Money and Monetary Policy Practice Flashcards

Unit 9: Money and Monetary Policy Goals

Learning Objectives

Explain the three primary functions of money.

Articulate methods for measuring the supply of money.

Understand different types of debt and their operational mechanics.

Identify the roles and responsibilities of the central bank within the economy.

Explain how the process of financial intermediation determines the money supply.

Understand the components of a bank’s balance sheet.

Explain the role of the Federal Reserve in determining the money supply.

Understand the function of the federal funds rate and how it is determined using graphical analysis.

Understand the role of interest on reserves in the economy.

Explain the Fed's decision-making process for interest rate targets and the use of graphs to determine interest.

Understand the concept of quantitative easing.

Overview and Properties of Money

Definition of Money

Money is defined by its properties and functions rather than its physical form.

The Properties of Money

Medium of Exchange: This is what sellers generally accept and buyers generally use to pay for goods and services. It’s a form of trading because instead of people exchanging items for goods, people instead use a currency, to get goods.

A good medium of exchange needs to be:

Widely accepted by people

Easy to carry and use

Divisible (you can make change)

Reliable in value

Liquidity Property: money that can be quickly and easily used to buy goods and services without losing value.

Money is considered the most liquid asset because you can immediately spend it.

In economics, liquidity refers to how easily an asset can be turned into cash.

Store of Value: An asset that can be used to transport purchasing power from one time period to another.

Essentially, it is anything that can retain its purchasing power over time, allowing you to save it now and use it in the future.

Example: Money serves as a store of value because you can earn it today, hold onto it, and spend it later.

Disadvantage: The main disadvantage of money as a store of value is that the value of money falls when the prices of goods and services rise (inflation).

Unit of Account: A standard unit that provides a consistent way of quoting prices and recording debts.

It is basically a common standard used to measure and express the value of goods, services, and assets.

Example:

Imagine you go shopping and see:

A shirt costs $20

A backpack costs $50

A laptop costs $800

Because all prices are measured in dollars, you can easily compare their values.

The Types of Money

Commodity Monies: Items used as money that also have intrinsic value in some other use. Meaning it is valuable not only because people use it as money, but also because the material itself has value.

Examples of commodity money

Gold

Silver

Copper

Salt (used as money in some societies)

Cigarettes (sometimes used as money in prisons or during wartime)

Fiat or Token Money: Money that has value because the government and society accept it as money, not because the material itself is valuable. Basically, it is items that are designated as money and that are intrinsically worthless.

This would include U.S dollar bills, euros, and Japanese yen.

Problem with Fiat Currency: Because the government determines the quantity, there is a constant temptation to print more money to finance spending.

Legal Tender: Money that a government has required to be accepted in the settlement of debts.

Currency Debasement: The decrease in the value of money that occurs when its supply is increased rapidly.

Solution for it: Many countries deal with this by having a partially independent central bank that controls the supply of money, insulated from direct political pressure.

EASIER EXPLANATION: Currency debasement happens when too much money is created, reducing each dollar's purchasing power (it loses value), and an independent central bank helps prevent this by carefully controlling the money supply and inflation.

(To prevent governments from printing too much money and causing inflation or currency debasement, many countries give their central bank the authority to manage the money supply independently of day-to-day political decisions.)

Measuring the Money Supply in the United States

Money is measured in how how liquid it is. (Going from most liquid to least liquid.)

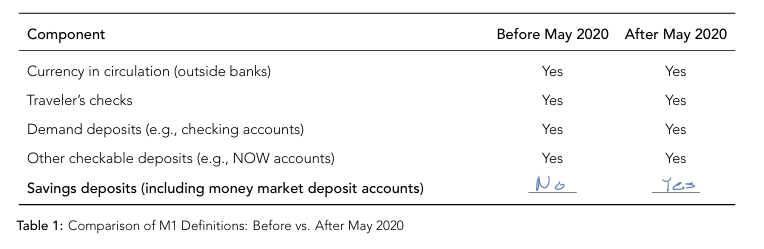

M1 Transactions of money:

Liquidity property of money: money that can be quickly and easily used to buy goods and services without losing value.

Money (M) is considered the most liquid asset because you can immediately spend it.

This money can be quickly used for transactions.

It includes:

Currency (cash held outside of banks).

Traveler's checks.

Demand deposits (e.g., checking accounts).

Other checkable deposits (e.g., NOW accounts).

M2: Broad Money

This includes everything in M1 plus "near monies."

Near Monies: financial assets that are not directly spendable like savings accounts, treasury bills, short term government bonds etc., but can be converted into cash quickly and with little loss of value

Beyond M2:

Broader definitions of money may include the amount of available credit on credit cards as part of the money supply., although there are no rules for deciding exactly what is, and what is not money.

For our purposes of this unit, "money" will always refer to transaction’s money or .

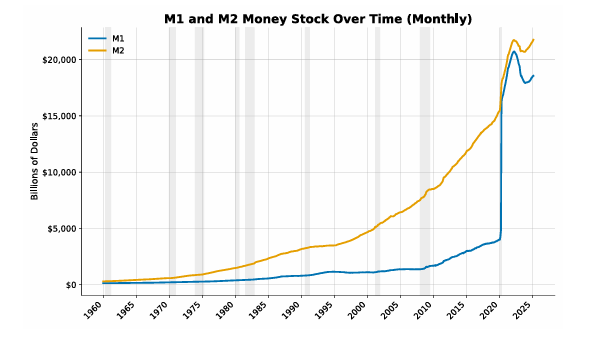

Figure 1: M1 and M2 Stock Overtime

In May 2020 there was a change in banking regulations that resulted in a classification in M1 and M2.

Types of Debt and Securities

Loans: Issued by banks to individual borrowers.

Examples: Car loans, student loans, mortgages.

Three Properties of a Loan:

Principal: The initial amount of money borrowed.

Interest Rate: The amount the borrower pays in order to get the principal.

The principal: is the original amount of money that is lent, borrowed, or invested before interest is added.

Typically, an annual percentage rate (APR): the borrower has to pay a percentage of the remaining principal balance with each payment.

APR: describes the yearly cost of borrowing money, and when applied to loans, interest is often charged based on the remaining balance of the loan, so as you pay it down, the interest amount decreases.

EXAMPLE:

Imagine:

You borrow $1,000

APR (interest rate) = 10% per year

You start paying it back over time

By month 1, the remaining principal is $1000.

Interest for the period: $100.

You make a payment: part of it goes towards interest, and part reduces the principal.

Now let’s say by month 2 you now only owe: $900

Now interest is charged on a smaller amount so it’s now $90.

You now pay less interest than before because you owe less money.

This system means:

Early payments (the beginning of paying off your loan) =

more interest, because interest is calculated on that larger balance of money owed.

less principal (money) paid off

Later payments (near the end of paying off your loan) =

less interest, because interest is now calculated on that smaller balance of money owed.

more principal (money) paid off

Because the loan shrinks over time.

Nominal Interest Rate: The percentage of interest stated on a loan or investment contract without adjusting for inflation.

Length: The duration or term of the loan.

Bonds (Securities):

Bonds: Issued by governments and corporations to raise sums of money larger than what can be acquired through a standard bank loan.

What is a bond?

A bond is basically an IOU (I owe you).

When you buy a bond:

You are lending money to a government or company

They promise to pay you back later

They also pay you interest while you wait.

Example: A company wants $1 billion.

Instead of asking one bank:

They issue bonds

1 million people each buy $1,000 worth of bonds

Now the company has $1 billion total

Companies use bonds because they need a lot of money, more than a normal bank can usually give. So, it’s why they borrow small amounts from many people so that the money can add up to a large amount.

Properties of a Bond:

Maturity Date: The length of time before the bondholder is paid back, ranging from to .

Face Value: the amount of money a bond is worth at the time it is issued and the amount it will be paid back at maturity.

Example:

You buy a bond with a face value of $1,000

When the bond “matures” (ends), you get $1,000 back

Coupon: A fixed amount paid back (usually semi-annually or annually) to the bondholder, functioning like interest. (It’s the extra money the bond pays you while you wait to get your original money back.)

Example:

You buy a bond for $1,000

The coupon rate is 5% per year

That means:

You get $50 every year (this is the coupon payment)

Plus, at the end, you get your $1,000 back

How do bonds work?

Suppose the government wants to raise $50 billion dollars to provide an after school program for low income households. Do they issue a $50 billion dollar bond?

No. they would issue many bonds that different individuals will purchase (typical bond face value is $1000)

These bonds are sold in the market.

Relationship between Price and Coupon: If a bond issuer wants to sell a face value bond, they offer it for sale in the bond market.

Does that mean somebody will automatically pay $1000 for the bond?

No. If you sell a car that’s worth 10k, will someone automatically pay 10k for it? No. The bond issuer would like to get, $1000 for their $1000 face value bond. What could they do if someone is only willing to pay $800 for it? Offer a higher coupon payment.

Here's the simple version:

A bond has a face value of $1,000.

The issuer (government or company) would like investors to pay $1,000 for it.

But investors might think:

"Why would I pay $1,000 for this bond? The interest payments aren't very attractive."

So, they might only be willing to pay $800.

What can the issuer do?

They can offer a higher coupon (higher interest payments).

For example:

Bond A: $1,000 face value, pays $20 per year in interest.

Bond B: $1,000 face value, pays $80 per year in interest.

Most investors would rather buy Bond B because it pays more interest.

So by increasing the coupon, the issuer makes the bond more attractive and increases the chance that investors will pay closer to the $1,000 face value.

is only viewed as worth , the issuer must offer a higher coupon payment to entice buyers to pay the full , or accept the lower market price.

A higher interest rate is a good thing for the person buying the bond because it means they earn more money each year for lending the person the money (the bond)

Common Types of Bonds

Treasury Securities: (e.g., T-bills, government bonds) bonds issued by the U.S. Federal Government.

Corporate Bonds: Debt issued by corporations.

Mortgage-Backed Securities (MBS):

Mortgages present a liquidity problem for banks because they are a large dispersesment of cash that is paid back over a long period of time (typically 30 years)

Banks will package together a group of mortgages into a single asset (the MBS) and sell it to financial institutions, retirement funds, or individuals.

Result: The bank receives immediate liquidity.

Those who by the MBS receive annuity payments (as people pay off the mortgage) over the life of the asset.

The Central Bank and Financial Intermediation

The Federal Reserve (The Fed)

Founded in 1913 by an act of Congress, with major reforms added in the 1930s.

It is an independent agency; it does not take direct orders from the President or Congress.

Responsibilities:

Monetary Policy: Conducted by the Federal Open Market Committee ().

FOMC Composition: 7 members of the Board of Governors, the president of the New York Fed, and 4 other district bank presidents (rotating).

Banking for Banks: Holds deposits for banks, clears payments, and manages interest rates and foreign exchange reserves.

Lender of Last Resort: Provides funds to troubled banks that cannot find other sources of funding.

Regulation: Monitors banking practices and standards.

Financial Intermediation

The process of transferring funds from savers (depositors) to borrowers.

Deposits: Money received by banks from savers.

Reserves: The money banks hold and do not lend out. This includes cash in the bank's vault and deposits held at the Federal Reserve Bank.

The Bank’s Balance Sheet

Accounting Equation: .

Liabilities: Money banks hold on deposit (owed back to depositors).

Assets: Reserves (cash on hand and deposits at the Fed) and loans/securities (money owed to the bank).

Reserve Requirements:

Required Reserve Ratio (rr): The percentage of deposits banks are legally required to hold.

Excess Reserves: Any reserves held in excess of the requirement.

.

The Creation of Money and the Money Multiplier

Money Creation Process

When a bank receives a deposit (e.g., ), it keeps a portion ( or ) and lends out the rest ().

The loaned money () is deposited into another bank (Bank 2), which then lends out of that ().

This cycle continues, increasing the total money supply through the creation of new deposits.

Money Multiplier Formula

Money Multiplier: The multiple by which deposits increase for every dollar increase in reserves.

.

The actual reserve ratio used in practice is determined by individual banks and can be higher than the legal requirement.

Total Money Supply (M):

(where is the total number of reserves).

Implications

Financial intermediation does not change the total number of reserves in the economy; it only changes the total money supply.

The Fed has complete control over the total number of reserves.

To change the money supply, the Fed can change the money multiplier (by changing the reserve ratio) or change the total number of reserves.

Tools of the Federal Reserve

Open Market Operations (Pre-Great Recession)

The purchase and sale of Treasury bonds (securities) by the Federal Reserve.

Open Market Purchase: The Fed buys bonds from banks, increasing banks' reserves and their ability to make loans (increases money supply).

Open Market Sale: The Fed sells bonds to banks, taking cash out of bank accounts at the Fed and decreasing reserves (decreases money supply).

The Federal Funds Rate (FFR)

The interest rate one bank charges another for an overnight loan of reserves.

Banks below the required reserve ratio can borrow from other banks at the FFR or from the Fed at the Discount Rate.

The demand for borrowing reserves depends inversely on the FFR.

The FFR should theoretically not exceed the discount rate.

FFR as a Signal: The FFR is a "lead" for other interest rates. Because it is short-term and essentially risk-free, other loans (car loans, mortgages) add a risk premium and a liquidity premium (for long-term durations) on top of this rate.

Interest on Reserves (Post-Great Recession)

In 2008, the Fed injected massive liquidity (reserves) into the system through emergency lending and asset purchases.

To control the money supply despite massive excess reserves, the Fed began paying banks interest on the money they hold on reserve.

Mechanism: A higher interest rate on reserves encourages banks to hold more reserves (increasing the reserve ratio), which decreases the money multiplier and the money supply.

Fed Decision Making: The Dual Mandate

The Federal Reserve Act of 1977

Mandates that the Fed must maintain Stable Prices (low inflation) and Maximum Employment.

Policy Stance

"Leaning against the wind": Counter-cyclical policy.

When the economy is too hot (high inflation), they cool it down (raise rates).

When the economy is too cold (high unemployment), they stimulate it (lower rates).

The Fed Rule

The Fed determines the Federal Funds Rate target based on several factors:

Output (Y): If output is above its natural rate, the Fed will raise the FFR target.

Prices (P): If prices/inflation rise, the Fed will raise the FFR target.

Other Factors (Z): External shocks or fiscal policy changes that might impact the economy.