MRU - Elasticity and its applications

Elasticity of demand

- The law of demand tells us that when price goes up, quantity demanded goes down and viceversa.

- But how much does quantity demanded change when price changes?

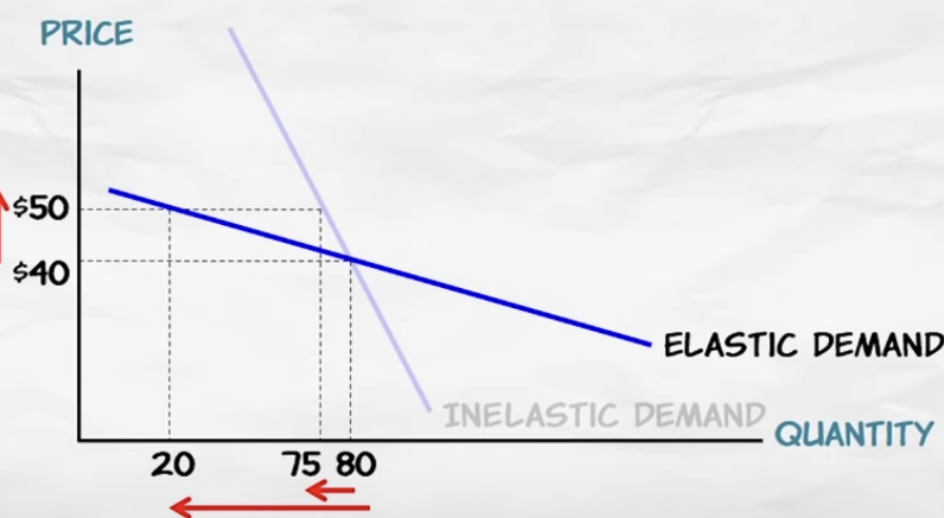

- A demand curve is said to be elastic when an increase in price redices que quantity demanded a lot.

- When the same increase in price reduces quantity demanded just a little, then the demand curve is inelastic.

- Elasticity is a measure of how responsive quantity demanded is to a change in the price.

- Elasicity is not the same as slope

- Flatter is more elastic

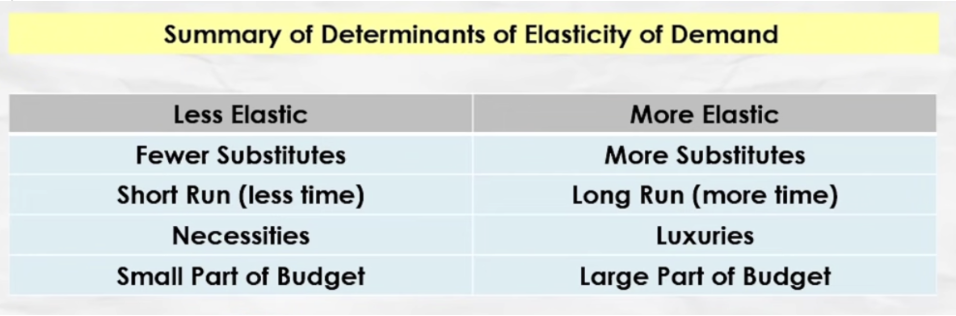

- Factors that determine elasticity:

- availability of substitutes: this is the fundamental determinant. the more substitutes the more elastic

- for goods with many substitutes, switing brands when price change is easy, so demand is elastic

- time horizon: immediately following a price increase, consumers may not be able to alter their consumption patterns, making demand inelastic

- over time, however, consumers can adjust their behavior by finding substitutes

- the longer the time horizon, the more ability to adjust

- category of product: the broader the classification, the more likely they are able to find a substitute, making it inelastic

- necessities vs luxiries: for necessities, consumers do not change quantity demamnded much when the price changes.

- purchase size, relative to the consumer's budget: consumers are less concerned about price changes when the good feels cheap, making demand inelastic. they might not even notice if it goes up.

Calculating elasticity of demand

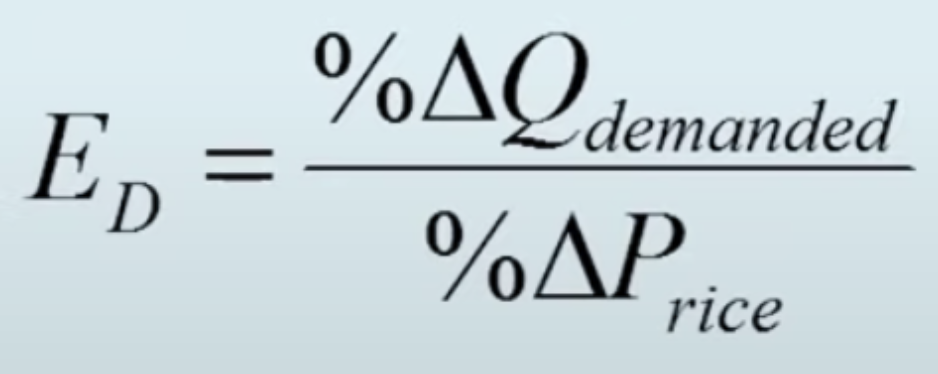

- Elasticity of demand: percentage change in quantity demanded divided by the percentage change in price.

- Ed < 1, inelastic

- Ed > 1, elastic

- Ed = 1, unit elastic

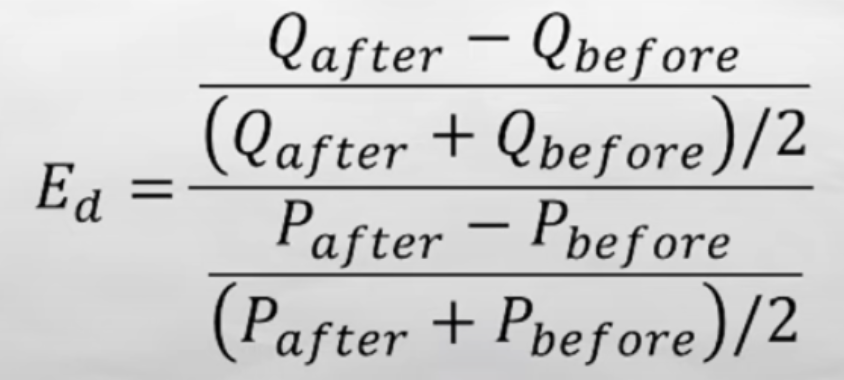

- Midpoint formula:

- A firm's revenues are equal to price times quantity sold

- revenue = price * quantity sold

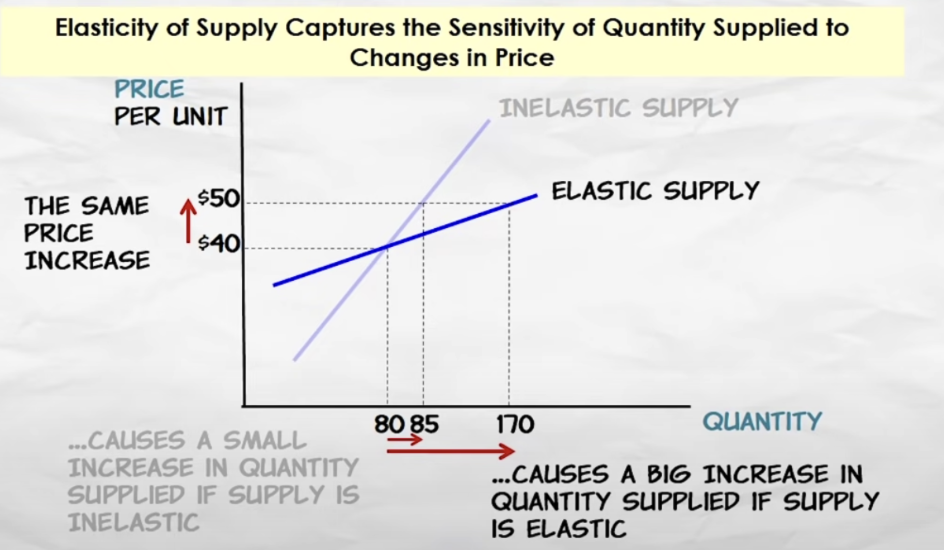

Elasticity of supply

- Elasticity of supply: how responsive the quantity supplied is to a change in price

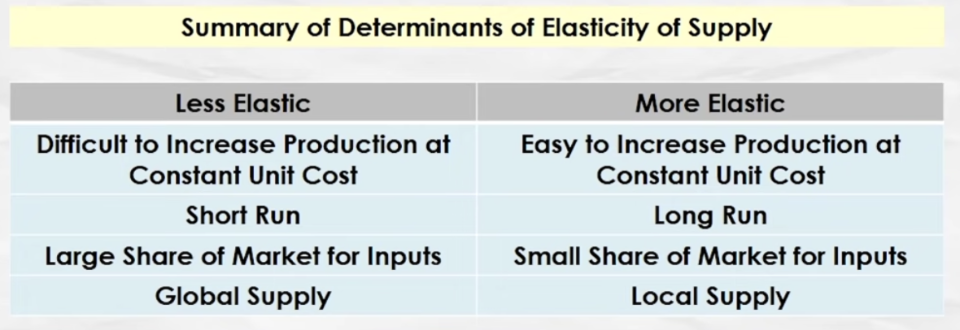

- determinants of elasticity of supply

- change in per unit costs with increased production: this is the main determinant if increased production requires higher csots, then the supply curve will be inelastic

- time horizon: immediately following a price increase, producers can expand output only using their current capacity, making supply inelastic

- share of market for inputs: supply is elastic when the industry is a small demander in its input markets because supply can be expanded without causing a big increase in the demand for the industry's inputs.

- example: we can double the supply of toothpicks without making a much bigger demand for wood

- geographic scope: the narrower the scope of the market, the more elasstic its supply

- we use the midpoint formula to calculate it too.