Lecture 3: expenses, non-current assets, debts.

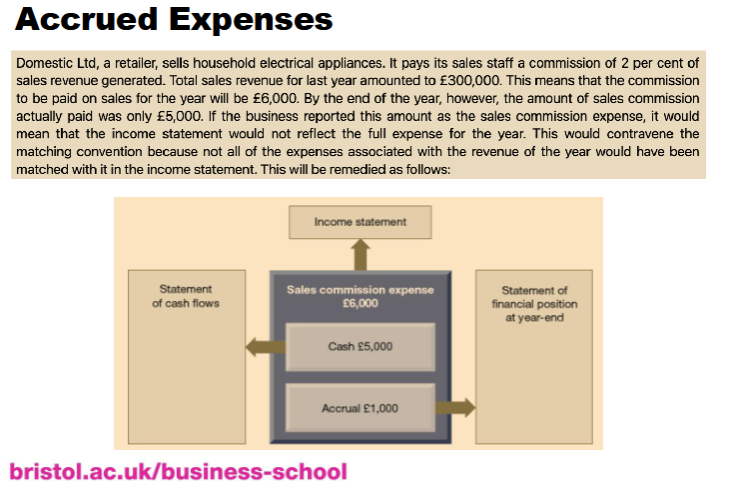

Accrued Expenses

Definition: expenses that are outstanding at the end of the reporting period.

o Example: Accrued Utilities

Utilities (e.g., electricity, water, and gas) are consumed continuously but are

typically billed after usage. If a company uses these utilities throughout the

month, the cost of the utilities used but not yet billed by the end of the month

represents an accrued expense. This is recorded as a liability as the service was

received (and thus the expense incurred) but payment has not yet been made.

o Recorded as liabilities on the SoFP, usually current liabilities (i.e., expected to be

settled within one year from the date of the SoFP).

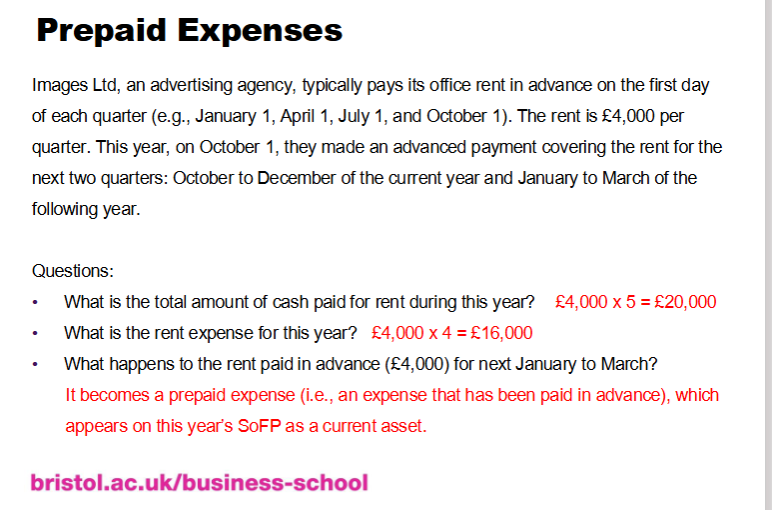

Prepaid Expenses

Definition: expenses that have been paid in advance at the end of the reporting period

o Examples: advance payments for expenses such as insurance premiums, rent,

or subscriptions.

o Recorded as assets on the SoFP, usually current assets (i.e., expected to be

consumed within one year from the date of the SoFP)

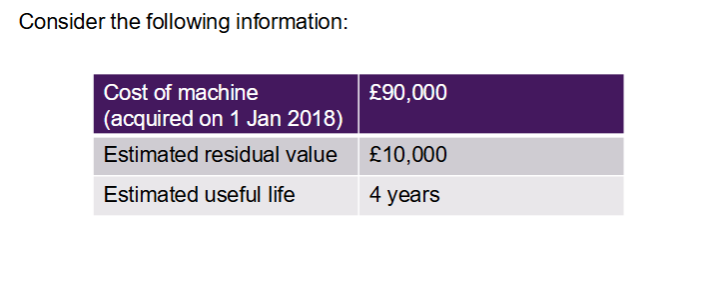

Non-current assets

Valuing NCAs

Non-current assets with finite lives:

• Definition: provides benefits for a limited period due to market changes, wear and

tear, etc.

• The amount used up is referred to as depreciation for tangible non-current

assets (or amortisation for intangible non-current assets).

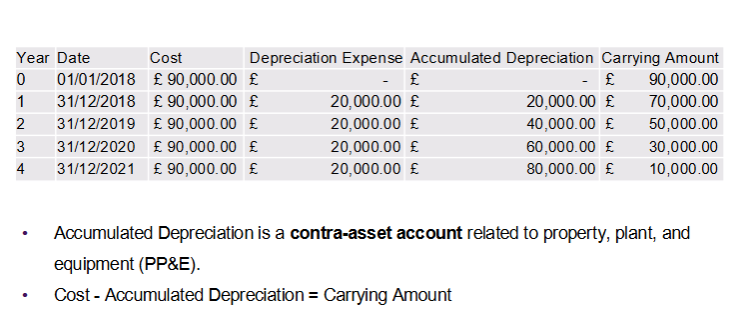

• Carrying amount (aka net book value or NBV) = cost – accumulated depreciation (or amortisation)Non -current assets with Indefinite lives:

Definition: provides continuous benefits without a foreseeable time limit.

• An example: land.

• They are not subject to depreciation/amortisation.

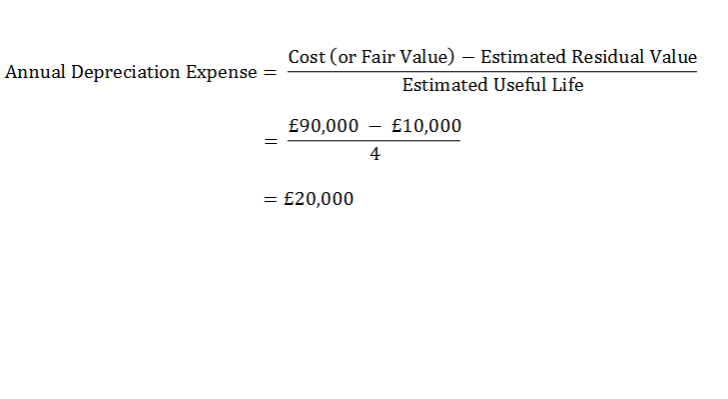

Depreciation

Two commonly used depreciation methods:

▪ Straight-line method

▪ Reducing-balance method

which depreciation method should be used?:The one that reflects the consumption of economic benefits provided by the asset.

- Use straight-line method when economic benefits are consumed evenly over time

(e.g., buildings).

- Use reducing-balance method when economic benefits consumed decline over

time (e.g., motor vehicles, certain machinery that loses efficiency).

straight-line method example:

Reducing-Balance Method Example:

Annual Depreciation Expense = Carrying Amount x Depreciation Rate

Suppose we apply a fixed depreciation rate of 40%:

Disposal

When an asset is sold, we need to calculate the gain or loss on disposal:

Gain (or Loss) on Disposal = Sale Proceeds – Carrying Amount

Example:

a

n asset, purchased two years ago for £100,000, has an estimated residual

value of £20,000 and a useful economic life of four years. Depreciation has been

applied on a straight-line basis over the past two years. Calculate the gain or loss

from the disposal if the asset is sold in the third year for £50,000.

• Annual Depreciation Expense = (£100,000 – £20,000) / 4 = £20,000

• Carrying Amount = Acquisition Cost – Accumulated Depreciation

= (£100,000 – £20,000 x 2)

= £60,000

• Gain (or Loss) on Disposal = Sale Proceeds – Carrying Amount

= £50,000 – £60,000

= –£10,000 → A loss of £10,000

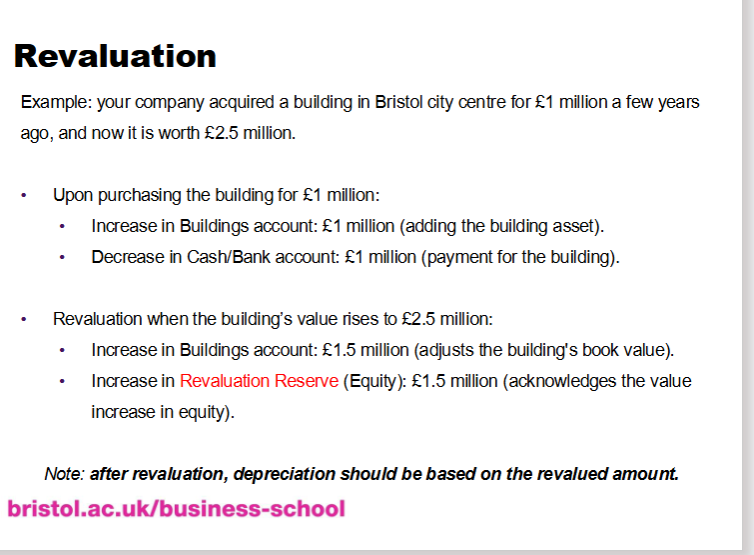

Fair Values of NCAs

Initial recording: at historic cost.

Subsequent measurement: at fair value, when reliably measurable.

Impacts:

Provides more up-to-date information about the business

Potentially enhances business image due to value appreciation over time.

Revaluation

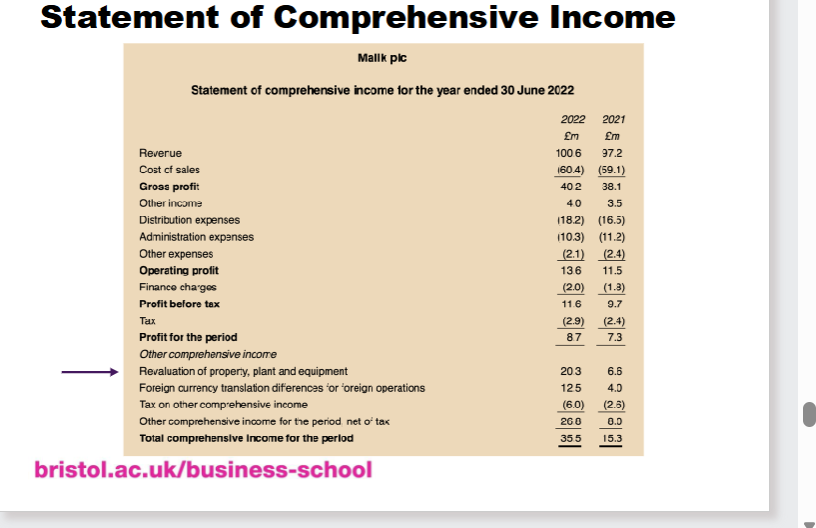

Statement of Comprehensive Income

Extends the conventional income statement to include Other Comprehensive Income (OCI): unrealised gains and some unrealised losses that affect equity

An unrealised gain (loss) refers to an increase (decrease) in the value of an asset/investment that has not been sold.

Examples of OCI items:

Property revaluation gain

Unrealised gains/losses from marketable equity shares

Foreign currency translation differences for foreign operations

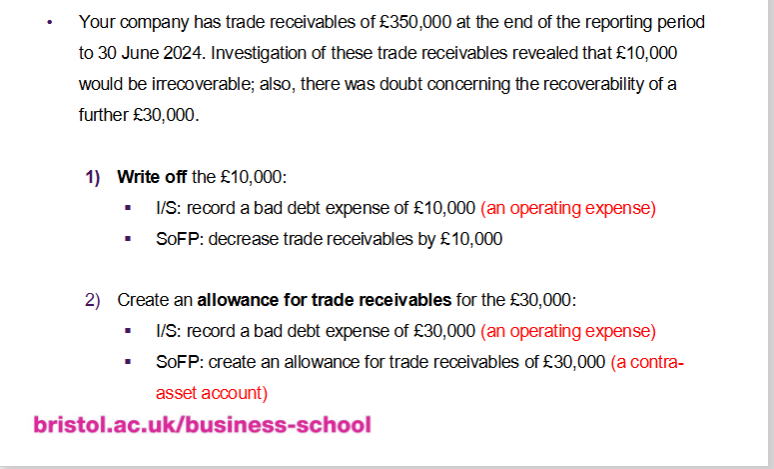

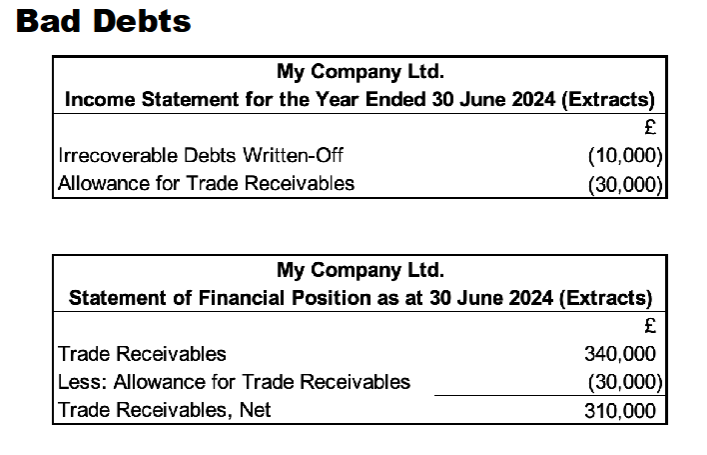

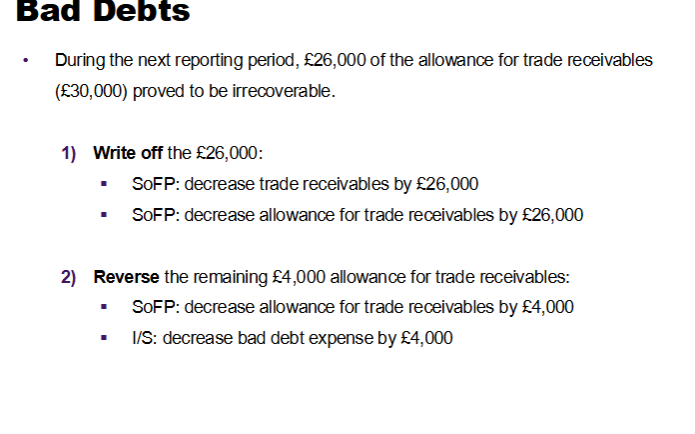

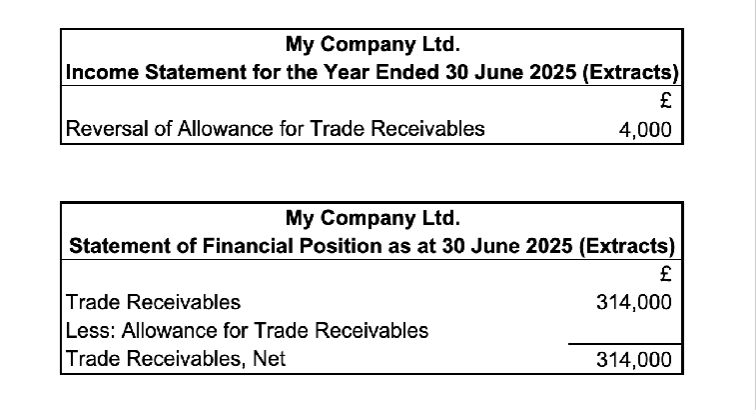

Bad Debts

Credit sales: some customers may not pay the amount due.

Impact on financial statements:

• Where it is reasonably certain that the customer will not pay,

the amount owed is considered an irrecoverable debt (or

bad debt) and written off.

• Where it is doubtful that a credit customer will pay, an

allowance for trade receivables expense should be

created.