CIE AS Level Accounting: Partnerships

Partnerships are a joint venture by two or more business owners. Together, they will run and finance a business in order to make (more) profits. Prior to the establishment of a partnership, its owners (known as partners) have to agree on the following aspects:

how much capital each partner will introduce

the roles each partner has in the running of the business

how profits will be shared

how assets and profit shares will change at the admission or dismissal of a partner(s)

i.e in the case of a partner leaving, retiring, or death, how will the business re-appropriate its assets?

how decisions will be made and disputes resolved

This is known as a partnership agreement. Should the partners decide not to draw up a partnership agreement, any disputes will be based on the Partnership Act of 1890. The Partnership Act states:

all partners must contribute the same amount of capital

no interest on capital will be given

no salaries will be given

interest on drawings will not be charged

the profits will be shared equally between partners

partners are entitled to 5% interest per annum on loans they make to the partnership

A limited partnership is where the limited partners are only liable to what they have contributed to the business; should any losses occur, the partners will only be responsible for a share of it. This is known as limited liability.

Limited liability: owners/shareholders are only responsible for any losses based on the nominal value of their investment

Unlimited liability: owners are responsible for all losses in the business’ day-to-day proceedings and can be liable to using personal assets to pay off its debts

The advantages and disadvantages of a partnership include:

Advantages | Disadvantages |

|---|---|

The capital invested by the partners is often more than can be raised by a sole trader | A partner doesn’t have the same freedom to act independently as a sole trader does; decisions may have to be agreed that may be a problem if the partners have different views on how the business should develop and operate |

Partners are likely to have a wider range of knowledge, experience, and expertise in running a business than a sole trader | Partners generally have ‘unlimited liability‘, which means that they are personally responsible for making good on all losses and debts of the business; this can extend to losing their personal assets |

A partnership may be able to offer a greater range of services to its customers (or clients) | A partner may be legally liable for the acts of the other partner(s), even if those acts were committed without all of the partners’ knowledge |

The business does not have to close down or be run by inexperienced staff in the absence of one of the partners; the other partner(s) will provide cover | |

All losses are shared by all partners |

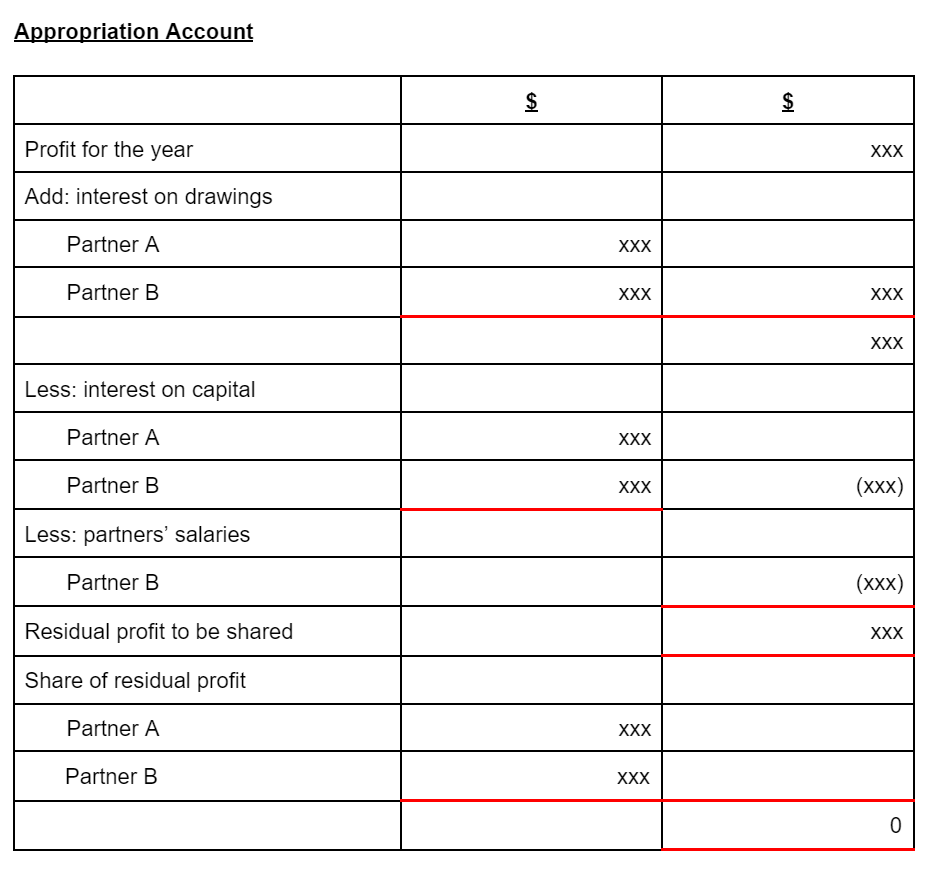

Partnership Appropriation Account

The partnership appropriation account divides the profit earned by the partnership for the year between the partners. It will look as follows:

Note: interest on loan to the partnership from a partner is not a distribution of net profit. It is to be debited to the income statement.

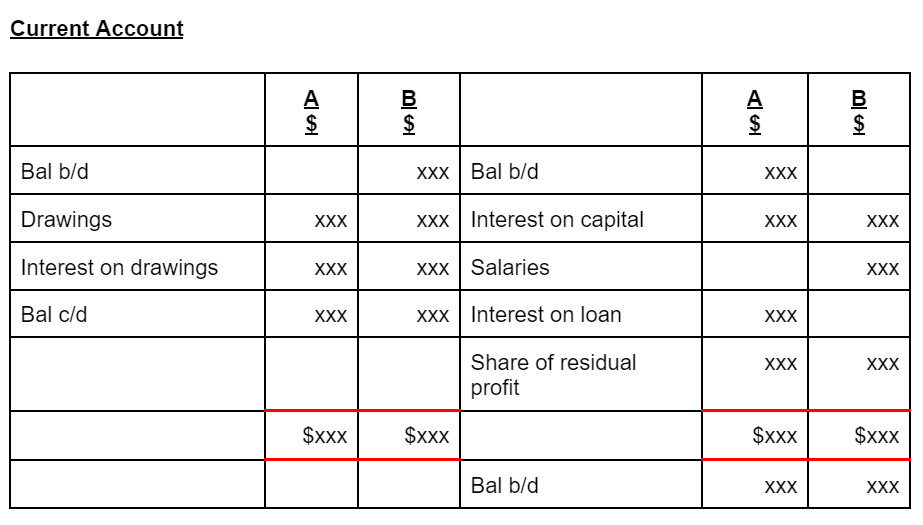

Current Accounts

The current account records shorter-term changes to the owners’ capital. This is where all information from the appropriation accounts will be entered.

Capital accounts are used to record longer-term changes to the owners’ capital. Any capital introduced by partners are recorded here

It is possible for the current accounts to have debit balancing; this suggests that the partner’s drawings were too large or they didn’t earn much in their share of the residual profit to cover their drawings.