Accounting Information Systems Chapter 1

Introduction

Information is a strategic asset if the firm

(1) knows what information it needs;

(2) develops systems to collect, store, and process that information; and

(3) uses that information to make critical decisions that will ultimately affect performance and profitability.

Accountants as Business Analysts

Firms have access to a tremendous amount of data

For instance, transactional data produced from point-of-sale terminals or bank deposits, consumer behavior data on customer preferences and purchases, product availability and costs, operational statistics generated throughout a supply chain, and more—that can contain valuable insights to enable decision making.

With such data, firms can more easily benchmark activity and compare and contrast results.

In that way, firms can determine the most effective way to allocate resources such as human resource (HR) talent, capital (e.g., equipment, buildings, etc.), and budgets (e.g., marketing, advertising, and research and development)

Definition of Accounting Information Systems

One type of information system is used in every firm: an accounting information system (AIS).

An AIS is defined as a system that records, processes, summarizes, reports and communicates the results of business transactions to provide financial and nonfinancial information to facilitate decision making.

In addition, an AIS is designed to ensure appropriate levels of internal controls (important security measures to protect the integrity of sensitive data) for those transactions.

A Simple Information System

An AIS, just like any system, can be explained using a general systems approach with input, storage, processing, and output activities.

The input may come in the form of sales recorded on a Starbucks cash register or point-of-sale terminal.

Processing those data may take the form of getting the input into storage (such as a database or a data table).

Processing might involve querying that database (e.g., using SQL or other queries) to produce the output in the form of a report for management use.

As an example, Starbucks may query its sales database to report how much coffee it sells around Christmas to see if additional sales incentives need to be made to increase sales around Christmas in the future.

Attributes of Useful Information

Information from an AIS must be both relevant and be a faithful representation

Relevance

Confirmatory, or feedback value (corrects or confirms what had been predicted in the past).

Predictive value (helps with forecasting the future).

Materiality (is above a threshold where missing or inaccurate information would impact decisions).

Faithful Representation

Complete (includes all monetary transactions; not missing any).

Neutrality (not biased one way or the other).

Free from error (contains no mistakes or inaccuracies).

Relevance

To be useful, information must be relevant to the decision maker, capable of influencing the decisions of users.

Information is relevant when it helps users evaluate how past decisions actually worked out (feedback value) or predict what will happen in the future (predictive value).

It is also relevant if the information is material in size, big enough to influence the decisions of its users.

Faithful Representation

Information exhibits faithful representation if the information is complete (i.e., includes all applicable transactions), is neutral (i.e., free from bias), and is free from error).

Faithful representation information represents the substance of the underlying economic transaction.

Data versus Information

Data are simply raw facts that describe the characteristics of an event. However, in isolation, data have little meaning.

Information is defined as data organized in a meaningful way to be useful to the user. Thus, data are often processed (e.g., aggregated, calculated, sorted, manipulated, etc.) and then combined with the appropriate context (year or location, etc.) to turn it into information.

To the extent that computers can assist in processing and organizing data in a way that is helpful to the decision maker, it is possible that there may be so much information available to actually cause information overload.

Information Overload is defined as the difficulty a person faces in understanding a problem and making a decision when faced with too much information.

The overall transformation from a business need and business event (like each individual transaction including bananas) to the collection of data and information to an ultimate decision is called the information value chain.

If Walmart needs to know how many bananas it should have at each location (i.e., business need), it will collect transactions involving banana sales (i.e., business event).

Discretionary versus Mandatory Information

Managerial accounting information is generally produced for internal information purposes and would usually be considered to be discretionary information because there is no law requiring that it be provided to management.

In contrast, much of the financial and tax accounting information is produced by the company for external information purposes such as for investors, banks, financial analysts, bondholders, and the Internal Revenue Service (IRS) in the form of tax returns or audited financial statements.

This financial and tax accounting information would generally be considered to be mandatory information.

Role of Accountants in Accounting in Accounting Information Systems

In today’s age, technology is a key tool in creating information systems for today’s businesses.

The International Federation of Accountants (IFAC) notes:

IT has grown (and will continue to grow) in importance at such a rapid pace and with such far reaching effects that it can no longer be considered a discipline peripheral to accounting.

Rather, professional accounting has merged and developed with IT to such an extent that one can hardly conceive of accounting independent from IT.

Accountants have a role as business analysts and business partners; that is, they gather information to solve business problems or address business opportunities.

They determine what information is relevant in solving business problems, work with the AIS (and/or other data provider) to create or extract that information, and then analyze the information to give needed information to the decision maker.

Specific Accounting Roles

It is important to recognize the potential role of accountants in accounting information systems, including the following:

The accountant as user of accounting information systems—whether it be inputting journal entries into an accounting system, using a financial spreadsheet to calculate the cost of a product, or using anti-virus software to protect the system, accountants use an AIS.

Accountants serving in an audit role should be able to understand how to access their client’s AIS and how to use at least one major computer-assisted auditing package.

The accountant as manager of accounting information systems (e.g., financial manager, controller, CFO).

Accountants must be able to plan and coordinate accounting information systems and be able to organize and staff, direct and lead, and monitor and control those information systems.

The accountant as designer of accounting information systems (e.g., business system design team, producer of financial information, systems analyst).

Systems Analyst: Person responsible for both determining the information needs of the business and designing a system to meet those needs.

Accountants must have significant practical exposure as they work to develop a system that will meet the needs of users.

The accountant as evaluator of accounting information systems (e.g., IT auditor, assessor of internal controls, tax advisor, general auditor, consultant)

The Sarbanes-Oxley Act of 2002 (SOX) requires an evaluation of the internal controls in an AIS. As part of that act, and as part of a standard audit, accountants must be able to tailor standard evaluation approaches to a firm’s AIS and offer practical recommendations for improvement where appropriate.

In addition, the accountant must be able to apply relevant IT tools and techniques to effectively evaluate the system.

Certifications in Accounting Information Systems

Certified Information Systems Auditor (CISA)

Identifies those professionals possessing IT audit, control, and security skills.

Generally, CISAs will perform IT audits to evaluate the accounting information system’s internal control design and effectiveness.

Also evaluates whether there is a threat of a cybersecurity breach to the financial reporting system of a company it is auditing.

Certified Information Technology Professional (CITP)

Identifies accountants (CPAs) with a broad range of AIS knowledge and experience.

The CITP designation demonstrates the accountant’s ability to leverage technology to effectively and efficiently manage information while ensuring the data’s reliability, security, accessibility, and relevance.

CITPs may help devise a more efficient financial reporting system, help the accounting function go paperless, or consult on how an IT function may transform the business.

Also designs a more efficient financial reporting system and helps design and implement a financial reporting system be done without paper

Certified Internal Auditor (CIA)

Is the only globally accepted certification for internal auditors and is the standard to demonstrate their competency and professionalism in the internal auditing field.

Examples include:

Determining if the internal controls are designed properly and working.

Looking for fraudulent financial transactions and working for the audit committee.

The Value Chain and Accounting Information Systems

Business value is defined as all those items, events, and interactions that determine the financial health and/or well-being of the firm.

To consider how value is created, we begin by looking at the business processes.

A business process is a coordinated, standardized set of activities conducted by both people and equipment to accomplish a specific task, such as invoicing a customer.

To evaluate the effectiveness of each of its business processes, a firm can use Michael Porter’s value chain analysis.

A value chain is a chain of business processes for a firm.

Primary activities directly provide value to the customer and include the following five activities:

Inbound logistics are the activities associated with receiving and storing raw materials and other partially completed materials and distributing those materials to manufacturing when and where they are needed.

Operations are the activities that transform inputs into finished goods and services (e.g., turning wood into furniture for a furniture manufacturer; building a house for a home builder).

Outbound logistics are the activities that warehouse and distribute the finished goods to the customers.

Marketing and sales activities identify the needs and wants of customers to help attract them to the firm’s products and, thus, buy them.

Service activities provide the support of customers after the products and services are sold to them (e.g., warranty repairs, parts, instruction manuals, etc.).

These five primary activities are sustained by the following four support activities:

Firm infrastructure activities are all of the activities needed to support the firm, including the chief executive officer (CEO) and the finance, accounting, and legal departments.

Human resource management activities include recruiting, hiring, training, and compensating employees.

Technology activities include all of the technologies necessary to support value-creating activities.

These technologies also include research and development to develop new products or determine ways to produce products at a cheaper price.

Procurement activities involve purchasing inputs such as raw materials, supplies, and equipment.

An AIS can add value to the firm by making each primary activity more effective and efficient.

For example, AISs can assist with inbound and outbound logistics by finding efficiencies and cost savings (transportation and warehousing costs, etc.).

AISs can make marketing, sales, and service activities more valuable by summarizing data about key customers to help manage and nurture a firm’s interactions with its clients.

An AIS:

Helps with the firm infrastructure by giving management information relevant to the decision makers.

May also help provide the internal control structure needed to make sure the information is secure, reliable, and free from error.

Helps produce external and internal financial reports efficiently and helps decision makers get timely access to the processed information.

This may give the information to the decision maker in time to influence the decision.

Supports the human resources function by assisting employees, who are arguably the most valuable asset of the firm.

This assistance includes easy access to payroll information, compensation policies, benefits, tax benefits, and so on.

Assists procurement by improving the effectiveness and efficiency of the supply chain.

This helps ensure that the right product is at the right location at the right time, including receipts of raw material from suppliers to delivery of finished goods to the customers.

AIS and Internal Business Processes

An AIS within a firm is usually the foundation for an enterprise system (ES) —also called an enterprise resource planning (ERP) system.

An enterprise system is a centralized database that collects data from throughout the firm.

This includes data from orders, customers, sales, inventory, and employees.

As the data are integrated into one single, centralized database to become useful information, authorized employees throughout the firm (from the CEO all the way to the lowest-paid line worker) have access to the information they need to make a decision.

For most firms, the informational benefits of these integrated data include enhanced completeness, transparency, and timeliness of information needed to effectively manage a firm’s business activities.

As an example, an enterprise system can automate a business process such as order fulfillment.

The enterprise system can take an order from a customer, fill that order, ship it, and then create an invoice to bill the customer.

As problems arise (e.g., backordered products, returned products, trucker strikes, etc.), the enterprise system gives all within the firm the most current, real-time information to address these issues.

The enterprise system serves as the backbone of the firm’s internal business processes and serves as a connection to the external business processes with external partners.

AIS and External Business Processes

Firms do not work in isolation. They are always connected to both their suppliers and customers and their wants and needs.

The AIS assists in business integration with external parties such as suppliers and customers.

The firm’s interaction with the suppliers is generally called supply chain management, and the interaction with its customers is generally called customer relationship management.

The Supply Chain

Supply chain refers to the flow of materials, information, payments, and services from raw materials suppliers, through factories and warehouses, all the way to the final customers of the firm’s products.

The supply chain also handles the product returns from the firm’s customers back to the firm’s suppliers, which represents a significant process that requires substantial planning.

To make the supply chain function efficiently, supply chain tasks include processes such as purchasing, payment flow, materials handling, production planning and control, logistics and warehousing, inventory control, returns, distribution, and delivery, and is usually assisted by supply chain software.

The software used to connect the focal firm with its suppliers is generally referred to as supply chain management (SCM) software.

This software addresses specific segments of the supply chain, especially in manufacturing scheduling, inventory control, and transportation.

This SCM software is designed to facilitate decision making and optimize the required levels of inventory to be ordered and held in stock.

Supply chain management systems allow inventory to be optimized to lower the amount of required inventory on hand while not decreasing sales.

Customer Relationship Management

The more a company can learn about its customers, the more likely it will be able to satisfy their needs.

Customer relationship management (CRM) software is a term that describes the software used to manage and nurture a firm’s interactions with its current and potential clients

CRM software often includes the use of database marketing tools to learn more about customers and to develop strong firm-to-customer relationships.

CRM software also includes using IT to manage sales and marketing for current sales and customer service and technical support after the sale is done.

AIS, Firm Profitability, and Stock Prices

AIS and Firm Profitability

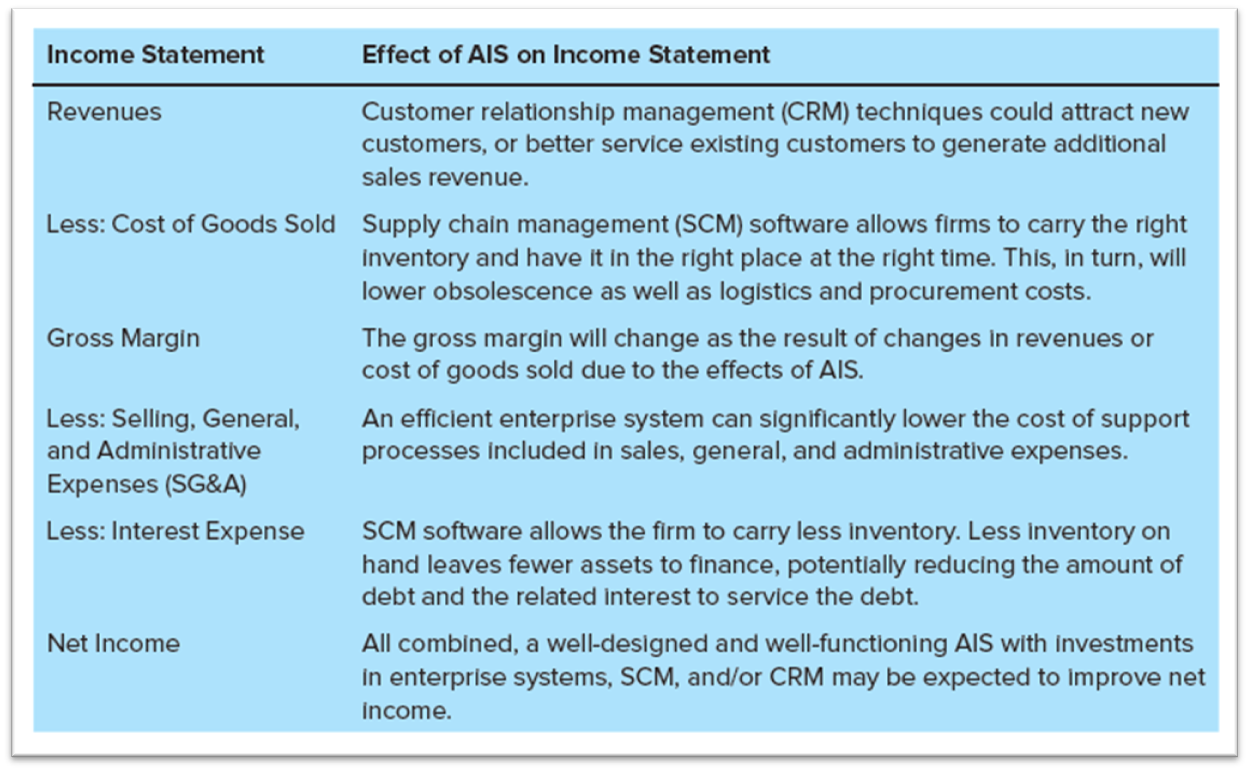

One way to consider how AIS creates value is to look at an income statement.

Accountants understand that to make more profits, a firm either needs to increase revenues or decrease expenses (or both!).

In an academic study, a positive association was found between the level of the firm’s annual AIS investment and its subsequent accounting earnings (as measured by return on assets and return on sales), suggesting that AIS investment does in fact create value.

AIS and Stock Prices

Every time a firm makes an investment, it expects a return of its original investment as well as a return on that investment. This is the case for AIS investments as well.

When an investment is announced by a public firm, stock market participants assess whether the investment will pay off or not, either by enhancing revenues or reducing expenses or some combination of both.

If AIS investments simply replace human labor to automat e business processes, they are defined as automate AIS investments.

The automate process will typically digitize (i.e., put in a digital form) the business processes.

Once digitized, this information can be automatically and easily summarized in a usable form (i.e., reports, etc.) for management use (defined as the AIS strategic role of informate-up) or in a usable form to employees across the firm (defined as AIS strategic role of informate-down).

AIS investment can also change the basis of competition and redefine business and industry processes (defined as the AIS strategic role of transform).

The lowest strategic role for technology is to Automate manual processes. The highest strategic role for technology is Transform, with Informate-up and Informate-down having a medium strategic role.

Summary of AIS Strategic Roles:

Automate —replace human labor in automating business processes.

Informate-up —provide information about business activities to senior management.

Informate-down —provide information about business activities to employees across the firm.

Transform —fundamentally redefine business processes and relationships.

On average, the 172 Automate AIS investments increased firm market value by 0.05 percent and the 95 Informate AIS investments increased firm market value by 0.40 percent. On average, the Transform AIS investments increased firm market value by 1.51 percent, which is statistically greater than zero.