Ch 4 - Elasticity Of Demand

Price elasticity of demand: measure of the responsiveness of quantity demanded to a price change. if a price is elastic, it is very responsive, if it is inelastic, it’s not responsive

- Key words:

- Ed = elasticity of demand

- Qd = quantity of demand

- P = price

- %△ = percentage change

- Ed = %△Qd / %△P

Steps:

- % change in Qd : New quantity - old quantity * 100 Old quantity

- % change in price : New price - Old price * 100Old price

- %△Qd / %△P

- Ignore negative sign

If the answer is:

- Between 0 and 1: price inelastic demand

- 1: unitary price elastic demand

- Above 1: price elastic demand

Inelastic demand curve:

- When a product’s PED is inelastic and the price falls, the firm will face loss in revenue

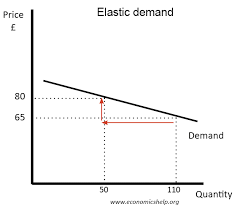

- Elastic demand curve:

- When the selling price of a product that has an elastic PED is decreased, the revenue increases (they sell more)

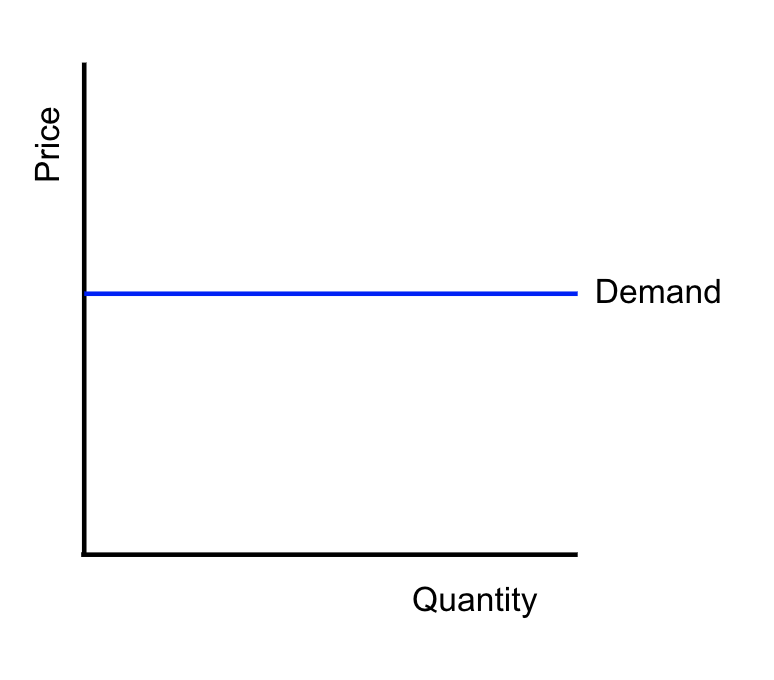

- Perfectly elastic demand curve:

The PED (price of elasticity of demand) will reduce as the price falls

- Demand becomes less elastic

Determinants of PED:

- Availability of substitutes (too many choices)

- Time

- Luxury

- Proportion of income is spent on a good

- Income elasticity of demand: measures the extent to which the quantity demanded of a product is affected by an income

- IED = %△Qd / %△ in income

For most normal accounts:

- Rise in consumer income = rise in demand

- Fall in consumer income = fall in demand

- Normal goods = positive YED

- Normal necessities = income inelastic

- Normal luxuries = income elastic

Inferior goods: as income rises, demand falls (consumers look for more affordable substitutes)

- Has negative IED, less than zero

Normal goods YED > 0:

- Increased income = higher demand

- Positive elasticity

Luxury goods YED > 1:

- Increased income

- Bigger % increase in demand

Inferior goods YED < 0:

- Increase income leads to fall in demand

- Negative elasticity

Unitary IED: perfectly proportional, Ey = 1

Zero income IED: consumer’s income doesn’t affect demand on product, Ey = 0

An Engel curve shows the relationship between demand for a good (x-axis) and income level (y-axis)

- Positive slope: normal good

- Negative slope: inferior good

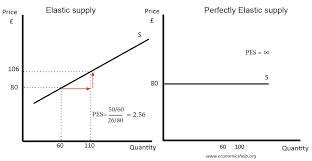

- PES price elasticity of supply: a measure of how much the quantity supplied of a product changes when there's a change in its price

- PES = %△ quantity supplied of the product / %△in price of the product

More time being considered = increased elasticity of a product

If total costs rise, supply will not be raised

Cross elasticity of demand (XED): measure of how much the demand of a product changes when there's a change in the price of another product

- XED = %△in quantity demanded of X / %△ in price of product Y

- If value of XED = positive, goods are substitutes for each other

- If value of XED = negative, goods are complements of each other

- If value of XED = 0, goods are unrelated