Concept: Elasticity of Demand

Elasticity refers to how sensitive demand is to price changes:

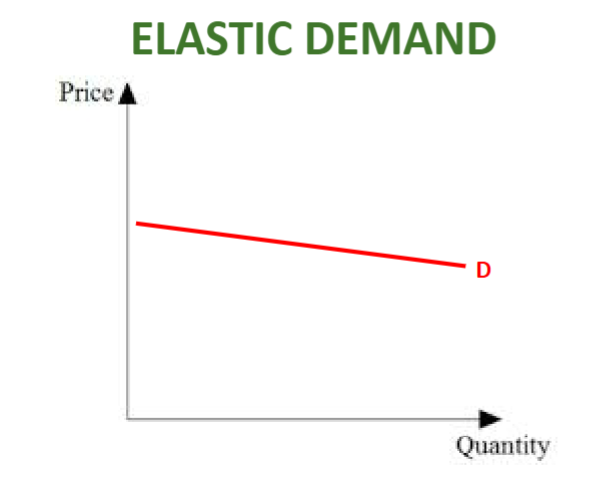

Elastic demand: Demand is very responsive to price changes. If the price drops, people buy significantly more; if the price rises, they buy significantly less. Examples: luxury goods, vacations, concert tickets, video games.

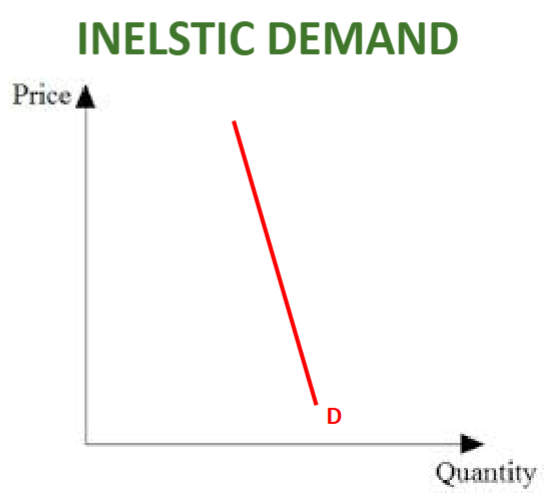

Inelastic demand: Demand does not change much with price fluctuations. Even if prices rise, people still need the product. Examples: gasoline, medicine, electricity, water, toilet paper.

Graphs:

Government Intervention in Markets:

Governments sometimes intervene in markets to protect consumers from extreme price exploitation, particularly when dealing with inelastic goods.

Price ceilings (e.g., rent control, limits on drug prices): Prevent prices from rising above a certain level. This can create shortages because suppliers are less willing to provide the good at a low price.

Price floors (e.g., minimum wage): Prevent prices from falling below a certain level. This can create surpluses (e.g., more workers seeking jobs than available jobs at higher wages).

Both of these tools prevent equilibrium price! (where how much suppliers are willing to invest meets how much people are willing to pay)

Preventing equilibrium is not necessarily a bad thing, but it does come with economic consequences along with the benefits.

Key Takeaways:

Elastic goods = people are price-sensitive, and demand is flexible.

Inelastic goods = people will buy regardless of price changes.

Government price controls (ceilings and floors) can fix one problem but create another, such as shortages or surpluses.