Chapter 8 - Process payments to suppliers

The purchasing process

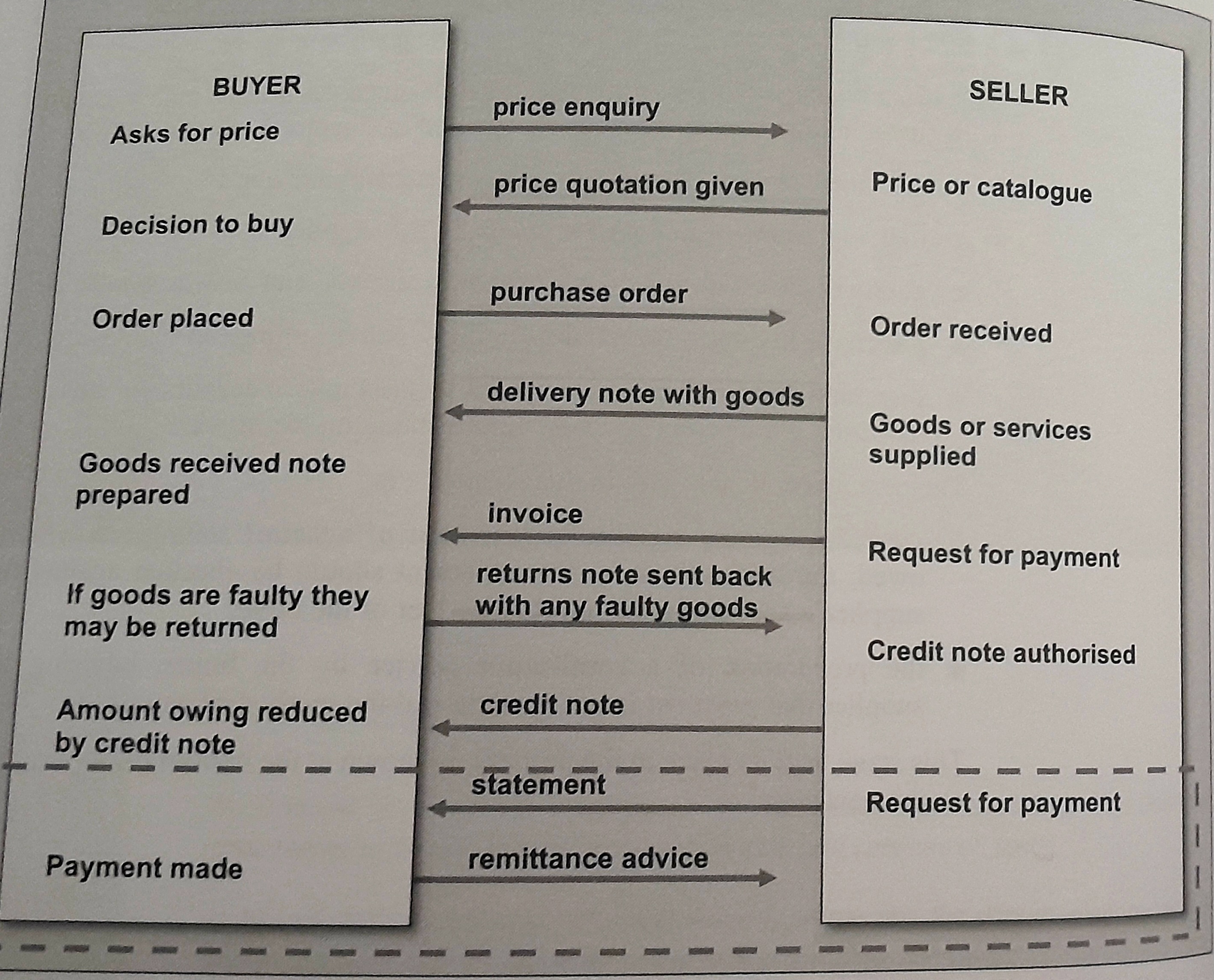

when a business makes a purchase of goods on credit, it deals with a number of financial documents

Purchase order - issed by the buyer ordering the goods

Delivery note - sent with the goods by the supplier

Goods recieved note - details of goods recieved and any discrepancies

Purchase invoice - recieved from the supplier setting out what is owed

Purchase credit note - any refund to the buyers account for missing, damaged or incorrect goods or any mistakes on the invoice

The next stage is :

the reciept of the suppliers statement of account setting out what is owed, the transactions on the statement should be checked against the suppliers account in the payable ledger of the buyer

the preparation of the remittance advice by the buyer, advising the supplier that payment is being made and the method of payment

reconciling the supplier statement of account

documents involved in the checking process are

delivery note and the actual goods recieved

supplier invoices and credit notes for calculations errors

supplier invoices and credit notes against the purchase order

credit notes for prompt payment discount

once the checks have been made and the invoices and credit notes have been authorised the buyer should settle up and pay the suppliers account in the payables ledger - contains all the details of all transactions

remittance advice - a document which states that a certain amount of money is being sent by a credit customer to a supplier in settlement of an account - to advise the sending of payment