Economics Unit 5

- %%asset%% → anything of value that we own

- %%liability%% → anything of value that we owe

- %%money%% → anything that we see as an asset that fulfills these three roles: * ^^medium of exchange^^ → you can purchase goods and services with it * ^^store of value^^ → retains its value over time * ^^unit of account^^ → making economic calculations and comparing prices

- types of money: * ^^commodity^^ → something with intrinsic value (just has value, ex: gold, silver) * ^^commodity-backed money^^ → money that is guaranteed by a physical commodity (ex: certificate that says $10 worth of gold is in the bank) * ^^fiat (greenbacks)^^ → not backed by a commodity, has value because the government says so

- %%liquidity%% → how easily an asset can be converted into cash * liquid if it can be easily converted into cash (ex: cash) * illiquid if it cannot be easily converted into cash (ex: houses)

- %%money supply%% → total amount of assets in the economy considered money circulating around the economy * we have different definitions (M1, M2) of the money supply based on the assets we include in them and how liquid they are * ^^M1^^ → currency in circulations (dollar bills and coins), checkable bank deposits (money in our checking accounts, checks and debit cards), traveler’s checks (checks that can be used when traveling without high service fees) * ^^M2^^ → includes all of M1 plus near moneys * ==near moneys== → assets that are not as liquid as the money in M1, but they are very close (ex: money in our savings accounts, short term certificates of deposit)

- %%Savings Investment Identity%% → we have idea that when we are saving, we are doing so by investing (savings = investments) * ^^Interest Rate (i)^^ → true profit for lenders and the true cost for borrowers * ==purpose of the interest rate== → compensate lenders for their lending services and also to account for inflation * when the money supply goes up, interest rates go down * households respond to interest rates going down in two ways: * households hold onto currency rather than investing it * households take out more loans for interest sensitive consumption (consumption that we have to borrow to do, have to take out a loan to do that consumption, ex: buying a house) * when money supply goes down, interest rates go up * households increase the money they put into investments * household consumption will go down * households will take out fewer loans for interest sensitive consumption

- diversification → putting money in different investments so that if some of the money goes bad, you won’t lose your savings

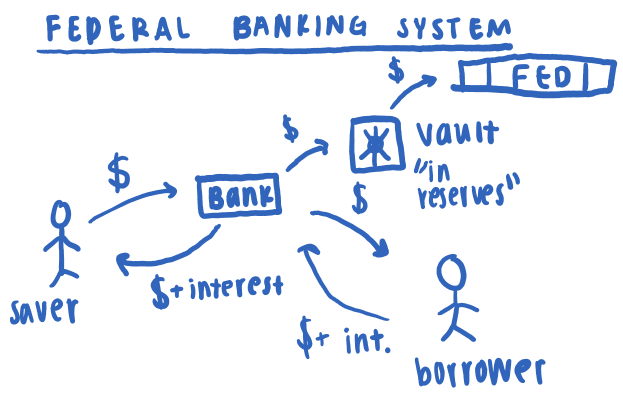

\ THE BANKING SYSTEM

- banks are one type of financial intermediary

- financial intermediary → firms that are in business for profit that transform the savings of investors into loans for borrowers * mutual funds * pensions/retirement plans * life insurance policies * banks

- federal reserve imposes a reserve requirement: a fraction of deposits needs to be in the reserves; excess reserves can be lent out to borrowers * if banks at the end of the banking day do not have enough in the reserve, they have to pay the Fed a fee * banks can borrow from other banks, must pay interest called federal funds rate * banks can borrow money directly from the fed, must pay interest called the discount rate * **discount rate is one percent higher than the federal funds rate to discourage banks from borrowing from the fed**

- %%federal deposit insurance corporation%% → guaranteeing deposits in banks up to $250,000

THE FED AND MONETARY POLICY

- FUNCTIONS OF THE FED * “banker’s bank” → provides financial services for banks * supervise and regulate financial system → decide things like what reserve requirement is * maintain stability → prevent bank runs, etc. * monetary policy → stabilizes where we are in the economy * monetary policy works because of the money multiplier * money multiplier → one dollar of additional deposits in the banking system multiplies to more than one dollar circulating around the economy * not just printing out more money, it about the money circulating around the economy * expansionary monetary policy or expansionary fiscal policy when in a recession * IN A RECESSION → expansionary monetary policy (must have all 3 words)

- 3 TOOLS OF MONETARY POLICY * reserve requirements → if we tell bank to change how much they keep in reserves, theoretically, it could impact how much money is circulating around the economy and also what interest rates are * required reserves decrease, banks have more excess reserves to lend, banks lend more which means there is more money circulating around the economy, money supply goes up, interest rates go down, households hold onto currency rather than investing, households take out more loans, consumption goes up, GDP goes up, expansionary monetary policy * required reserves increases, banks have less excess reserves to lend, banks lend less which means there is less money circulating around the economy, money supply goes down, interest rates go up, households invest more, households take out less, consumption goes down, GDP goes down, contractionary monetary policy * spread between the federal funds rate and the discount rate * fed can only control the discount rate directly, fed can’t control the federal funds rate in this way * fed can incentivize the behavior of the banks by controlling the difference between the federal funds rate and the discount rate * increase spread between federal funds rate and discount rate, banks won’t risk making as many loans, less money circling around the economy, etc. contractionary monetary policy * decrease spread between federal funds rate and discount rate, banks will risk making many loans, increases money supply, interest rates go down, households hold onto currency, gdp goes up, expansionary monetary policy * open market operations → when the fed buys and sells bonds from a bank with the purpose of stabilizing the economy * they typically buy a specific type of bond → bonds issued by the federal government * if the fed buys these treasury bonds from the banks, the bank has more excess reserves to lend, money supply goes up, expansionary monetary policy * if the fed sells treasury bonds to the bank, the bank as fewer excess reserves to lend, the money supply goes down, contractionary monetary policy * CONSIDERATIONS FOR MONETARY POLICY * lags * recognition lag * decision lag * implementation lag * FOR FRQ MUST CALCULATE GDP, UNEMPLOYMENT RATE, AND INFLATION RATE * from that information we will have to decide where we are in the business cycle, expansion or recession, THEN must say how the federal government would conduct fiscal policy and how the federal reserve would conduct monetary policy

\ \

\