tutorial 2 [week 4]

question 1

Step 1: Calculate the Required Rate of Return (Cost of Equity) for Each Firm Using CAPM

The CAPM formula is:

Required Rate of Return = Rf+ β × (Market Risk Premium)

Where:

Rf = Risk-free rate (3% or 0.03)

β = Firm's beta (1.25 for AstraZeneca and 0.75 for Shire)

Market Risk Premium = Expected return on the market minus the risk free rate (8% or 0.08)

For AstraZeneca:

Required Rate of Return = 0.03 + 1.25 × 0.08 = 13%

AstraZeneca's required rate of return (cost of equity) is 13%.

For Shire:

Required Rate of Return= 0.03 + 0.75 × 0.08 = 9%

Shire's required rate of return (cost of equity) is 9%.

Step 2: Compare the Required Rate of Return with the NPVs at Different Discount Rates

From the problem:

At a 12% discount rate, the project has a +£10 million NPV for both firms.

At a 15% discount rate, the project has a -£12 million NPV for both firms.

For AstraZeneca (Required Return = 13%):

At 12%: The project has a positive NPV of £10 million.

At 15%: The project has a negative NPV of £12 million.

Since AstraZeneca’s required return is 13%, which is between the 12% and 15% discount rates:

The NPV at 12% is positive, but since the required return is higher than 12%, the actual NPV would be lower than £10 million but still positive.

The project NPV would not fall to the negative value of -£12 million unless the discount rate exceeds 15%.

Therefore, AstraZeneca should proceed because the project’s NPV is still positive at the firm’s required rate of return.

For Shire (Required Return = 9%):

At 12%: The project has a positive NPV of £10 million.

At 9%: Shire’s required return is below the 12% discount rate used to calculate the £10 million NPV, meaning that the NPV for Shire would actually be even higher than £10 million at the firm’s required rate of return.

Since the project has a positive NPV at 12%, and Shire’s discount rate is even lower, the NPV for Shire would remain positive at its required rate of return.

Therefore, Shire should definitely proceed as well.

question 2

Given:

Shanken NV issues a perpetual bond, meaning it has no maturity and pays interest indefinitely.

The bond has a 10% coupon rate, with semi-annual payments (this means the bond pays 5% interest every six months).

The bond is currently selling for 108% of its face value.

The corporate tax rate is 35%.

a) What is the pre-tax cost of debt?

To calculate the pre-tax cost of debt for a perpetual bond, we use the following formula:

Cost of Debt (pre-tax) = Annual Coupon Payment/Current Market Value

Step 1: Determine the annual coupon payment

The coupon rate is 10% of the face value, but it’s semi-annual, so each period pays 5% of the face value. Therefore, the annual coupon payment is:

Annual Coupon Payment = 10% × Face Value= 0.10 × Face Value

Step 2: Calculate the current market price

The bond is selling for 108% of its face value, so:

Market Price = 1.08 × Face Value

Step 3: Plug into the formula

The pre-tax cost of debt is [assuming face value is 1000]:

Cost of Debt (pre-tax) = [0.10 × Face Value] / [1.08 × Face Value] = 9.26%

So, the pre-tax cost of debt is 9.26%.

method 2

you could also divide your annual coupon payment by 2 [as the payments are semi-annual] and multiply your final answer [which, now, is the interest rate, not the yield to maturity] by 2 to get 9.26%

b) What is the after-tax cost of debt?

The after-tax cost of debt is calculated by adjusting the pre-tax cost of debt for the company's tax rate. The formula is:

After-tax Cost of Debt= Pre-tax Cost of Debt × (1−Tax Rate)

Given the tax rate of 35%, the after-tax cost of debt is:

After-tax Cost of Debt = 9.26% × (1−0.35) = 6.02%

So, the after-tax cost of debt is 6.02%.

c) Which is more relevant, and why?

The after-tax cost of debt is more relevant for the company's financing decisions. This is because interest payments on debt are tax-deductible, meaning the company saves on taxes by issuing debt. The actual cost to the company for borrowing (what affects its cash flows) is lower than the nominal interest rate (pre-tax cost) due to these tax savings.

For example, while the company pays an interest rate of 9.26% to bondholders, the government effectively "pays" part of this interest in the form of reduced taxes, reducing the company's real cost of debt to 6.02%.

Thus, when evaluating the cost of capital or deciding on financing options, the after-tax cost of debt gives a more accurate picture of the true cost to the firm.

question 3

Given Data

Capital Structure:

Debt ratio = 40%

Equity ratio = 60% (100% - 40%)

Debt Information:

Coupon interest rate = 12%

Yield to maturity = 8%

Corporate tax rate = 20%

Equity Information:

Equity beta of FEB = 0.5

Industry beta (for the project) = 2

Market Information:

Expected return on the stock market = 10%

Risk-free rate = 1%

Project Information:

Initial investment = £10 million

Cash flows:

Year 1 = £5 million

Year 2 = £10 million

a) Cost of Equity of the New Project

To calculate the cost of equity for the new project, we use the Capital Asset Pricing Model (CAPM):

Where:

Rf = risk-free rate = 1%

Rm = expected market return = 10%

β = industry beta = 2

Substituting the values:

Cost of Equity = 0.01 + 2 × (0.10−0.01) = 0.19 or 19%

b) After-Tax Cost of Debt of FEB

The after-tax cost of debt can be calculated as follows:

After-Tax Cost of Debt= rd × (1−T)

Where:

rd = yield to maturity (cost of debt) = 8%

T = tax rate = 20%

Substituting the values:

After-Tax Cost of Debt = 0.08 × (1−0.20) = 0.064 or 6.4%

c) Weighted Average Cost of Capital (WACC) of the Project

WACC can be calculated using the formula:

Where:

S/S+B = weight of equity = 60% or 0.6

B/B+S = weight of debt = 40% or 0.4

Rs = cost of equity (calculated above) = 19% or 0.19

Rb = cost of debt = 8% or 0.08

Substituting the values:

WACC = (0.6 x 0.19) + (0.4 x 0.08) x (1 - 0.2) = 0.1396 or 13.96%

d) Net Present Value (NPV) of the Project

To calculate NPV, we will discount the expected cash flows to their present value and subtract the initial investment.

The formula for NPV is:

NPV = ∑ [CFt/(1 + r)^t] − Initial Investment

Where:

CFt = cash flow at time t

r = WACC = 13.96%

Initial Investment = £10 million

Cash Flows:

Year 1: £5 million

Year 2: £10 million

Calculating present values:

PV Year 1 = 5,000,000/(1.1396)1 = 4,389,119.66

PV Year 2 = 10,000,000/(1.1396)2 = 7,724,796.23

Total Present Value of Cash Flows:

Total PV = 4,389,119.66 + 7,724,796.23 ≈12,113,915.89

NPV Calculation:

NPV = 12,113,915.89 − 10,000,000 ≈ 2,113,915.89

e) Should FEB Undertake the Project?

Decision: Since the NPV of the project is positive, it indicates that the project is expected to generate value for the firm and its shareholders. A positive NPV suggests that the project would increase the wealth of the company's owners.

question 4

objective - our objective is to calculate Filer Manufacturing’s WACC. the WACC is a key metric that combines the company’s cost of equity and after-tax cost of debt, weighted by the proportion of each type of financing in the company’s capital structure

given data:

equity:

no. of outstanding shares = 9.5 mil.

share price = 53.00

beta equity = 1.2

debt:

bond 1:

face value = 75 mil.

coupon rate = 8% [semi-annual payments]

price = 93% of face value

maturity = 1 yr

bond 2:

face value = 60 mil.

coupon rate = 7.5%

price = 96.5% of face value

maturity = 1 yr

additional financial information:

risk free rate = 5.2%

market risk premium = 9%

tax rate = 35%

calculate cost of equity [Re] using the CAPM:

Re = risk free rate + beta x market risk premium

Re = 5.2% + [1.2 × 9%] = 16%

calculate yield to maturity for each bond:

bond 1:

face val = 75 mil.

coupon rate = 8% [annually], so each semi annual coupon = 8%/2 = 4% x 1000 = £40

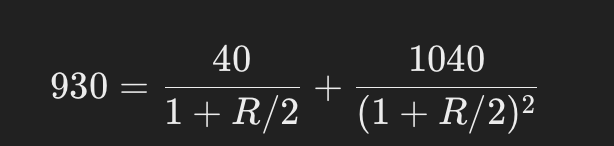

price = 93% of face value = £930 for each £1000 bond

maturity = 1 yr [2 semi annual periods]

NOTE - the bond will have 2 cash flows. the first cash flow is the semi annual coupon payment of £40 in 6 months. the second cash flow is the final coupon payment of £40 plus the face value of £1000 in 1 yr [1040].

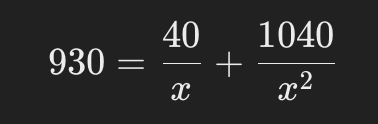

since the bond’s price is the present value of these cash flows discounted at the rate R/2 [where R is the annualised rate we want to find], we set up the equation:

to solve for R/2 , we must convert it into a quadratic form and solve using the quadratic formula.

rewrite the equation in terms of x:

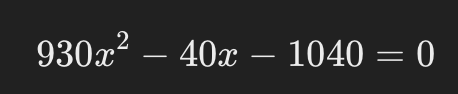

multiply both sides by x2 to eliminate the denominators [and make it equal 0]:

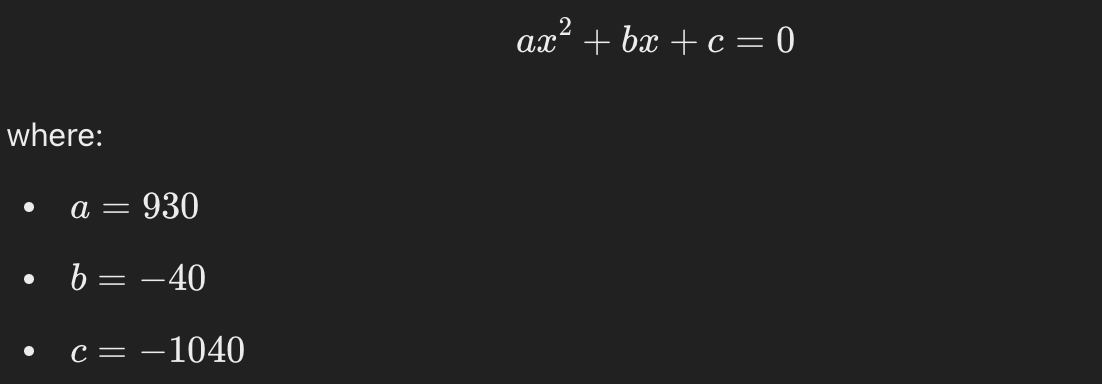

now, we have the quadratic formula in standard form:

substitute the values into the formula:

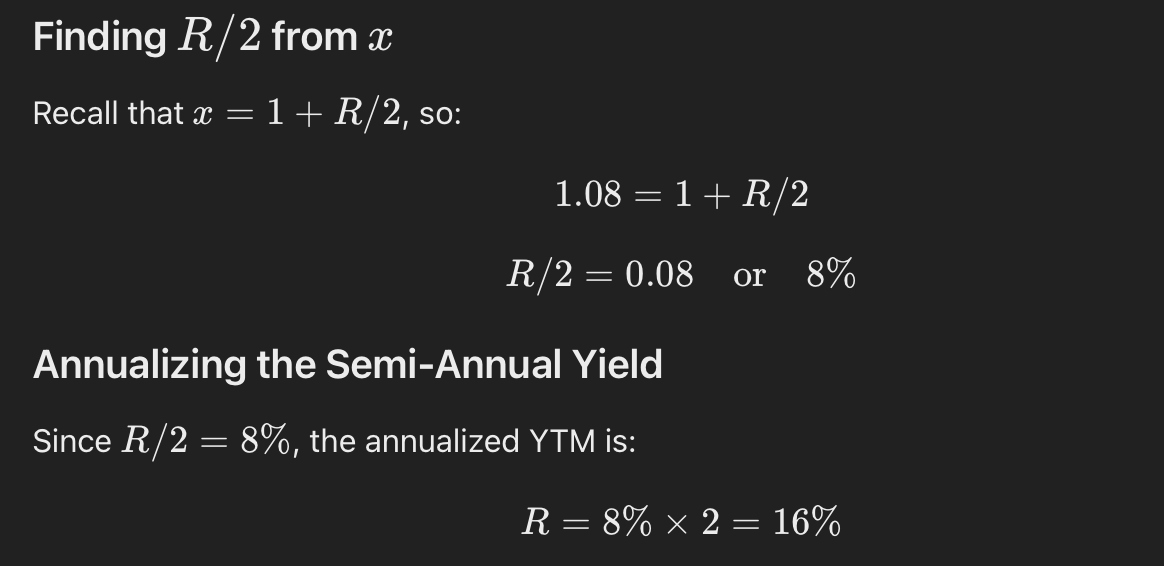

which will give you values 1.08, and -1.04 [we discard of the value -1.04 as negative values aren’t realistic]. therefore, x = 1.08, so:

so, the annualised YTM for bond 1 is 16%, or 15.84% exactly

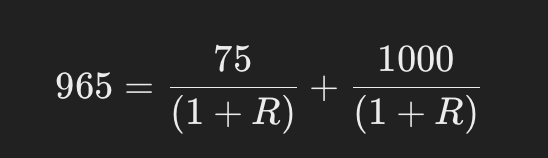

bond 2:

face value = 60 mil.

coupon rate = 7.5%, so each coupon = 7.5% x 1000 = £75

price = 96.5% of face value, which £965 for each bond £1000 bond

maturity = 1 yr [1 annual period]

since bond 2 matures in 1 yr, and pays interest annually, there is only 1 payment at the end of that year. this means both cash flows of the coupon payment and the face value are discounted at the same rate. therefore, the YTM equation is:

solving the equation [using the same method - quadratically] gives:

R = 11.4%

calculate the weighted average after tax cost of debt:

total market value of debt = bond 1 market value + bond 2 market value

bond market value = face value price percentage x face value

bond 1 market value = 93% x 75 mil. = 69.75 mil.

bond 2 market value = 96.5% x 60 mil. = 57.9 mil.

total market value of debt = 69.75 + 57.9 = 127.65 mil.

weight of each bond in total debt:

Wb1 = 69.75/127.65 = 54.6%

Wb2 = 57.90/127.65 = 45.4%

calculate the weighted average cost of debt:

Rd = [weight of bond 1 x YTM] + [weight of bond 2 x YTM]

Rd = [54.6% x 15.84%] + [45.4% x 11.4%] = 14.03%

calculate after tax cost of debt:

WA cost of debt [Rd] = Rd x [1 - tax rate] = 14.03% x [1 - 35%] = 9.12%

calculate the market value of the firm:

market value of equity = no. of shares x share price

market value of equity = 9.5 mil x £53 = 503.5 mil.

total firm value = equity market value + debt market value

total firm value = 503.5 mil. + 127.65 mil. = 631.15 mil.

calculate weights of debt and equity in firm capital structure:

weight = weight of equity or debt/total firm value

weight of equity [E/V] = 503.5/631.5 = 79.78%

weight of debt [D/V] = 127.65/631.15 = 20.22%

calculate the WACC:

plugging in values:

WACC = [79.78% x 16%] + [20.22% x 9.12%] = 14.58%

final answer — the company’s WACC is 14.58%