Lecture 7 - Privatisation

Definition

Privatisation is the transfer of ownership and/or control of a state-owned enterprise (SOE) to the private sector.

It can involve:

Full sale of assets

Partial sale (share flotation)

Contracting out

Public–private partnerships

Major UK programme: 1980s–1990s under Margaret Thatcher.

2. Why Governments Privatise (Arguments For)

A. Productive Efficiency

Private firms:

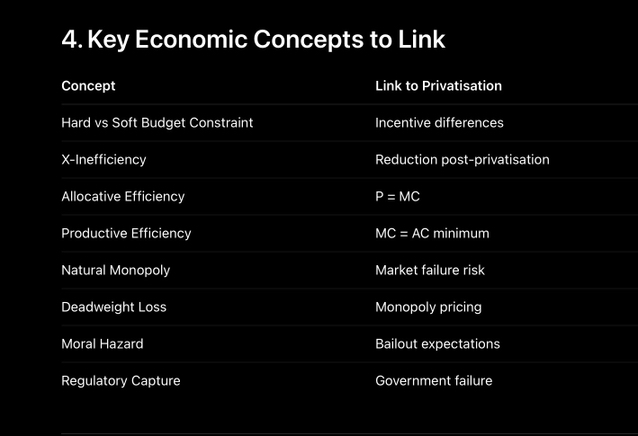

Face hard budget constraints

Must minimise costs to survive

Risk bankruptcy if inefficient

State firms may face soft budget constraints (concept by János Kornai).

Result: Lower average costs, reduced X-inefficiency.

B. Profit Incentives & Managerial Discipline

Privatisation introduces:

Shareholder monitoring

Performance-based incentives

Corporate governance mechanisms

Reduces:

Overstaffing

Political interference

Bureaucratic slack

C. Dynamic Efficiency (Innovation)

Competition + profit motive →

Investment in R&D

Technological improvement

Quality enhancement

Example: British Telecom experienced increased competition and expansion after privatisation.

D. Fiscal Benefits

Government gains:

Immediate revenue from asset sale

Reduced borrowing requirement

Lower public sector debt (short-term)

E. Increased Competition

If combined with deregulation:

Entry increases

Prices fall

Output rises

Potential movement toward:

P ≈ MC (allocative efficiency)

F. Wider Share Ownership

Privatisation programmes sometimes aim to:

Develop capital markets

Encourage household investment

Promote “shareholder capitalism”

3. Arguments Against Privatisation

A. Natural Monopoly Risk

Industries with:

High fixed costs

Large economies of scale

Privatisation may simply replace:

Public monopoly → Private monopoly

Private monopolist:

Restricts output

Raises price

Creates deadweight loss

Example: Rail infrastructure under Railtrack, later replaced by Network Rail.

B. Higher Prices

Private firms maximise profit, not welfare.

Can lead to:

Price increases

Reduced cross-subsidisation

Lower affordability

Example: Energy sector criticism of British Gas.

C. Equity Concerns

State firms may:

Protect employment

Provide universal access

Support rural regions

Privatised firms may:

Cut unprofitable services

Focus on high-income areas

→ Increased inequality.

D. Under-Provision of Merit Goods

Where:

Social Benefit > Private Benefit

Private market underprovides:

Transport

Water

Infrastructure

E. Short-Termism

Private firms may:

Prioritise dividends

Underinvest in long-term infrastructure

Focus on quarterly performance

Particularly risky in capital-intensive sectors.

F. Regulatory Failure

Privatisation often requires:

Price caps

Competition authorities

Industry regulators

Risk of:

Regulatory capture

High monitoring costs

Government failure

6. Evaluation Framework (High-Level Analysis)

Privatisation works best when:

Market is competitive

Entry barriers are low

Demand is elastic

Externalities are minimal

Strong independent regulation exists

Privatisation works worst when:

Industry is a natural monopoly

Service is a merit good

Equity concerns are significant

Information asymmetry is high

Regulation is weak