2.5 - sustainability, management accounting, & responsible leadership ll

learning outcomes

discuss the effects of current environmental and sustainability issues and their impact for organisations, management control and responsible decision making

explore some of the broader developments that are shaping management accounting in response to changing environmental, social and governance [ESG] concerns

evaluate the impact of ESG on familiar management accounting practices and techniques and the way in which they are adapting to integrate wider concerns

discuss the impact of ESG for management control and management control processes

last week recap

last week we outlined developments in the wider context of accounting and management accounting that are shaping developments in sustainable reporting and sustainable management accounting

we argued that given organisational leaders and decision-makers increasingly need to direct organisations towards sustainability, management accounting information needs to be used to inform sustainable and responsible decisions

this information will help us better understand our resources and is particularly important in terms of assessing and steering organisational performance

information can help organisations to reduce their environmental impact, develop good organisational activities, understand dependencies and contribute to long term shared value

management accounting and control tools are developing to integrate sustainability issues

management accounting systems not only shape internal decision-making, but they help to measure a firm’s contribution to sustainability – quantifying expected performance and risks

performance measurement and management systems help enact purpose, translating sustainability strategies into plans and objectives

management accounting tools and techniques to encompass sustainability

1 - material flow cost accounting [MCFA] for a circular economy

Tracing and Quantifying material flows and stocks within manufacturing processes, might include raw materials, energy, water and waste

assessing material and financial flows for environmental and

economic goals through resource efficiencysystemic examination of material flows in this way helps managers

to identify wasteit could be argued that more detailed environmental cost

information in turn has financial efficiency benefits toopotentially improve environmental performance in terms of energy

consumption, CO2 emissions, and waste produced

what is the circular economy

“in a circular economy, things are made and consumed in a way that minimised our use of the worlds resources, cuts waste and reduces carbon emissions products are kept in use for as long as possible, through repairing, recycling, and redesigning, so they can be used again and again'“

at the end of a products life, the materials used to make it are kept in the economy and used wherever possible, the european parliament explains

how companies might use MCFA

MCFA helps organisations understand material flows in and out of the organisation, identifying inefficiencies and waste

MCFA can reduce energy used in production

gives visibility to material and energy use throughout the production lifecycle providing companies with opportunities for recycling and reusing materials

design product more eco-efficiently

reusing materials also reduces the need for new materials

2 - sustainable investment appraisal

embedding sustainability into capital investment decisions

how are decision-making criteria to be set, multi-criteria analysis?

potentially using sustainable investment appraisal tools to calculate the impact [either positive or negative] on natural, social, or human capital

it is important to incorporate non-financial knowledge and evaluation criteria into sustainable capital budgeting [frost and rooney, 2021]

sustainable investment appraisal decisions e.g. investment in wind farm energy - consider environmental impact, social impact, financial returns and risk

“IGPG promotes the need for project and investment appraisal to facilitate long term decision making and to incorporate sustainability-related considerations. organisations with explicit sustainable value-creating strategies typically emphasise

techniques such as DCF and real options and downplay the role of other short-term

measurement criteria, such as payback and earnings per share (EPS) growth” - (International Good Practice Guidance, IFAC, 2013)

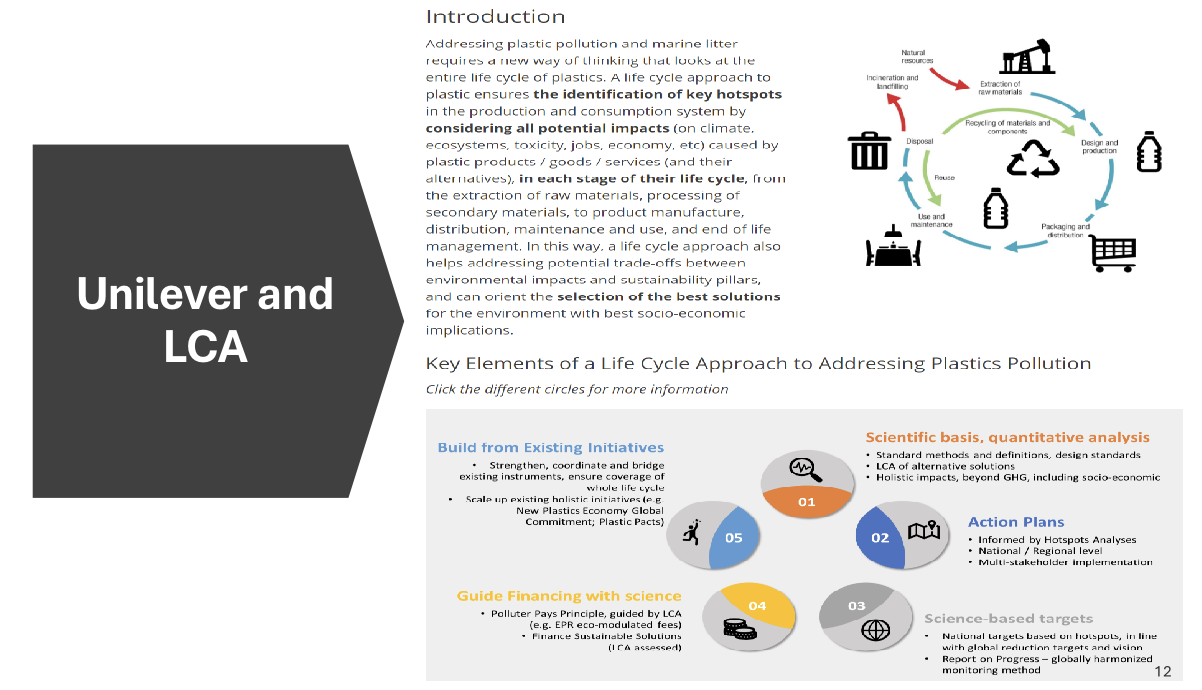

3 - life cycle assessment

examine the impacts of products, services and processes

LCA is a method to quantify total sustainability impact, resource use and environmental damage, over the life of a product from inception to end

records the inputs and outputs of a product/service and its related impacts - helps identify where are the risky stages in the product life cycle in terms of sustainability

but preparing a comprehensive LCA is not that straightforward, with complexity of suppliers, users, retailers - so this might be difficult to do across product/service ranges

4 - sustainability budgeting

using budgets to communicate sustainability objectives just as it is used to communicate financial objectives

budget inclusion of broader resources, such as natural resources also signals their importance to the organisation, and helps establish benchmarks for monitoring performance

variance analysis [e.g. budgeted emissions] - flexing budgets to calculate environmental variances

green budgeting: government & public sector

OECD guidelines

aligning public budgets with climate and environmental objectives

helping to embed and track Net Zero emissions targets

drawing on budget policy making tools to integrate climate and environmental issues into budget decision making

5 - sustainable activity analysis

examining activities to produce goods and services to assess, for example, inefficient use of environmental resources

breaking down activities to understand how they impact the environment, use of resources and sustainable performance

activity analysis and activity based management help mangers allocate resource use - water, energy, raw materials - to specific activities to better understand the direct and indirect costs associated with activities as well as helping to provide information for better management of this resources

6 - performance measurement systems and sustainability

integrating sustainability into key performance indicators - can influence organisational culture and enhance performance

use of KPI’s is familiar territory for organisations in evaluating how targets are being achieved

we’ve seen the use of complex KPIs in this area, such as balanced scorecards with sustainability perspectives

KPIs can be effective in guiding organisations in particular decisions so well devised and integrated KPIs could contribute to shaping decision making across the organisation

however, we have seen before the limitations and behavioural issues of performance measurement

sustainability is also inherently complex with interconnections of social, economic, environmental, ethical concerns which makes it difficult to devise appropriate KPIs

e.g. how to use balanced scorecards & sustainability

its now argued that this approach of adding an additional perspective is too simplistic and whilst it may increase visibility of environment/sustainability, it may not be sufficiently integrated with other objectives and its significance may be affected

sustainability scorecard in additions to the BSC?

better yet, integrating sustainability into all 4 of the original perspectives?

some factors to consider - which metrics should be used, how, and why?

qualitative and quantitative information - recurring issues as we have seen before, how to translate some objectives into measurable criteria, e.g. human rights, employee well-being? difficulties in quantifying impacts

relative and absolute numbers - using relative numbers might signal improved performance comparatively but in absolute terms could still mean poor performance in consumption of resources. might be misleading

timescales - sustainability indicators tend to produce lagging information, based on what has already happened. long term forward looking information is essential to sustainability

issues and challenges of using MA tools for sustainability

accounting tools tend not to foster decision-making for long-term effects of environmental impacts and accounting, is often notoriously short-term in orientation - but sustainability and ethical, environmental problems, such as climate change, poverty, have long-term horizons

complexity of boundaries between internal and external facets of the organisation are not always easy to delimit (Bouten and Hoozee, 2013) – for example it might be tricky to assess how a company’s supply chain impacts on its environmental performance

the majority of traditional non financial performance measures focus on internal processes while the largest share of environmental measures focus on effects outside the boundaries of the organisation

overemphasis on quantitative data and capturing quantitative data – but this may overlook critical qualitative aspects e.g. local communities and social effects

ensuring sustainable MA is embedded and not on the periphery

trying to ensure that traditional financial based MA does not dominate when it comes to decision making

how well integrated are sustainability related MA tools [in relation to BSC discussion]

implementation issues

having sustainability MA tools has no bearing on how effectively they are bing used

relevance of measures and indicators used to evaluate performance in terms of sustainability

an integrated approach to SDGs and management control

if improvements in social and environmental performance are to translate into long term shareholder value, firms need to ensure that associated activities are fully integrated into strategic processes and translated into goals and objectives [Arjales and Mundy, 2013]

how do management control systems help in the integration of sustainability within organisational strategy? simply adapting performance measurement systems such as balanced scorecards is insufficient. sustainability needs to be embedded into organisational strategy [Beusch et al. 2022]

Arjales and Mundy (2013) highlight why and how organisations could use their MCS to achieve strategic change, drive sustainability strategy and achieve their strategic objectives. the paper suggests that businesses are unlikely to extend CSR activities beyond that which benefits their investors’ and as such might fall short of the transformations required for a more sustainable society

management control systems and sustainability

note that some of research on sustainability and management control systems tends to utilise Simon’s Levers of Control (see readings on LC)

sustainability can be integrated into belief systems – this can drive sustainability efforts by embedding them into company culture. sustainability can be reinforced by measures and metrics using diagnostic and interactive controls (Gond et al., 2012). boundary systems can create a baseline and clear rules about sustainability compliance

in organisations where the profit-seeking logics dominate, management control systems may be insufficient to see radical change (Narayanan and Boyce, 2019)

don’t forget that some of our previous issues with management control and management control systems remain relevant

summary and reflections

despite the slow start, there are many developments in sustainability and management accounting practice and literature

implicit assumptions about the relevance and ability of management accounting practices to contribute to data collection and achievement of sustainability goals

diagnostic/Results based sustainability controls may provide only a partial picture and if not well-integrated could end up being siloed

but embedding sustainability into organisations through belief systems can help shape organisational cultures and steer managerial decision-making

performance measurement systems can help connect corporate purpose to societal and environmental aims

ambitious targets and strategic objectives do not necessarily translate into actions

some concerns about the limitations of management accounting to address sustainability challenges