Principles of Macroeconomics Self-Notes

Chapter 1- Ten Principles

Introduction Video

Economics helps us human beings make choices, as our resources are limited (scarcity), these choices must be rational to maximize happiness-(may be profit, social impacts, family, achievements, knowledge,

ex of scarcity: time, materials, money, energy

First Principles= Trade Offs

Trade offs mean trading one thing means to give up one of your own things.

ex: time, guns, foods

Examples of typical trade off in countries:

-trade off of money and materials (limited resources) for expanding military to increase your military power around the world.

-Efficiency vs. Equality. - efficiency of max outputs and equality of distribute income equally

trade off example connecting to efficency and equality is Left and Right (left as democratic and right as republican..?)

Left is connected to equality, wants to improve welfare, requiring the input of money that needs increased taxes.

Right is connected to efficiency, caring most about max outputs and hard work. To encourage these actions from people, they seek decreased taxes to allow them to keep their income instead of contributing it to the government. Also seek little regulation. But this is opposite of left as less money to government means less welfare. “Less welfare transfers to the poor”

-Current vs Future consumption (spend now or save and spend later)

Part Two - Opportunity Costs

In order to make rational choices is to minimize opportunity cost and think at margin (marginal benefit vs. marginal cost)

Second principle= Opportunity Cost

Definition-The cost of something is what you give up to get it

examples:

-2 hours listening to lectures → giving up the happiness of other activities / paid tuition for the class

-putting money into military means giving up the opportunity to put money into welfare

-bringing manufacturing jobs back to the US needs money and resources that you cannot put into other sectors like technology/education

-free healthcare may need the opportunity cost of cutting benefits such as budget for military or education

note that “O.C” means opportunity cost

Part Three - Marginal Benefit and Marginal Cost

Third principle- To think at Margin

Margin is based on time and how many times you are going to do the action

Marginal Benefit = The additional benefit of a small incremental adjustment of an action

-marginal benefit is personally measured by your happiness

Marginal Cost = The additional cost of a small incremental adjustment of an action

-marginal cost is based on something that has CHANGED. if a price is set, then this marginal cost does not change and it is 0.

People tend to keep taking the incremental change of an action if the marginal benefit is more or equal to the marginal cost. Yet they stop when the marginal cost is more than the marginal benefit'

Part Four - The rest of the Principles

Principle Four - People respond to incentives

Definition of Incentives = something that induces a person to act

examples:

-increased tax on gasoline → higher total cost of gasoline → people are less inclined to buy gasoline and would seek to use less → stay home and live on their provided welfare

Principle Five - Trade can make most people better off

principle that almost all economists agree on

Principle Six - The markets are usually a good way to organize economic activity

economic activity may be organized by governments, markets, war, etc..

supply and demand model

Principle Seven - Government can sometimes improves social efficiency

markets are usually better at organizing economics but under certain circumstances, government can be better. markets are not perfect and neither is the government! as government and markets care mostly about their own happiness

examples-

pollution = as markets seek profits, they do no care/focus on pollution as its an externality

externality → market and government failure

Principle Eight - Standard of Living depends on the ability to produce goods and services productivity

Principle Nine - Prices rise when the government prints too much money (inflation)

Principle Ten - The society faces a short-run trade off between inflation and unemployment

Chapter 2 - Think like an Economist

Introduction Video

to think like an economist we…

make observation → make a theory → test theory by more observations → ( two options) of either a rejected theory that goes back to observation OR fail to reject with leads back the theory

-when a theory is rejected, it pushes economists to make new and better theories

-sometimes data rejects or fails to reject a theory, either now or later

There is no absolute truth!

First model - Circular Flow

Second model - Production Possiblities

Part two - Circular Flow Model (Youtube Video)

highlights the flows within a economy, flow of resoruces, money, goods and services

cost of production and profit

The model shows the interaction between two economic decision makers of households and business who are both buyers and sellers, and two economic markets of the market of resources and the market of goods and services.

Households - people in the same housing unit who own economic resources of land, labor, capital, and entrepreneurial

-land resources are natural, can be the land, water, or oil

-labor is source of income, jobs

=capital is goods used to produce other goods and services

-entrepreneurial ability is the human resource that combines the other resources to produce new goods and services and bring them to market

Businesses - private owned organizations that produces goods and services and then sells them

both businesses and households interact in the market

The market for resources is where households sell and businesses buy economic resources of land, labor, capital, and entrepreneurial ability

-business are owned by people that are in a household

-businesses are buyers and households are sellers!

In exchange of giving the businesses these economic resources, households get wage for labor, rent for land, interest for capital, and profit for entrepreneurial ability

Market for goods and services

-businesses sell these goods and services in this market for households, households use part of their income for the goods and services. Businesses earn revenue.

-businesses are sellers and households are buyers!

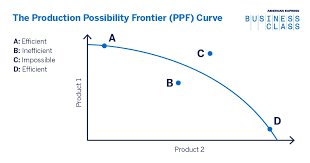

Part Three - Possibility Production Frontier (Part One)

A graph that shows all possible combinations of two outputs that an economy can produce, given the available inputs and technology.

-inputs are the factors of production

-outputs are the goods and services that are produced

Assumptions for the model:

-fixed resources

-fixed technology (no improvement)

-two broad classes of output

-some inputs are better adapted to the production of one good than to the production of another (specialization)

Points on and inside the Frontier on the graph are the all possible combinations of the economy

-inside points are inefficient, they can be improved to be on the curve

-points ON the curve are efficient

-points above the curve are not possible to produce outside the frontier (unattainable) but with trade its possible to consume outside the frontier (No Trade deficit)

examples:

Point B = China before 1978, under the communist system

Point D = USA is already here

-its not possible to increase one good without decreasing the other good (efficiency)

PPF - Part Two

the PPF is bowed outwards, concave, because of the specialization of inputs

-goal is to minimize opportunity costs

-move the inputs rationally to minimize these costs

PPF - Part Three - Calculating Opportunity Cost and The Law of Increasing Cost

opportunity cost will involve gaining a certain number of product while also giving up a certain number of the other product

Formula for Opportunity Costs for Product = Give Up/Gain

Law of Increasing Opportunity Cost - When we have more of one goods, if we want additional of these good, we have to give up more and more of the other good.

-the first good, the additional one, will increase in its opportunity costs because inputs are being moved around and the other good is being given up

PPF - Part Four - Relax Assumptions

Fixed Resouces:

-Adding more resources would more the whole curve forward

-less labor force would cause the production of goods to go down and shift the whole curve to the left

-more of an input can cause one of the inputs to shift up their axis

Fixed Technology:

-improved technology can shift the curve as a whole forward to the right

Two Inputs are not changed because of the two axis’s of a graph, changing the number of inputs would change the dimensions of the graph, making it hard to graph

Specializations are not changed because its realistic