lecture 2: statement of financial position/income statement

statement of financial position

• Aka balance sheet

• Provides a “snapshot” of financial position at a point in time

• Key components:

▪ Assets: resources held by the company

▪ Liabilities: what the company owes to parties apart from the owner(s)

▪ Equity: what is left for the owner(s) after liabilities are settled

• The accounting equation:

Assets = Equity + Liabilities

Assets

An asset is a resource held by a business. To be included in the SoFP as an asset, a resource must possess all of these characteristics:

▪ Being an economic resource

▪ Under the control of the business

▪ Can be measured in monetary terms

Money measurement

Some economic resources cannot be faithfully measured in monetary terms and thus,

cannot be recognised as assets on the SoFP.For example:

• Human resources (except in certain limited circumstances, such as football

clubs)

• Internally generated goodwill (e.g., a reputation for high-quality products, good

customer relationships)

• Internally generated product brands (e.g., brand image, trademark)

Classification of assets

Assets can be categorised as either current or non-current.

current assets

Definition: short-term held assets, which meet any of the following conditions:

❖ Held for sale/consumption during normal operating cycle

❖ Expected to be sold within a year after the date of the relevant SoFP

❖ Held for trading

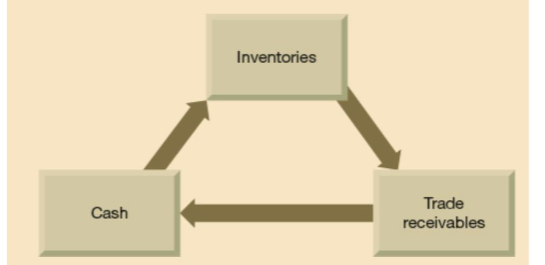

❖ Cash or near cash such as easily marketable, short-term investmentsExamples: inventories, trade receivables (amounts owed by customers for goods or

services supplied on credit), and cashthe circulating nature of current assets:

Non-current assets

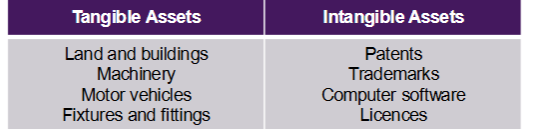

Definition: long-term held assets which do not qualify as current assets

• Aka fixed assets

• May be tangible (i.e., physical) or intangible (i.e., nonphysical)Examples:

current vs non-current

The classification depends on the nature of the asset and the business.

For example, a motor van retailer will normally hold inventories of the motor vans for

sale; it would, therefore, classify them as part of the current assets. However, a

business that buys one of these vans to use for delivering goods to customers (that

is, as part of its long-term operations) would classify it as a non-current asset.

Equity and Liabilities

A claim is an obligation to provide cash, or some form of benefit, to an outside party.

There are two types of claim against a business:

▪ Equity: the claim of owner(s). Note that a business is viewed as being separate

from its owner(s) for accounting purposes.

▪ Liabilities: the claim of other parties, apart from the owner(s). They involve an

obligation to transfer economic resources (usually cash) as a result of past

transactions or events.

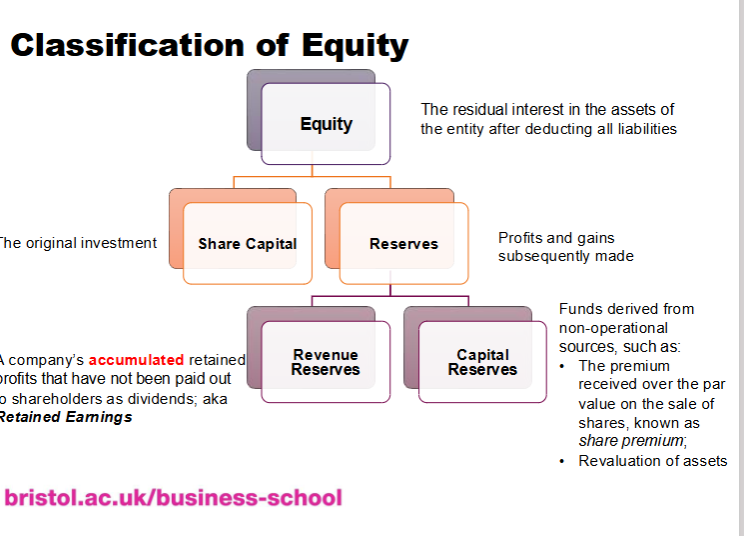

classification of equity

classification of Liabilities

Liabilities can be categorised as either current or non-current.

current Liabilities:

Definition: amounts due for settlement in the short term, which meet any of

the following conditions:

❖ Expected to be settled within the business’s normal operating cycle (e.g.,

accrued salaries)

❖ Exist primarily as a result of trading (e.g., trade payables)

❖ Due to be settled within a year after the date of the relevant SoFP (e.g.,

bank overdrafts)

❖ No right to defer settlement beyond a year after the date of the relevant

SoFP (e.g., a bank loan that must be repaid within 12 months)

Non-current Liabilities

Definition: amounts due that do not meet the definition of current liabilities

▪ Example: long-term loans (borrowings from banks or other financial institutions

where the repayment is due over a period longer than one year)

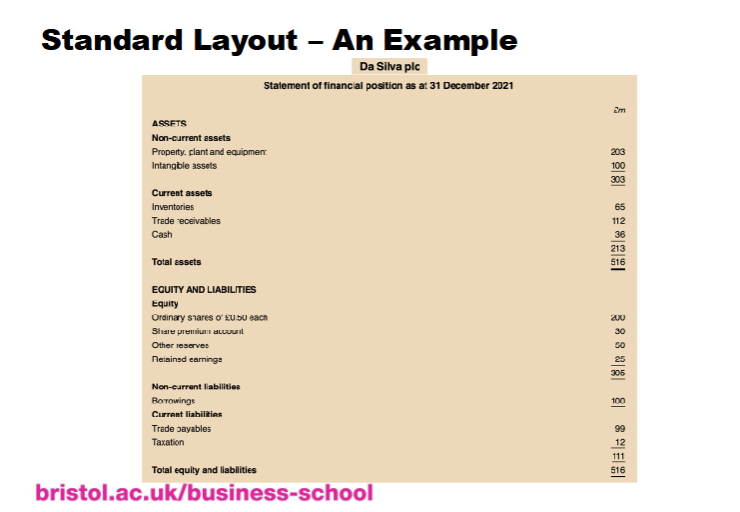

statement of financial position

why is the SoFP useful?

Assessing overall financial health

Showing how the business is financed and how its funds are deployed

Providing a basis for valuing the business

Accounting conventions influencing the SoFP

Business entity convention (not the same as “limited liability”!)

• Treats business and owners as distinct entities for accounting purposes

• Ensures clear financial assessment, irrespective of legal business form

Historic cost convention

• Values assets based on historic cost (i.e., acquisition cost)

• Reliable but may not reflect current market values

Prudence convention

• Advocates caution in financial reporting

• Aims to prevent overstatement or understatement of financial strengthGoing concern convention

• Assumes business will operate in foreseeable future

• Important for asset valuation in financial difficultiesDual aspect convention

• Recognises that each transaction affects the business in at least two aspects

• Ensures that the SoFP will continue to balance

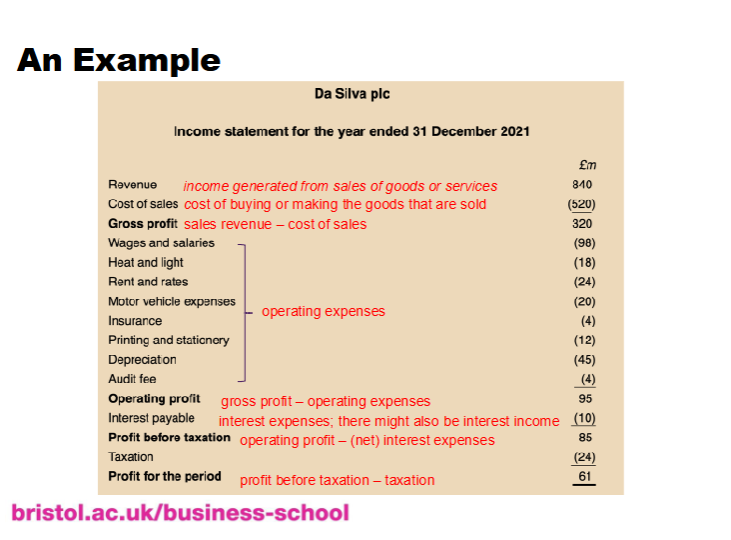

Income statement

Aka profit and loss account

Measures financial performance of a business over a period

Key components:

▪ Revenue: income generated from sales of goods or services

▪ Expenses: costs incurred to generate the revenue

• Equation:

Revenue – Expenses = Profit (or loss)

Why is the income statement useful?

the income statement shows:

How effective the business has been in generating wealth

How profit was derived

Revenue

Aka sales, sales revenue, turnover

Definition: income generated from sales of goods or services

Example: a smartphone retailer has sold 100 smartphones at a price of £500 each

during the period.

Revenue = 100 Smartphones Sold x £500 per Smartphone = £50,000

Revenue recognition

Accruals convention: revenue is recognised when earned (i.e., control of the

goods/services is transferred to the customer), regardless of when cash is received.Revenue is NOT the same as cash received!

▪ Cash sales: sales is recognised when cash is received

▪ E.g., you buy a coffee at Caffè Nero for £3, paying cash at the counter. Caffè Nero

recognises the £3 as revenue when the coffee is handed over to you.

▪ Credit sales: sales is recognised before cash is received

▪ E.g., Caffè Nero orders coffee beans from a supplier worth £1,000. The supplier

delivers the beans today but allows Caffè Nero to pay in 30 days (credit terms). The

supplier recognises the £1,000 as revenue today as the control of the coffee beans

has been transferred to Caffè Nero, even though the payment will be received later.

Expense recognition

Accruals convention: expenses are recognised when incurred, regardless of when cash

is paid.Expenses are NOT the same as cash paid!

Example: Electricity Bill

Caffè Nero receives its electricity bill for December 2024 for £500, but the payment is

not due until end of January 2025. Even though the payment will be made in January,

the £500 expense is recorded in December 2024 because that is when the electricity

was used (the expense was incurred).

cost of sales

Aka cost of goods sold

Definition: cost of goods that are sold during the period

Some goods bought during the period may remain as inventories at the end of the

period.In some businesses, the cost of sales for each individual item is identified at the time of

sale; however, this is not practical for many businesses.Calculation of CoS:

Cost of Sales = Opening Inzventories + Purchases – Closing Inventoriesthese are sometimes shown directly on the income statement

Matching convention: expenses should be matched to the revenue that they helped

to generate.

• Example below: the cost of sales was the cost of inventories that were sold, not the

whole cost of inventories that were available for sale during the period.

accruals accounting

Profit = Revenue – Expenses

(not Cash Receipts – Cash Payments)