3.3 Revenue, costs and profits

Revenue

Total revenue = Quantity sold x price

OR Average revenue x output

Average revenue = Total revenue / quantity

Marginal revenue = Change in TR / Change in Quantity - the change in a firms revenue from selling one extra unit of output

Maximising revenue occurs when MR = 0

Elasticity

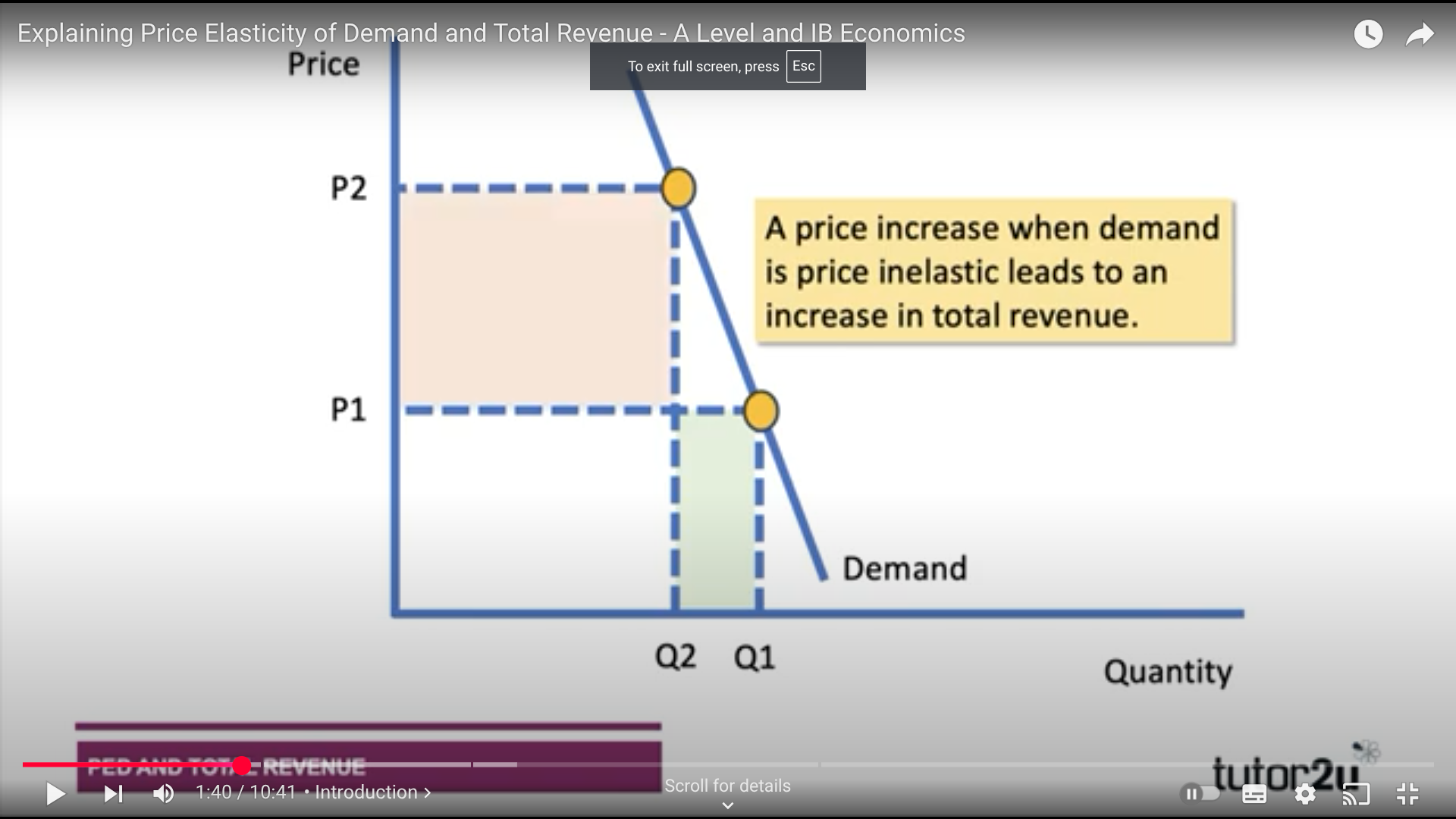

When demand is price inelastic then a price rise will mean a business will increase their total revenue as the fall in QD will be less than proportional to the rise in price

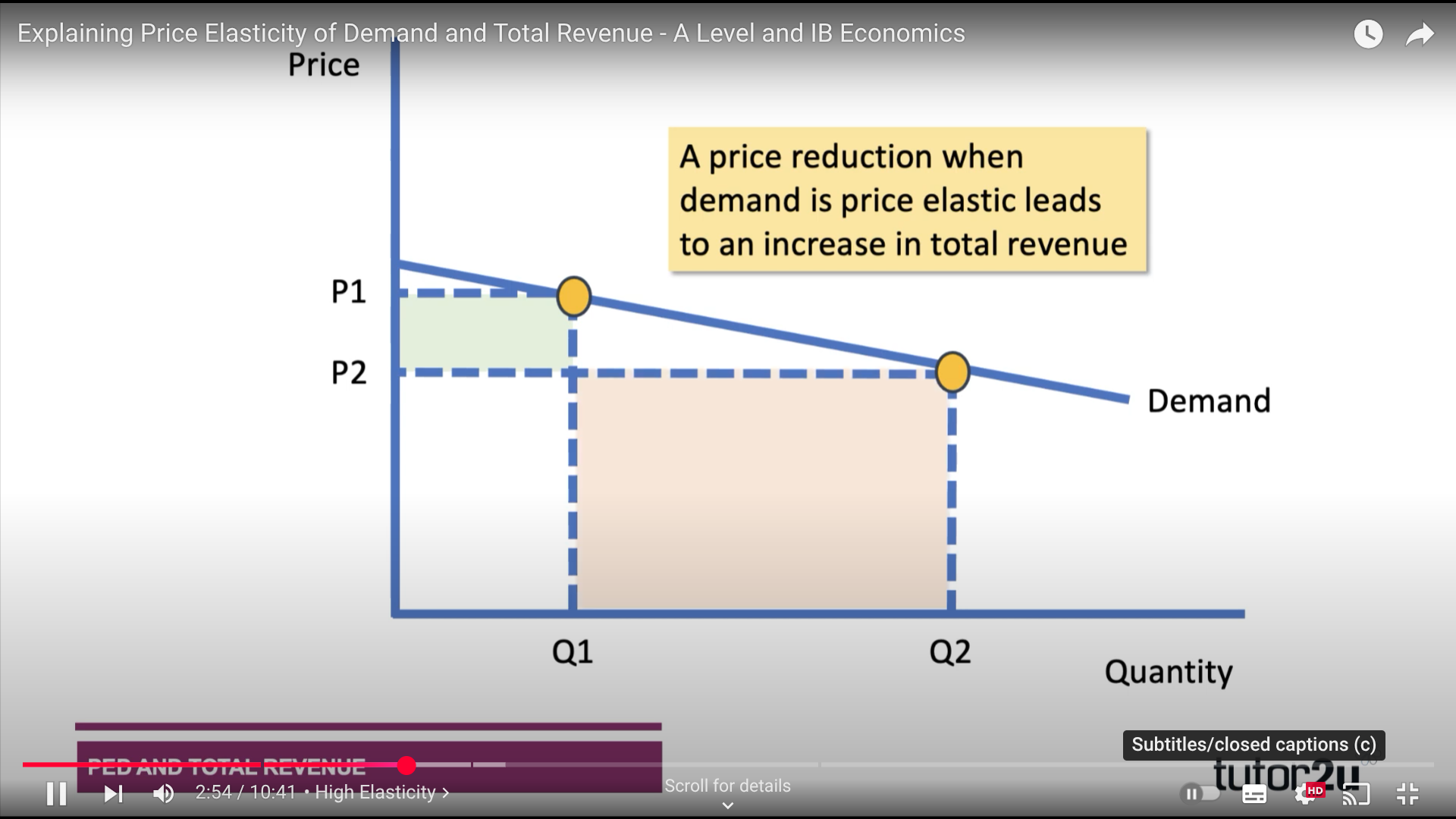

A price reduction in a product with high elasticity of demand will increase TR

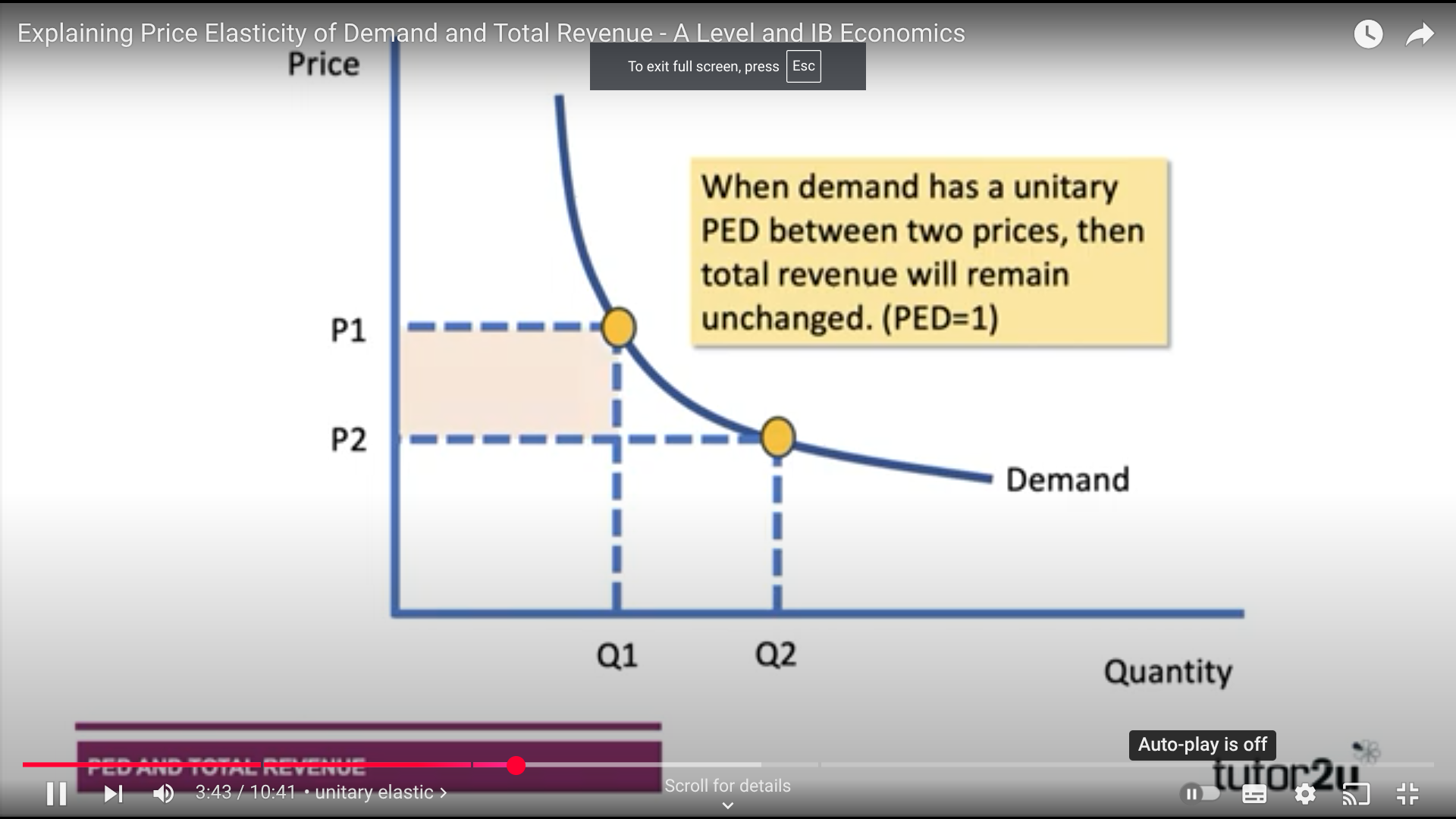

When PED is unitary then TR will remain unchanged

Price maker = a firm with the ability to alter prices due to market power

MR is less than AR because to sell additional units the price of all units must be lowered

Price taker = A firm with no market power, selling as the market price only

MR = AR because every unit sold is at the exact same price

TR is upward sloping with a constant gradient

Costs

Short run = a period of time where at least one factor of production is fixed

Long Run = All factors of production are variable

Fixed costs = Costs that do not directly vary with output i.e. rent, salaries and interest on loans

Variable Costs = Costs that do directly vary with output i.e. wages, utility bills, raw material costs

Total Fixed Costs

Average Fixed Costs - TFC / Q - AFC decreases with output so downwards sloping

Average variable costs - U shaped - at lower output levels output rises faster than TVC and at higher output levels rises slower than TVC

Average total costs = AFC + AVC

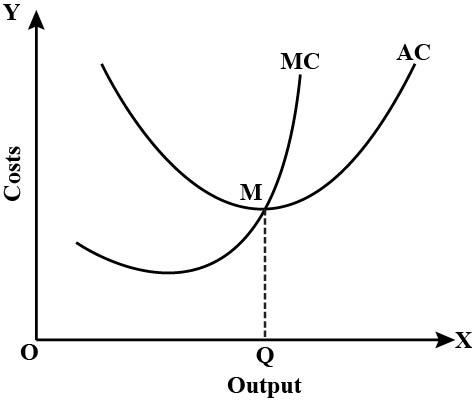

Marginal and Fixed Costs ( Short Run )

MC = the total change in total costs when output increases by one unit

Calculated by the change in costs / Change in output

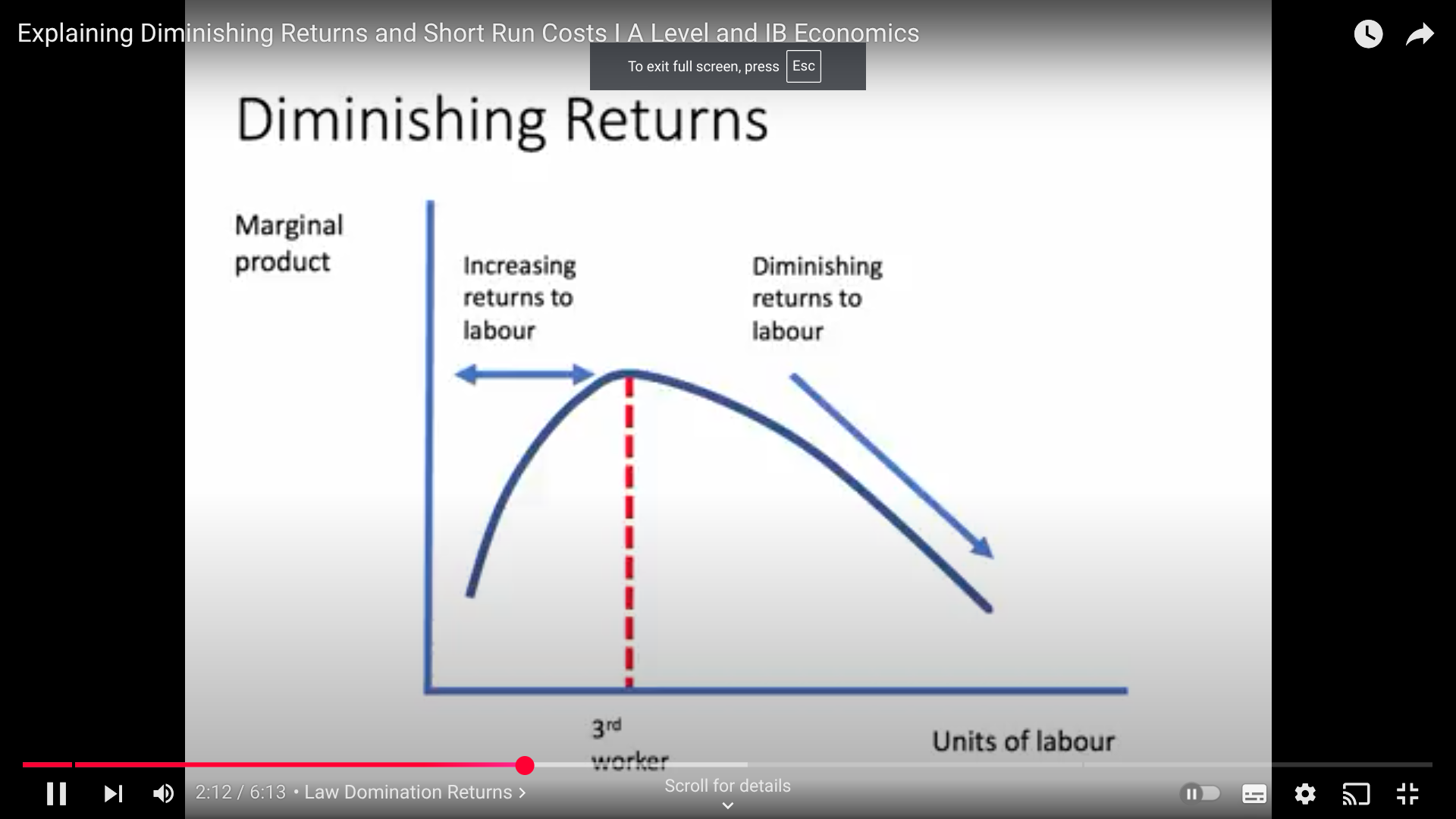

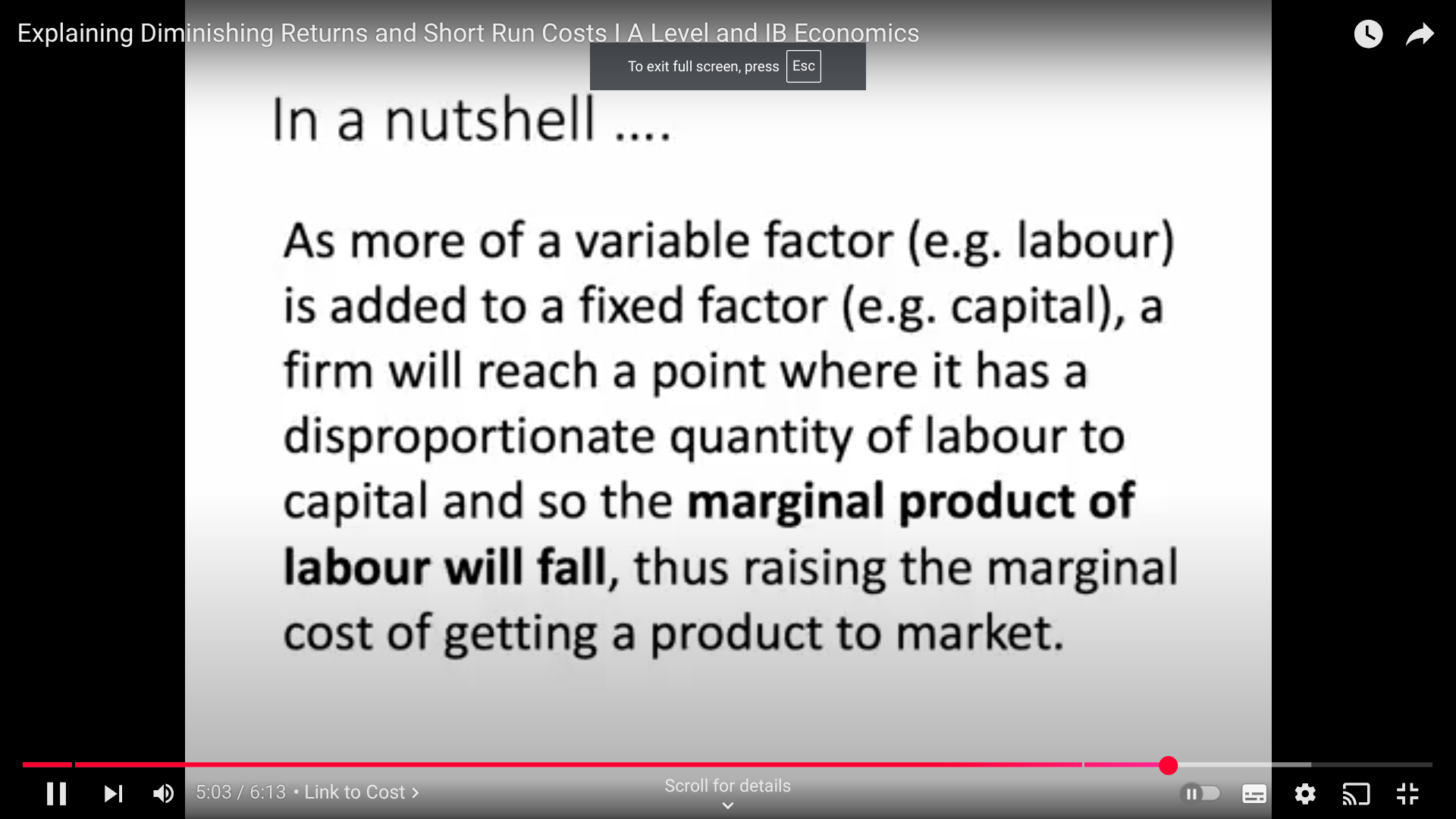

The law of diminishing returns:

States that as more units of variable factors are added to fixed FoP output will rise at first then fall

This is because capital becomes more scarce and marginal product ( change in output from one extra worker ) falls causing MC to rise

The law of diminishing returns causes a fall in marginal product of labour

This causes average product to fall

Which then causes AVC and MC to rise

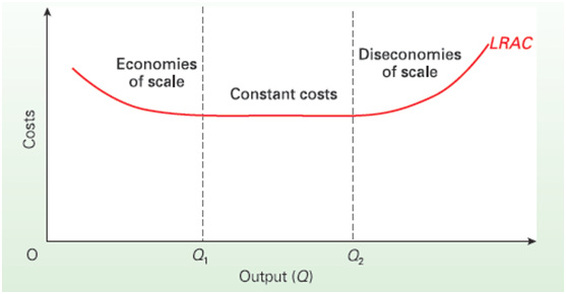

Long Run Average Costs

Assume that all FoP are variable

Economies of scale = % output > % input

Constant costs = % output = % input

Diseconomies of scale = % output < % input

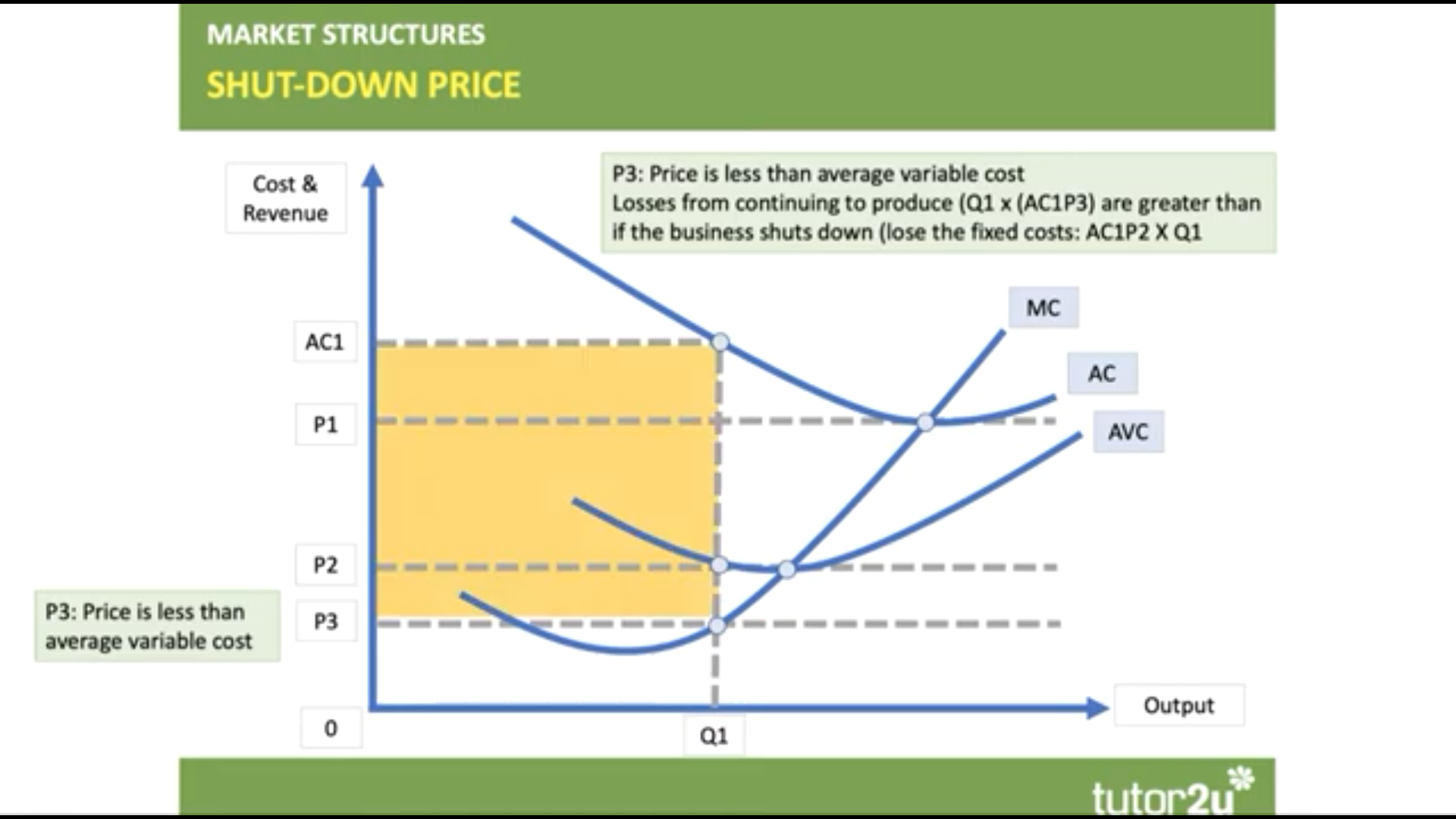

Shutdown point

In the short run firms will continue to produce output so long as price per unit is equal to or greater than AVC

Price = Min AVC = shut down point in a competitive market

In the Long Run a business needs to make atleast normal profit this is where just enough is made to keep FoP in their current use

Firms may be able to survive whilst making a loss due to profit saticficing or just an economic downturn i.e. travel in the pandemic - this may be cross subsidised in other areas