenting: technology usually helps workers increase their marginal product.

Labour-saving: technology lowers the marginal product of workers as it is a substitute for workers.

Work versus Leisure

leisure: any time spent not working.

- work and leisure are one of the biggest trade-offs

- The labour supply curve slopes upward. that means that workers react to a higher wage by working more hours.

- Not everyone’s labour supply curve is upward-sloping. if you get a wage increase of $20 to $200 the opportunity cost is higher, but you have more money to justify your leisure.

Shifts in Labour Supply

- labour supply shifts whenever the quantity supplied for labour changes due to a non-wage factor.

Changes in Preferences and Social Norms

- In 1953, 24% of Canadian women were employed or looking for a job. In 2019 the number increased to 62%.

- There were many reasons why the percentage increased but a major factor was social norms.

Change in opportunities

- Some will change jobs if there is a better wage or other motivation for them to do so.

Immigration

- the supply of labour rises in the country with the influx of new workers. And the supply of labour falls in the countries being left.

Equilibrium in the Labour Market

- Equilibrium looks similar to the market of goods and services. Price adjusts until quantity demanded = quantity supplied.

- Wage = value of the marginal product to have equilibrium

- any event that shifts the demand for labour will change the equilibrium wage and the value of the marginal product of labour since these must always be equal.

Example - More Labour

- imagine immigration increases the rates of workers who want to work in a doughnut shop. This will shift the supply of labour right.

- This creates a surplus of workers so the price falls the make the new equilibrium.

- This fall in wages makes it profitable to hire more workers. Then the marginal product of labour falls so then the value of the marginal product falls.

- At the new equilibrium, workers’ wages and the value of the marginal product are lower than they were before the arrival of new workers.

Example - More Demand

- Imagine new research shows doughnuts are healthy, increasing demand for doughnuts.

- The price of doughnuts will quickly rise. This does not increase the value of the marginal product of labour.

- The higher price of doughnuts allows businesses to hire more workers. Which shifts the demand for labour right.

- Now there is a shortage of workers so the wage will increase.

- Increased wages attract more workers and encourage workers to work longer hours.

- conclusion: prosperity in the market is usually linked to the prosperity of workers in that market.

Other Factor Markets: Land and Capital

- Not only do businesses have to decide how many workers to hire and their wages. They also have to decide where they will have their business, the size of the business, and the equipment. (land labour, capital)

Capital: anything human-made that is used to produce a good or service.

Equilibrium in other factor markets

- there are two different kinds of prices: rental and purchase price.

rental price: the price someone pays to use a factor for a given amount of time:

purchase price: the price someone pays to own a factor for an unlimited amount of time.

- assuming this is a competitive market and each business is maximizing profit, then each factor will be paid in a rental price equal to the value of the marginal product.

- The marginal factor of a product depends on how much of it is being used.

- if a factor’s supply changes it not only changes its rental price but other the rental price of other factors as well.

- If the supply of equipment falls the equilibrium falls as well.

- But not only will equipment fall, but if there is less equipment then workers will be less effective. So a decrease in equipment will make the demand for workers fall, which will lower the workers’ wages.