Income Tax Provision

Fundamentals

GAAP and TAX are 2 different entities

the revenue recognition is different

Gaap = pretax financial income → Income tax expense

this is what would be on their books based off of their revenue recognition

in this chapter we will take the pretax financial income and turn it into TAXABLE INCOME

the process goes as so;

TAX= Pretax financial income → account for permanent and temporary differences (explained later) → TAXABLE INCOME → income tax Payable

Income taxes payable is a LIABILITY on the BALANCE SHEET

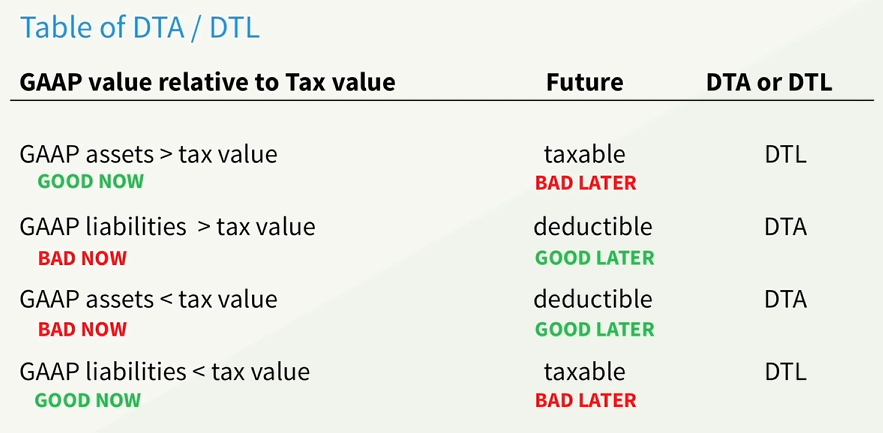

DTA AND DTL

overview

The difference between the the income tax expense and taxable income tax payable is known as a DEFERRED TAX AMOUNT

in this example, the excess difference is a deferred tax ASSET.

in this example, the excess difference is a deferred tax ASSET.

When the TAX EXPENSE is greater than the tax payable that means that the company has essentially OVERPAID on taxes, meaning that they will have a the money set aside to pay the remaining tax in the future already, no longer taken out of revenue going forward —- this is a Deferred tax ASSET or DTA

DTA AND DTL’s are TEMPORARY DIFFERENCES

this means that even though the book (gaap) and tax don’t line up doesn’t mean that they will never line up about this topic

NON TAXABLE AND NON DEDUCTABLE are permanent differences- book and tax will never line up on these because they will never be REVERESED like a DTA OR DTL

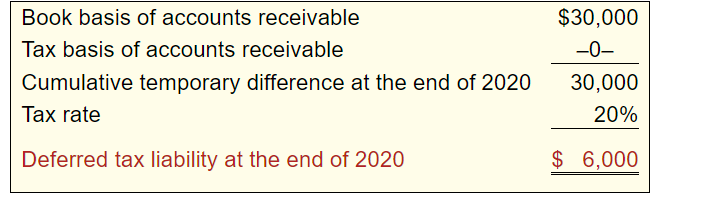

in book terms: A temporary difference is the difference between the tax basis of an asset or liability and its reported (carrying or book) amount in the financial statements, which will result in taxable amounts or deductible amounts in future years

Taxable amounts increase taxable income in future years

Deductible amounts DECREASE taxable income in future years

DTL

A DTL represents the increase in taxes payable in future years as a result of taxable temporary differences existing at the end of the current year

we accounted for LESS then the actual taxable amount was

we didn’t set aside the money for the tax NOW but will need to pay it LATER resulting in a deferred LIABILITY

this will now be communicated into the balance sheet accounts

this will now be communicated into the balance sheet accounts

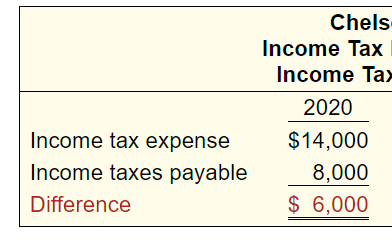

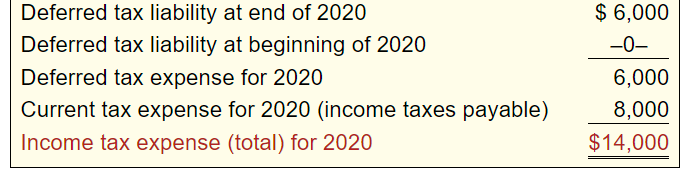

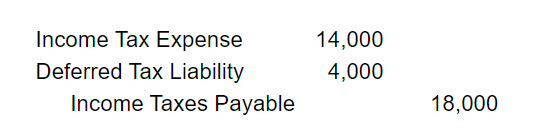

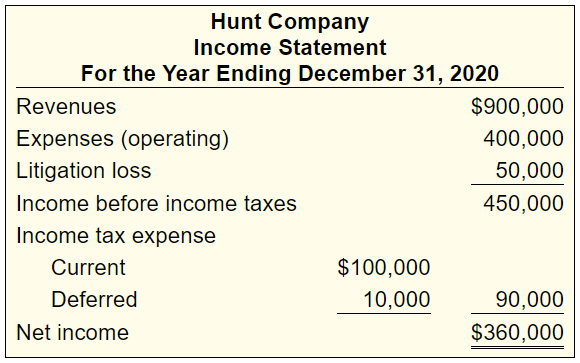

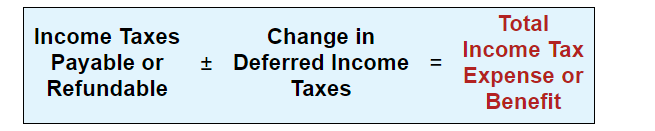

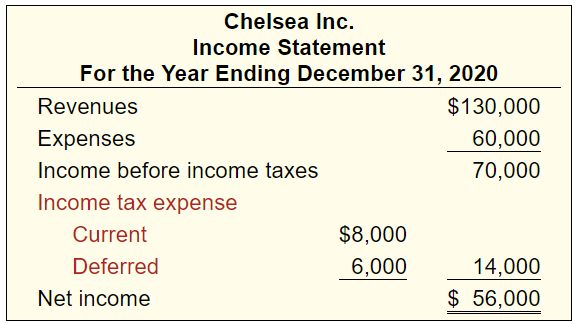

the income tax expense has two components

the income tax expense has two components

current tax expense ( income tax payable for this period)

deferred tax expense (the deferred liability DTL increase in this period

this is an ORIGINATING ENTRY

this is an ORIGINATING ENTRY

DTL | ||

|---|---|---|

2020 | 6,000 | |

2021 | 4,000 | |

2022 | 2,000 |

at the end of 2021 dtl is 2,000 meaning that 4,000 was added in making the journal entry thus

at the end of 2022 dtl is 0 meaning that 2,000 was added in to the dtl account effectivity 0ing out the t account, making the journal entry thus

at the end of 2022 dtl is 0 meaning that 2,000 was added in to the dtl account effectivity 0ing out the t account, making the journal entry thus

WARRANTY DEDUCTION IS NOT ALLOWED TO BE DEDUCTED UNTIL PAID

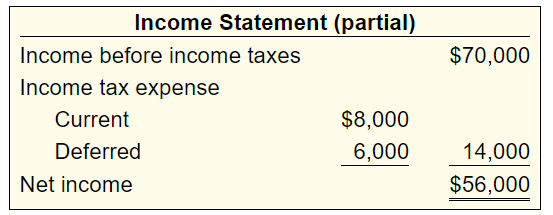

Income statement and balance sheet presentation

BALANCE SHEET

Income Taxes Payable is a CURRENT LIABILITY

deferred tax liability is a NONCURRENT LIABILITY

INCOME STATEMENT

DTA

A DTA is represents the increase intaxes refundable (or saved) in the future

in essence, you OVERPAID now so you dont have to pay later

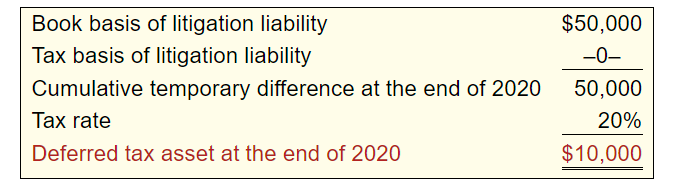

you CANNOT deduct litigation expense until you settle the litigation

litigation creates a DTA because you account for it NOW but tax it LATER meaning you overpay

this is what the journal entry looks like

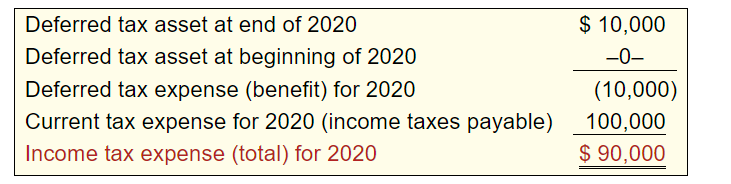

INCOME STATEMENT AND BALANCE SHEET

INCOME STATEMENT AND BALANCE SHEET

balance sheet

Income taxes payable is recorded as a current liability and DTA is reported as a noncurrent asset

Income statement

DTA | ||

|---|---|---|

2020 | 10,000 | |

2021 | 10,000 |

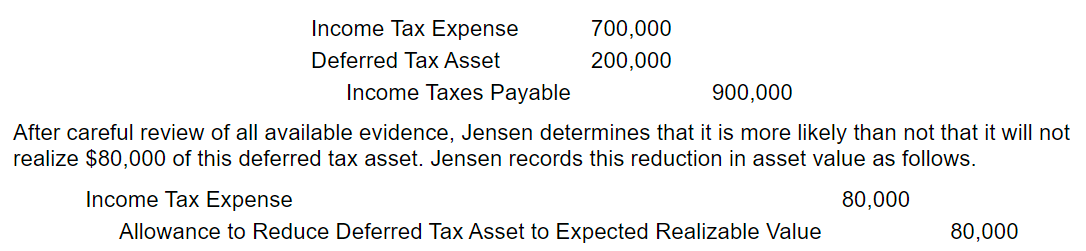

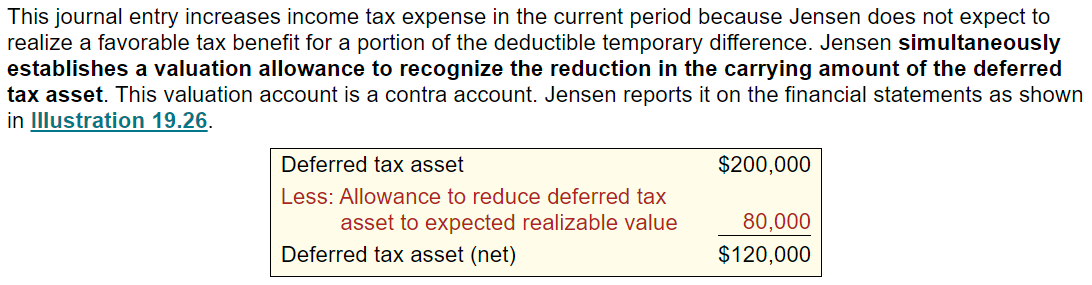

DTA VALUATION ALLOWANCE

A company should REDUCE a DTA by a VALUATION ACCOUNT if based on available evidence when it is more likely than not that whey WILL NOT REALIZE some portion or all of the deffered tax asset (proibability of more than 50%)

Income tax expense increases because they DO NOT expect to recoup a portion of the DTA

Income tax expense increases because they DO NOT expect to recoup a portion of the DTA

on the balance sheet at the end of the year the allowance to reduct dta is then reevaluated if it is expected to not realize 50,000 instead of 80,000 the reversing entry will go like so

on the balance sheet at the end of the year the allowance to reduct dta is then reevaluated if it is expected to not realize 50,000 instead of 80,000 the reversing entry will go like so

obj 2 : ADDITIONAL ISSUES

Income Statement Presentation

a company ADDS an increase in a deferred tax liability to income tax payable

a company a company SUBTRACTS an increase in an deferred tax asset from income taxes payable

The income statement should disclose relevant components of the tax expense

The income statement should disclose relevant components of the tax expense

Income tax expense is also often referred to as “provision for income taxes”

Income tax expense is also often referred to as “provision for income taxes”

Specific differences

temporary vs permanent differences

Temporary Differences

Deductible temporary differences are temporary differences that will result in deductible amounts in future years when related book liabilities are settled

Revenues and Gains are taxable AFTER they are recognized in financial income.

an asset may be recognized for revenues or gains that will result in tacable amounts in future years (DTL) when the asset is recovered

Sales accounted on accrual for GAAP but on Installment basis for TAX

in accounting you recognize the sale immediately even though you haven’t received the money yes (in a receivable)

in taxes you only pay the taxes when you ACTUALLY get the money meaning that you will pay taxes on on the money when you get it in the future

THIS IS A DTL because you have to recognize income in the future when you’ve already written it off your report

Contracts under percentage of completion for GAAP but related to gross profit for tax

in accounting you gradual recognize the revenue

in tax you pay taxes on the money you actually received

this could result in BOTH a DTL and DTA

DTL you recognized revenue for GAAP earlier than you recognize it for TAX making this a DTL you havent recieved the money yet so you pay money LATER

DTA you RECIEVE the money BEFORE you complete it then it is recognized for TAX you pay now making it a DTA

Investments accounted for under the equity method for GAAP and under the cost method for TAX

for GAAP you show you’re share of stands profits or losses

for tax you pay money that you’ve received as dividends

DTL the investment makes a profit but they have received no dividends, then its a DTL you will be taxed for this LATER

DTA if you LOSE money on the investment and haven’t received the dividend than you do not receive the tax benefit from having had a lost you will receive this BENEFIT LATER

Gain on involuntary conversion of nonmonetary asset for GAAP but deferred for TAX

insurance reimbursement recognized on gap but not on TAX immediately so you will owe taxes on this gain in the future

Unrealized holdings gains for financial reporting purposes ( including use of fair value) but deferred for tax purposes

collecting something, you recognize the value in GAAP

TAX you don’t recognize the value until you SELL it

OWEING in the future is a DTL

Expenses or losses are deductible after they are recognized in financial income

A liability (or contra asset) may be recognized for expenses or losses that will result in deductible amounts in future years (DTA) when the liability is settled

Product warranty liabilities

you have a warranty on a product RIGHT NOW so you set aside the money, you can only count it as an expense in the future when you actually payout the warranty. this is a DTA you will receive the benefits of this more in the future

Estimated liabilities related to discontinued operations or restructurings

when you are closing a store you set aside money to close the store for GAAP

for TAX you actually count the expenses when you spend them on closing the store

this is a DTA as you experience the benefit LATER

Bad debt allowance for GAAP vs. write off method used for tax

for GAAP you set aside an allowance for bad debt when you think a customer is not going to make there payment this then increases your ewxpenses HOWEVER

for tax you only realize the bad debt when you have INCURED IT meaning they will NOT pay you back, then this is a DTA

Lititgation accruals

whilst ins a litigation you expense it for GAAP but for tax you expense it when the litigation period is COMPLETED this is a DTA

Stock based compensation expense

for GAAP you count giving your employee stock as an expense when it is given but for tax you account it as an expense when they EXCERSIZE the right to the stock

EXCERCISE -= is when you actually use the stock option not just offered it

Unrealized holding losses for financial reporting purposes including use of the fair value option but deferred for tax purposes

when you have a loss on your investment but havent sold them you you record as a loss for gaap

for tax you record as a loss when you SELL them in the FUTURE this creates a DTA

Revenues or gains are taxable before they are recognized in financial income

An advanced payment is recognized when the money is given for tax purpose but recognized overtime for GAAP purpose

Subscriptions received in advance

because you pay the tax on it NOW you don’t have to pay it later this is a DTA

Advance rental receipts

because you pay the tax now you don’t have to pay it later this is a DTA

Sales and leaseback for financial reporting purposes (income deferral) but reported as sales for tax purposes

sales and leasebacks allows the company to turn the asset into cash while still gaining value from the use of the asset.

TAX will recognize the sale when it is made while making a DTA

GAAP we didnt consider it a sale because we are still using it

Prepaid contracts and royalties received in advance

if you recieve money for a contract in advance you recognize the money NOW on TAXES so you dont pay the tax later, this is a dta

for GAAP you record when you complete the task

Expenses or losses are deductible before they are recognized in financial income

The cost of an asset may have been deducted for tax purposes faster than it was expensed for financial reporting purposes. Amounts received upon future recovery of the amount of the asset for financial reporting

Depreciable property, depletable resources, and intangibles.

the tax depreciates at a different rate usually leading to you having to pay more taxes later

Deductible pension funding exceeding expense

for gaap you write down the expense now

for tax you dont pay tax on the money that you are putting in BUT you pay tax on the money that when you are taking it out of your account LATET

TAXES LATER IS A DTL

Prepaid expenses that are deducted on the tax return in the period paid