Notes on Standard Costing and Variance Analysis

Standard Costing and Variance Analysis

Learning Objectives

Explain operation and purpose of a standard costing system.

Set standard costs and understand standard hours produced.

Calculate variances for labor, materials, overhead, and sales margins; reconcile actual profit with budgeted profit.

Identify causes of variances.

Introduction to Standard Costing

Standard costing is a system for budgeting and control in organizations, especially in repetitive production processes.

Applicable in manufacturing and service industries with measurable outputs.

Distinction between standard costs (predetermined target costs) and budgeted costs (total expected costs for an activity).

Operation of a Standard Costing System

Repetitive Operations: Most effective in contexts where input and outputs can be defined (e.g., manufacturing).

Sales Variances: While not usually included in standard costing, they can also apply to service centers.

Standard Costs: Developed from historical data or engineering studies. Should accurately reflect efficient operations.

Historical Data: Draws on past performances; risk of inefficiency.

Engineering Studies: Aimed at establishing optimal resource specifications.

Variance Analysis

Variances indicate the difference between standard and actual performance, highlighting areas needing attention.

Variances can be categorized as:

Price Variances: Differences in expected costs due to price changes.

Usage Variances: Differences caused by excess or inefficient use of resources.

Total Variances: Overall performance metric compared to budgets.

Standards and Cost Components

Direct Material Standards: Defined by the amount and cost of raw materials.

Direct Labor Standards: Based on hours needed to produce goods, factoring in normal delays.

Overhead Standards: Established for fixed and variable components, often tied to direct labor or machine hours.

Standard Cost Card: Summarizes all these costs for individual products and operations.

Standard Hours Produced

The measure of efficiency that allows for combining production results across different outputs. Examples from production processes illustrate its use.

Example Measurement: If producing Product X takes 5 hours for 100 units, we'd expect $5 imes 100$ hours of labor standardized.

Purposes of Standard Costing

Cost Prediction: Helps forecast future costs, aiding decision-making.

Performance Targets: Sets benchmarks that motivate employees.

Budget Preparation: Makes developing budgets easier through consistent cost information.

Control Mechanism: Pinpoints deviations from standard performance.

Cost Tracing: Facilitates tracking costs for product profitability and inventory valuation.

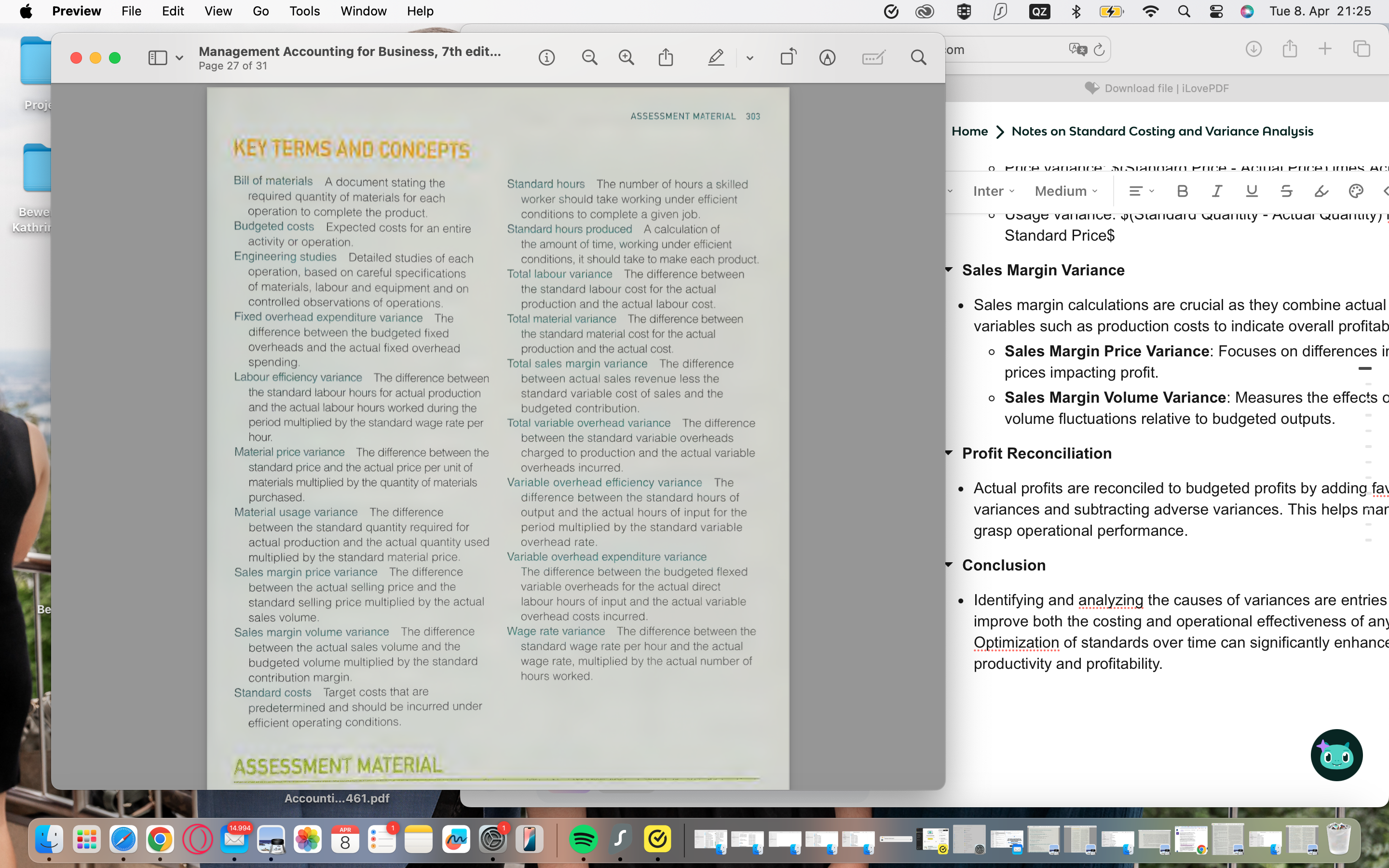

Calculation of Variants

Labour Variances:

Wage rate variance: $(Standard Rate - Actual Rate) imes Actual Hours$

Efficiency variance: $(Standard Hours - Actual Hours) imes Standard Rate$

Material Variances:

Price variance: $(Standard Price - Actual Price) imes Actual Quantity$

Usage variance: $(Standard Quantity - Actual Quantity) imes Standard Price$

Sales Margin Variance

Sales margin calculations are crucial as they combine actual sales with variables such as production costs to indicate overall profitability.

Sales Margin Price Variance: Focuses on differences in selling prices impacting profit.

Sales Margin Volume Variance: Measures the effects of sales volume fluctuations relative to budgeted outputs.

Profit Reconciliation

Actual profits are reconciled to budgeted profits by adding favorable variances and subtracting adverse variances. This helps management grasp operational performance.

Conclusion

Identifying and analyzing the causes of variances are entries to further improve both the costing and operational effectiveness of any organization. Optimization of standards over time can significantly enhance both productivity and profitability.