Unit 5: Factor Markets

(5.1) Intro to Factor Markets

factor market graphs convey same info from units 1-4, just looks at products in a factor perspective

households own factors of production

h earn income by selling factors in resource market (EX: selling labor for wages)

marginal revenue product (MRP): extra revenue that firm gains when firm hires 1 additional worker/resource

formula: P * MR (change in revenue) = MRP

true whether product market is perfectly/imperfectly competitive

marginal factor or resource cost (MFC or MRC): additional cost paid by firm when it hires additional worker/resource

EX: wage for labor

MRC = TFC (price) / additional Q (usually +1)

MRP = MRC → MR = MC (profit maximizing quantity)

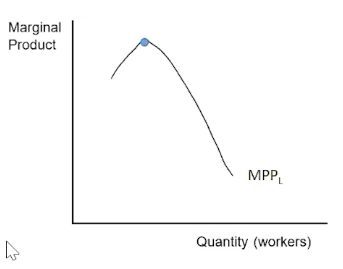

total product: amount produced with given amount of workers

marginal product: change in total product that results in an additional worker/resource

table indicators:

increasing returns = increasing marginal product

diminishing returns = marginal product decreases (or diminishes)

negative returns = marginal product is a negative integer

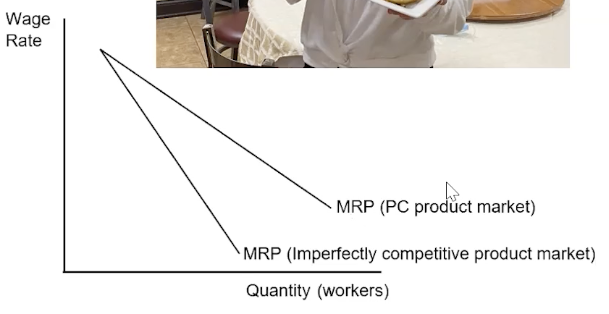

in perfect competition:

P (price) = MR means perfectly competitive product market

MP * MR = MRP is the same as MP * P = VMP (value marginal product) in perfect competition

in imperfect competition:

downward sloping demand curve → firm needs to lower the price to sell additional units

TP (total product) is Q

P * Q = TR (total revenue)

change in TR with 1 additional worker is MRP

P > MR → MRP is focused on

MRP = (change in TR) divided by (change in quantity of labor)

(5.2) Changes in Factor Demand/Supply

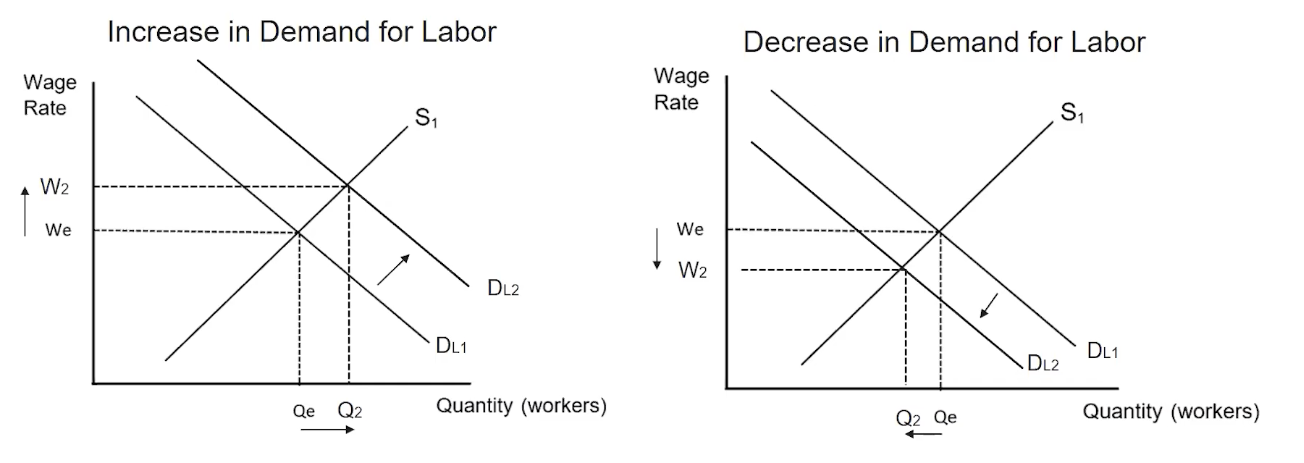

derived demand: demand of resource from product demand

effects: productivity (MPP) and output price (MRP)

MPP (marginal physical product) = change in total product / change in quantity (usually +1)

MRP (marginal revenue product) = MPP * MR

diminishing returns = output increases at a decreasing rate (MPP decreases) with additional input

demand determinants → MR

change in number of consumers

price of related good

increase if more expensive, decrease if not

government regulations

decreases productivity of workers → decreases demands

improvements in education

increase productivity of workers → increases demand

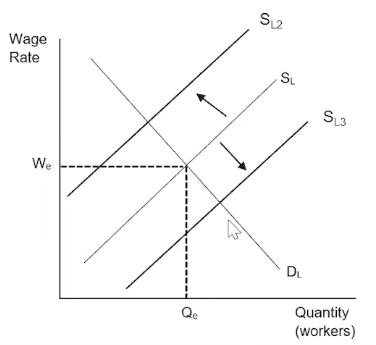

5 supply determinants

leisure (choosing not to work)

opportunity cost for work

increase in leisure → less in supply

number of alternative options

decrease in supply of one industry → increase in supply of another

age distribution

more retiring workers → less new workers entering

education

more years spent at universities → decrease in supply of labor

changes in skill levels

immigration

increase in immigration → increase in workers (vice versa)

(5.3) Profit-Maximizing Behavior in Perfectly Competitive Factor Markets

wage takers: workers that are selling labor at set price

perfectly competitive supply curve

TFC (total factor cost) = Q of workers * wage rate

MFC or MRC = change in TFC / change in Q

wage rate (W) = supply curve (S) = MRC

perfectly elastic (horizontally straight)

imperfectly competitive firm

MRP < perfectly competitive MRP

least-cost rule: rule that minimizes costs/maximizes profits

minimizing costs formula: (MP of capital / P of capital) = (MP of labor / P of labor)

if ratios aren’t equal, remember diminishing marginal returns and figure out which to increase/decrease

similar to utility maximization

diminishing marginal returns is the diminishing marginal utility here (less is more)

inputs considered in least-cost rule can be complements and substitutes

type of worker + type of produce is perfectly competitive → MRP = VMP (value of the marginal product)

VMP is hence MP of labor * P

MR → P (from equation MP * MR = MRP)

(5.4) Monopolistic Markets

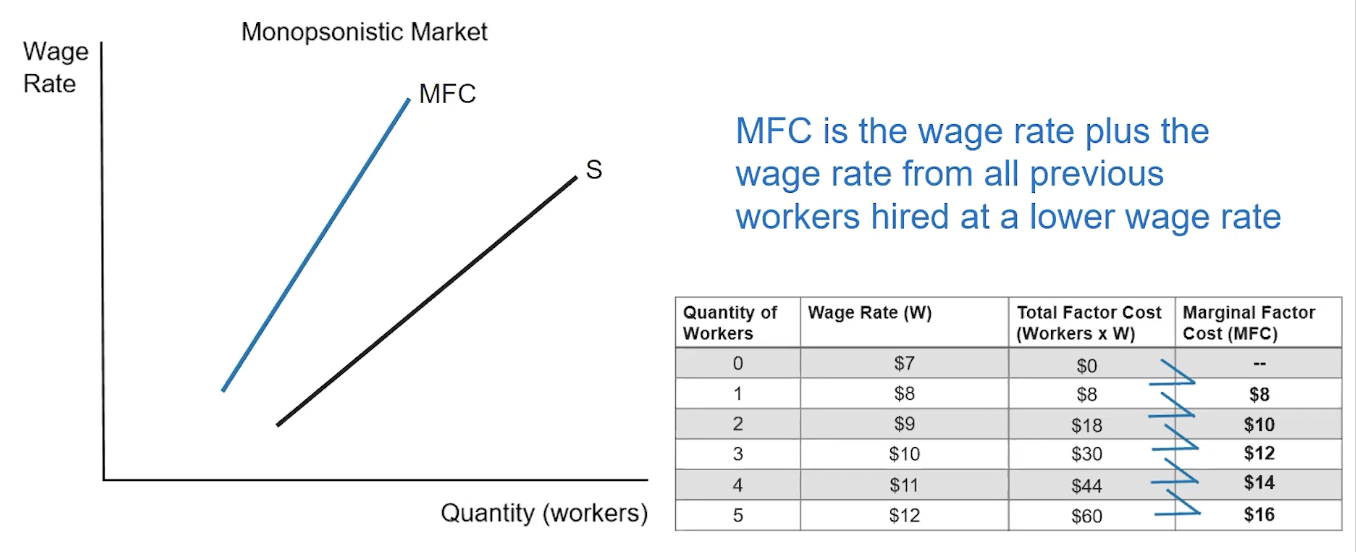

monopsony: market where there’s a single buyer (aka monopsonist)

one firm is hiring labor → control over wage rate (wage maker)

MFC > supply (S) = wage rate (W)

MFC = wage rate of ALL workers (wages of previous workers get raised to match the additional one)

profit maximizing monopsony (optimal quantity of workers): MRC = MRP

MRP = demand

wage: intersection of supply and profit maximizing line (Q of workers)

vs a perfectly competitive market

monopsony graph is just pc market + MFC curve

pays lower wages + hires fewer workers

is not allocatively efficient and produces DWL